Signs Of The Times

“The End of Snow?”

– The New York Times Sunday Review, February 7

“Over Two Thirds of Contiguous USA Covered With Snow”

– WUWT, February 7

“1 in 4 Americans Unaware That Earth Revolves Around The Sun”

– Survey of 2,200 by the National Science Foundation, February 14

(It is uncertain that the survey included the NYT Editorial Board)

“We don’t see a broad-based buildup in leverage.”

“Asset prices generally do not appear to be out of line with traditional metrics.”

– Testimony, Janet Yellen, February 11

“The shadows are growing in the corporate bond market as investors turn to derivatives. An increasingly illiquid cash bond market is behind the shift.”

– Financial Times, February 11

“Investors have been warned by Fitch that losses from the next leveraged default cycle may be significantly in excess of previous cycles.”

– Financial Times, February 14

* * * * *

Perspective

In what seems to be bureaucratic ritual, Yellen’s public statements may vary from her private comments. The Fed head is not going to holler “Fire” in the equivalent of a crowded theatre. Nevertheless, we think the Fed chair is sincere.

Pity.

Perhaps her info on developing strains in the credit markets and asset valuations is a month or so behind the action.

Yesterday’s hit to the bond market was accompanied by the comment that traders had read the latest Fed minutes and realized that “they” did not know what they were talking about.

These pages have been hammering central banking for decades. Quite likely the treasury market was poised for change and the utterance by the Fed became the catalyst. Whatever, it is constructive criticism of an agency whose sole purpose is to provide unlimited funding for another experiment in unlimited government.

In Ukraine the “Cold War” between the governing classes and the ruled is turning to physical rebellion. Hopefully, this does not become a civil war. It need not as all the folks want is self-government. More links with Europe would be a step towards freedom. Ooops, we have referred to the seat of Euro-government as “Moscow on the Maastrich”. Perhaps the natural movement for freedom in Ukraine could spread to the rest of Europe. Maybe even to Democrat-controlled states and cities in America.

The violence in Kiev is spreading to other Ukrainian cities and it reminds of the Prague Spring uprising in 1968 and of the Hungarian uprising in 1956.

Political violence in Europe in the 1920s and into the early 1930s was between national socialists and international socialists. Each was dedicated to authoritarian central planning.

The conflict in Ukraine is vastly different – it is between authoritarians and those who value freedom. The latter were successful in bringing down the Berlin Wall in 1989 and today’s movement should eventually win.

Another reform movement could sweep the political world.

In the financial markets it would include profound criticism of the Federal Reserve System.

Credit Markets

At the first of the month, the bond future reached resistance at the 134 level, which was the high in November. The surge was enough to drive the Daily RSI to 75, which compares to the momentum of 73 reached with the bond high in May.

This surge was to vulnerability and all that was needed was a “news” hit. The catalyst was the Fed minutes, and the reversal was associated with reversals in stocks, lowergrade bonds, copper, gold and silver.

HYG (high-yield) and investment-grade (LQD) accomplished Outside Reversals. Liquidity, indeed, is diminishing. Essentially, this was from new highs on a move that has not had a significant correction since the “mini-panic” in June.

Long treasuries have been correcting and the 50-Day ma (about 130) should provide support.

Credit spreads (JNK:TLT) led recent uncertainties in peaking at the end of December and taking out the 50-Day a week later. Then it plunged to the 200-Day which was enough to prompt the rebound. Now it is attempting to test the 50-Day line from below.

Emerging bond spreads (EMB:TLT) plunged to below the 200-Day and bounced back to that level and has been struggling. At 1.02 now, falling below 1.01 would resume the decline. The “high” or maximum narrowing was reached at the end of December.

Of interest, is that the initial hit looks quite like the reversal in June 2008.

We are keeping in mind that when troubles start in lesser exchanges they eventually hit the financial centre. We are also keeping in mind the unprecedented recklessness by the senior central banks in arbitrary pursuit of perfection.

Commodities

The rotation into commodities has been working well.

For some, such as coffee, the rally has been spectacular. Bottoming in November coffee led the play and has become, well, over-caffeinated.

The price was 1.01 in November and it took two months to rally 19 cents – yesterday’s gain was 19 cents – to 1.73. The Weekly RSI jumped to 81 which is a snick off of that reached at the top of the bull market in April 2011.

Clearly a remarkable short squeeze. Wonder if it includes “fair trade” coffee?

In November we mentioned that one of the coffee ETFs was JO, which seems an appropriate way to play the opportunities. The short squeeze is massive and the spike up will be followed by a spike down. Will it reverse this week, or next? Who knows.

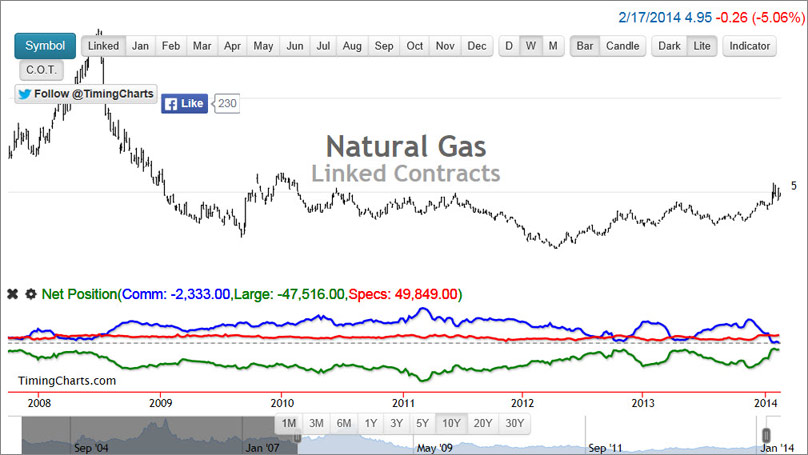

Natural gas suffered a paradigm shift as it crashed from 13.69 in 2008 to 1.90 in 2012. The initial rally made it to 3.50 in early 2013 and the correction was to 3.13 in August. Obviously, natgas is in a huge “weather” rally. However, the Weekly RSI is as high as reached in 2008 and the price is at the resistance level of 6.11.

Crude’s action has been strong enough to drive the Daily RSI to 73, which compares to 75 reached with the brisk rally to the 110 level last summer.

Yesterday’s “Peak Oil” study was essentially written a week ago and being very longterm allowed seasonal room for the top. This week’s action in hot commodities suggests it may be sooner than later.

Base metals (GYX) rallied from 330 to 362 in