Timing & trends

In today’s post I’m going to make the case for stocks moving down into a sharp correction over the next 4 weeks and conclude with my thoughts on inflation.

To begin we need to examine the last two intermediate cycles. Normally an intermediate cycle will run roughly 22 weeks. Well in our case the last two cycles were both stretched to 32 weeks by the Fed’s QE3 programs. As you can see in the next chart both intermediate cycles had 4 smaller daily cycles embedded within them. This is pretty unusual as most intermediate cycles only have 2 or 3 daily cycles nested within. The market is now in desperate need of a short cycle to balance out these two long cycles.

Next let’s examine the larger yearly cycle. As you can see out of the last 4 years, the larger yearly cycle bottom has occurred in the summer 3 times. The odds are favorable that the 2014 yearly cycle low should also occur in the middle of summer.

If the current intermediate cycle bottoms with the ongoing 2nd daily cycle, then we would get our yearly cycle low in early June. Right when it is expected.

On the other hand if somehow the Fed manages to stretch this intermediate cycle also, then the yearly cycle wouldn’t arrive until the end of summer/early fall.

Obviously I don’t give this scenario very favorable odds as I don’t believe we will see three stretched intermediate cycles in a row, especially now that the Fed is withdrawing the fuel to generate another stretched cycle.

What appears to be happening is that stocks have entered a 4 month consolidation phase ever since the Fed started tapering.

A consolidation of that size is likely to produce a rather large move once the consolidation resolves one way or the other. I’m in the camp, based on my cyclical analysis that believes it will resolve downwards over the next 4-5 weeks. Go to that first chart again to see my expectations for what I think is about to play out.

THE INFLATION HAS BEGUN

Just like the topping process in 2007/08 the rotation of inflation out of the stock market and into the commodity markets has begun.

Notice that since the first taper in December the stock market has stagnated and gone basically nowhere for the last 4 months. During that period inflation has begun to leak into the commodity markets. This is the same process that occurred as stocks topped in 2007/08.

We should see a mild deflationary period over the next 4-8 weeks and all assets should take a hit. But once that correction has run its course stocks should continue the stagnation phase as the cyclical bull continues what I expect will be a multi-month topping process. As this progresses the inflation that has been stored in the stock market will leak faster and faster into the commodity markets during the second half of the year.

The inspiration for this memo came from a report entitled Alpha and the Paradox of Skill by Michael Mauboussin of Credit Suisse. In it he talks about Jim Rutt, the CEO of Network Solutions. As a young man, Rutt wanted to become a better poker player, and to that end he worked hard to learn the odds regarding each hand and how to detect “tells” in other players that give away their position.

Here’s the part that attracted my attention:

At that point, an uncle pulled him aside and doled out some advice. “Jim, I wouldn’t spend my time getting better,” he advised, “I’d spend my time finding weak games.”

Success in investing has two aspects. The first is skill, which requires you to be technically proficient. Technical skills include the ability to find mispriced securities (based on capabilities in modeling, financial statement analysis, competitive strategy analysis, and valuation – all while sidestepping behavioral biases) and a good framework for portfolio construction. The second aspect is the game in which you choose to compete.

Mauboussin goes on to talk primarily about changes in the relative importance of luck and skill. But for me, what his words keyed first and foremost were musings about market efficiency and inefficiency. What they highlighted is that the easiest way to win at poker is by playing in easy games in which other players make mistakes. Likewise, the easiest way to win at investing is by sticking to inefficient markets.

Are Markets Efficient?

In well-followed markets, thousands of people are looking for superior investments and trying to avoid inferior ones. If they find information indicating something’s a bargain, they buy it, driving up the price and eliminating the potential for an excess return. Likewise, if they find an overpriced asset, they sell it or short it, driving down the price and lifting its prospective return. I think it makes perfect sense to expect intelligent market participants to drive out mispricings.

I also believe some markets are less efficient than others. Not everyone knows about them or understands them. They may be controversial, making people hesitant to invest. They may appear too risky for some. They may be hard to invest in, illiquid, or accessible only through locked-up vehicles in which some people can’t or don’t want to participate. Some market participants may have better information than others . . . legally. Thus, in an inefficient market there can be mastery and/or luck, since market prices are often wrong, enabling some investors to do better than others.

Remember the assumptions underlying market efficiency: the participants have to be objective and unemotional. Regardless of the market, few investors pass that test. How many are unemotional enough to resist buying into a fast-rising bubble, or selling in a crash when the price of an asset appears to be on the way to zero?

How, then, do I expect to find inefficiency?

My answer is that while few markets demonstrate great structural inefficiency today, many exhibit a great deal of cyclical inefficiency from time to time. Just five years ago, there were lots of things people wouldn’t touch with a ten-foot pole, and as a result they offered absurdly high returns. Most of those opportunities are gone today, but I’m sure they’ll be back the next time investors turn tail and run.

Markets will be permanently efficient when investors are permanently objective and unemotional. In other words, never. Unless that unlikely day comes, skill and luck will both continue to play very important roles.

Understand how Egypt’s constraints will affect the rest of the world

Gain a deeper understanding as we consider these important questions:

- What options will Egypt’s new president have to improve the country’s precarious financial situation? And how might the price of bread impact his longevity in office?

- How could politics in Cairo impact the global shipping industry, which routinely makes use of the strategic Suez Canal?

- How will Egypt, which is focused on its core as it struggles through the transition to democracy, ensure that the Sinai Peninsula does not become a safe haven for jihadists – and what will happen to the peace treaty with Israel if Cairo fails?

- How does Cairo’s approach to the Muslim Brotherhood make allies or enemies of neighboring states in North Africa and the Middle East?

- What might be the implications for Egypt’s future if a military-backed president can’t deliver on promises for the common good?

Presidential campaigns are in full swing in Egypt, where voting is scheduled by the end of May. It’s widely expected that the recently retired military chief, Field Marshal Abdel Fattah al-Sisi, will sweep to a landslide victory over his sole (and many say nominal) challenger – thus keeping the Egyptian military firmly in control of the government.

But even if there are no surprises at the ballot box, Egypt’s next president will have to walk a careful line, with little room to maneuver. In this country – the pivot of the Arab world – politics are not strictly local. The rest of the Middle East – and the world – will be watching the next steps in Egypt’s long journey with interest.

Stratfor

About Stratfor

At Stratfor, one of the things we study is the “butterfly effect:” the ways that political, economic and security developments, which often start as small, almost imperceptible shifts, can grow and ripple outward – impacting people, companies and industries far from the initial event. Our analysts make it their business to track and write about the small but meaningful events around the world, focusing on motivations, constraints and implications for the future.

Learn more about Egypt’s “butterfly effect” and who is likely to be touched by it with a Stratfor subscription. Get one year of complete access at 63% off and get The Next 100 Years, by Stratfor founder and chairman George Friedman, for free.

Last week we speculated that a decline in May would create an opportunity. We concluded: The near term prognosis looks cut and dry. Until proven otherwise the short-term trend is down. If that is confirmed in the coming days then let these markets fall to strong support before buying. The Ukraine-induced alleged safe haven bid for Gold could be starting to come out of the market. Regardless of the cause, the charts for the miners (and Gold) continue to urge caution as lower prices are likely ahead before the next major turn.

GDX and GDXJ (shown below) have had a very weak respite since the end of March. Both markets failed twice at their 50-day moving averages. The second failure occurred a few days ago at now declining 50-day moving averages. The markets reversed before even touching the moving averages. The path of least resistance is definitely lower.

Click image for larger view.

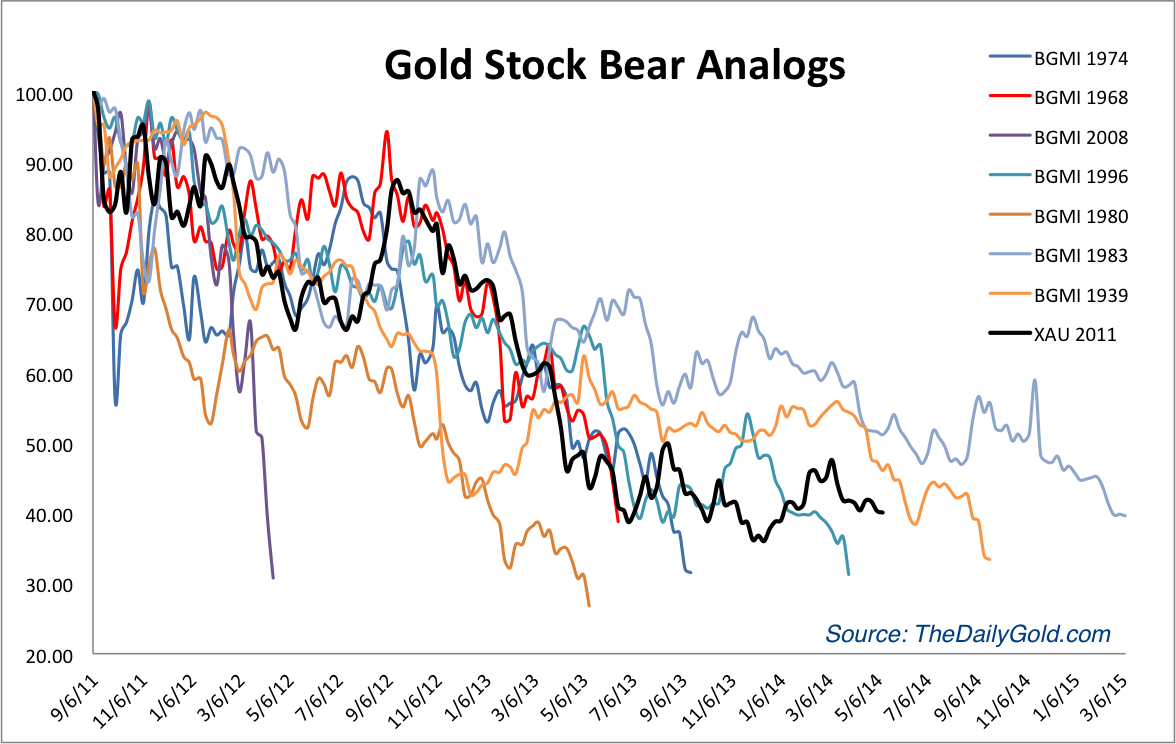

We strongly believe the next low for GDX and GDXJ will occur at or very close to the December 2013 lows and it will be a major low, similar to the June 2013 and December 2013 lows. Its presumptuous to say but not when you take into account the next chart, which many of you have already seen. This chart helped us spot the last two major lows. It may not tell us where the next low will be but it strongly argues that the next low will likely be the final low in this arduous bottoming process which is already in its 11th month.

Click Image for larger view:

So how could this next bottom play out? No one knows for sure but we’ll take a stab at it in this next chart and point out a few things. Note how the 200-day bollinger bands were far apart when GDXJ first peaked in 2011, yet tightened before GDXJ began to breakdown. Currently, the 200-day bands are far apart and GDXJ is yet to touch either side. Perhaps GDXJ will touch the lower band next and then a months later touch the upper band. These bands will need to pinch in before GDXJ attempts a major breakout. Volatility continues to be low as demonstrated by the ATR indicator. It is declining and near a multi-year low. Until that reverses, don’t expect any huge breakout in GDXJ.

Click Image for larger view:

With respect to our projection, let’s keep in mind that GDXJ rebounded 59% in two months in summer 2013 and recently surged 53% in less than two months (from late December to mid February). Our past historical work shows that the large cap miners usually recover 50% in four to five months after the bottom. Hence, a move for GDXJ from 30 to 50 (more than 50%) in four to five months would be inline with historical tendencies.

One security I am looking at is JNUG the 3x long GDXJ ETF. This is essentially an option on the already volatile GDXJ. JNUG is super volatile but the upside potential is tremendous. During that less than two month period in which GDXJ surged 53%, JNUG returned 210%! I am looking to buy that in the coming weeks when the downside risk becomes very low. I am also looking to buy several juniors I believe have exceedingly strong upside potential over the coming quarters and years. In any event, be patient over the coming weeks and let this final selloff run its course. If you’d like to know which stocks we believe are poised to outperform after this next low, then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com

The future will be decided in a race between global advances in demand for resources, complex technology and biotech innovation, and growing sovereign debt. In this interview with The Gold Report, Thoughts from the Frontline author John Mauldin points to the sectors that could benefit from the upside of improving world demand and the possible downside of a fiscal collapse in the geographic hot spots of China, Japan and Europe.

The future will be decided in a race between global advances in demand for resources, complex technology and biotech innovation, and growing sovereign debt. In this interview with The Gold Report, Thoughts from the Frontline author John Mauldin points to the sectors that could benefit from the upside of improving world demand and the possible downside of a fiscal collapse in the geographic hot spots of China, Japan and Europe.

The Gold Report: John, you’re one of the best-connected newsletter writers in the business. When you and I last chatted, the fiscal cliff was looming. Will the U.S. continue to lurch from one politically motivated crisis to another artificial crisis, or have politicians in D.C. learned their lessons?

John Mauldin: I guess it depends on which politicians you’re talking about. There are some politicians who get it. There are others who don’t. I think that government is still the solution to the problem. In the end, it’s going to take the equivalent of a knock on the side of the head by a two-by-four in the form of the bond market. Or voters could express their frustration with the direction of the country at the ballot box. That’s possible. Maybe the Republicans can realize that where they are is not where the voter population wants to be. They would have to change some of their programs to adapt to a younger generation and single women, because that’s where the Republicans are losing their message of fiscal conservatism, which is actually quite popular in those demographics. It’s all the other baggage that goes along with the Republican brand that is the problem. The same thing is true for Democrats. Their constituency is also fiscally conservative.

Perhaps after 2016, we could see a move to balancing the budget, which is really all we need to do. To do that, we have to figure out how much healthcare we want and how we’re going to pay for it. That’s going to take some compromises on both sides. I think both sides recognize that at the end of the day, if we don’t solve that question, then all the other questions become secondary.

TGR: You’re talking about compromise. The fiscal cliff was partially a crisis around using the raising of the debt ceiling to impact policy. Will that continue to be a flash point or have people decided that that’s not the way to fight?

JM: Democrats and Republicans alike have used the debt ceiling a handful of times in my lifetime. This last time it was politically not rational to use it, so it didn’t get used. But we’ll see it used again. There has to be some moment of crisis, something that forces people to compromise. Seemingly, we just can’t be rational and sit down like adults.

TGR: You are going to be speaking at the Strategic Investment Conference in San Diego along with Newt Gingrich and John Hunt. Your specialty is explaining the forces driving the global economy and investment markets. I have to ask the question everyone watching the upward climb of the indexes wants to know: Are we in an asset bubble? What is supporting it? What could pop it?

JM: I don’t think we’re in an asset bubble. We’re in a period of very high valuations, but it doesn’t look like bubble territory. We have seen serious bear markets start at this level, but there is nothing to say that it couldn’t go higher, and I’m not talking about in terms of valuations or price. What’s driving the market is sentiment, the story. What’s driving it is trust in the central bank. I’ve been writing for years that if there is a bubble, it’s the bubble in the belief that the Federal Reserve can actually control things, that it is actually in charge and that the markets themselves don’t have do anything but just follow the path of the Fed. That’s a lesson that always ends in tears. Central banks and policymakers can’t control things. When valuations get stretched too far, they snap back. When it comes to popping this current valuation expansion, it could be a China slowdown or international debt challenges. Bill White, former chief economist for the Bank for International Settlements, who is now at the Organisation for Economic Co-operation and Development, is arguing that we spent the last five years trying to increase demand in the economy when we should have been repairing the balance sheet. We haven’t addressed the primary cause of the crisis, which was out-of-whack balance sheets. We haven’t reduced the debt. We haven’t been reducing leverage. There are ways to deal with debt, but none of them are pleasant. None of them are going to make people happy. The reality is we still have too much debt and we haven’t dealt with it, especially in Europe. Europe is still a problem.

German banks are significantly overleveraged; they have a lot of bad debt on their books. We are a few sovereign debt crises away from a serious banking crisis there. Think about this. We have allowed Spanish, Italian and Greek bond rates to fall to precrisis levels, and yet the debt/ GDP ratios for every one of those countries are significantly higher. Spain and Greece have 25% unemployment and 50% youth unemployment. France’s GDP is shrinking, not rising. I think that Europe could be a serious problem when markets realize some European countries can’t pay their debts and start asking for higher interest rates. And it accelerates rapidly. It’s the old Ernest Hemingway line, when one of his characters asks how the other went bankrupt. And the guy said, well, slowly, then all at once.

TGR: We have been talking about the market as if it’s one thing, but are commodities, technology, banking and energy all reacting differently, both in the rise and what sounds like the inevitable fall? Will some do better than others?

JM: Yes, they all do act differently. Not everything is going to fall. There are always stocks that create value, businesses that have figured out a new approach. There are things that are solid. We are still going to buy Coca-Cola, soap, food. We’re going to need to consume energy. The price that we pay for a dollar’s worth of earnings may change, but the underlying true value of the company will still be there. Sometimes we just have to recognize that we need to accumulate assets that are going to be valuable at the other end of the crisis.

Governments are going to have spastic-type movements if they want to monetize debt as they try to minimize the effects of their bad policies. And it doesn’t work. The cure central banks and governments have come up with is quantitative easing (QE). That makes the problem worse and can lead to catastrophic problems.

TGR: How close are we at this point in Europe or in the U.S. to a catastrophic problem?

JM: We could see another crisis in Europe within the next few years. The U.S. is still some time away. Japan is in the process of destroying its currency. I’m hedging a significant part of my mortgage in yen, and I’m buying 10-year options on the yen with out-of-the money strike prices because I think the yen is going to go to 200 over the next 10 years. It may go much higher. Currency markets are terrible in Japan. Japan has been called a widowmaker for very good reasons. I think Japan is committed to a serious process of monetization. It could be putting as much as $8 trillion ($8T) into the world’s economy through QE. That would be the equivalent of the U.S. printing $32T for its balance sheet. At 250% debt/GDP, it has painted itself into the mother of all bad corners. If you’re sitting with a long bond position entirely in Japan, you’re not going to be very happy at the end of this 10-year process. If you are short the yen and you’re sitting in the U.S., you’re going to be able to buy a Lexus cheaper than you can buy a Kia. Sony TVs are going to get cheaper and cheaper. Their robots might be cheaper. So it might be a good thing from our point of view, but not from the Japanese retiree’s point of view.

The same problem could be lurking in the U.S. if we don’t get our act together. I’m still optimistic that we will. We did it in the 1990s. Who knew we’d be nostalgic for Clinton and Gingrich? We could make the same decisions again. I’m less confident that France and Italy will be able to make those decisions. I think there could be some problems.

TGR: If we’re looking at a looming sovereign debt crisis in Europe and Japan, what asset classes should U.S. investors be considering?

JM: My view is that given the rise of energy production, we’re going to see the dollar get stronger, not weaker. I know people are talking about the end of America, the end of treasuries—I don’t believe that’s going to happen. If we go back into a QE program in a few years, we could see an inflationary period at the beginning of that cycle. But that’s off a ways.

U.S. investors do need to watch out for disruptions in the rest of the world. That could reduce the consumption of commodities. That’s not a very good prospect if you’re in South Africa, Canada, Australia or Brazil, one of the commodity-producing countries.

TGR: John, you’ve named China as one of the biggest macroeconomic problems in the world today. Is the problem the debt from recent expansion, or a slowdown in the expansion?

JM: The answer is, probably both. Since the end of World War II, we have had the Italian miracle, then the Latin American miracle and the Japanese miracle, followed by American, Irish and Spanish housing miracles. All those ended in rather spectacular busts. China’s miracle has the same two components: rising leverage and excess construction. China’s leaders are very cognizant of this. The proposals they’ve made are some of the most far-reaching since Deng Xiaoping. They could really be dramatic change-makers if they do what they say they’re going to do, but that path is going to produce slower growth. The Chinese have to figure out how they are going to restructure their debt while protecting consumers and depositors. They seem to be doing that. But it’s a very difficult path, because they’ve expanded their debt by massive amounts, which historically hasn’t ended well. Now they are trying to be proactive about it rather than just pushing it to the end. So I’m hopeful that it’s just a slowdown, but I’m cautious in saying it could be more if they make a policy mistake or something happens out of the ordinary.

TGR: Even with the slowdown, China is growing. It’s just not growing as fast. Wouldn’t that be good for stocks?

JM: When I was in South Africa, I met business owners who had factored in 7% and 8% growth to their business plans. Chinese growth has fallen pretty seriously. The world has gotten used to its built-in models.

TGR: There has been a lot of news recently about conflict in the South China Sea and Ukraine. To what extent do you think that war might be a black swan that will impact markets?

JM: God, I hope not. War would certainly affect markets, potentially significantly. I just hope cooler heads will prevail. I can’t see the U.S. going to war over Ukraine. We’ll just increase sanctions. Will that hurt Russia? Yes. It’s already hurting. Money is fleeing the country. Stock markets are down. Russia seems to be willing to pay the price to have Crimea. Maybe it’s going to try to figure out how to absorb part of eastern Ukraine directly or as an autonomous region so that it doesn’t have to worry about its border.

TGR: John, you’re always very positive about technology and the impact technology will have on our lives. What technological advances are you most excited about now?

JM: I continue to be mostly excited about biotech, maybe because that is what’s going to personally affect me. We got rid of smallpox, diphtheria and polio—those were big changes. We’re going to see those types of events happening every year now. I think there’s potential for a cure for cancer on the horizon, for liver disease, for chronic heart disease, for arthritis, Alzheimer’s. Those things are coming soon. What those dramatic changes mean for many of your readers is that they need to plan to live a lot longer.

Energy is also exciting. After a couple more decades of improving solar technology, sun power will be cheap enough to replace oil. In the next 20 years, we’re going to become natural gas exporters. That will do great things for the economy.

Most of the developed world is still trying to rise up through the second industrial revolution. They’re coming at it much faster, but they have a long way to grow. As they go through that, they’re going to want more protein, more metals. The growth in biotechnology is a function of Moore’s law. We’re seeing more change. We’re going to see, in the next 10 years, some of the most incredible advances in human history.

We’re going to see changes in computing power. I’m talking to you on a mobile phone that is 1,000 times more powerful than the phone I had 15 years ago. In another 15 years, I will be talking on a phone that will be 1,000 times more powerful than the one I have today. If the trend keeps going, it will be the size of a button, but the possibilities will only be limited by the scope of our imagination. Facebook and Google are buying high-altitude balloons and solar-powered drones with advanced communications systems that can track anything. Everyone will be connected, not just in the U.S. but throughout the Middle East and India. Those kids are going to have access to systems that will allow them to improve their lives and their families’ lives.

The amount of change that we’re going to see is simply an accelerating trend. That’s in juxtaposition to the amount of growth we’re seeing in sovereign debt, which is destructive. The question becomes: Can government and central banks destroy wealth faster than technology and humans create it? And it’s going to be a race. In some countries, citizens will lose. Some countries’ citizens are going to win. I think each country, each region, has to be responsible for deciding that it wants to be in the winner’s category.

TGR: John, thank you for your insights.

John Mauldin is a world-renowned economist and financial writer of the New York Times best-selling books Bull’s Eye Investing, Just One Thing, and Endgame. His most recent book is The Little Book of Bull’s Eye Investing. Mauldin’s free weekly e-letter, Thoughts from the Frontline, is one of the most widely distributed investment newsletters in the world. Launched in 2000, it was one of the first publications to provide investors with free, unbiased information and guidance.

Mauldin is also the chairman of Mauldin Economics, a company created to provide individual investors with his big-picture thoughts on the global economy, as well as actionable investment and trading strategies typically deployed by institutional money managers on behalf of their high-net-worth clients, but at a fraction of the cost.

Mauldin is the president of Millennium Wave Advisors, an investment advisory firm registered with multiple states. His track record of success vetting and consulting with money managers spans over three decades. His passion is to understand the world of economics, investment, politics and science, and to determine how it may all come together in the future. As a highly sought-after market pundit, Mauldin is a frequent contributor to publications such as The Financial Times and The Daily Reckoning and is a regular guest on CNBC, Yahoo! Daily Ticker and Breakout, and Bloomberg TV and Radio.

DISCLOSURE:

1) Karen Roche and JT Long conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provide services to Streetwise Reports as employees. They own, or their families own, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services.

3) John Mauldin: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair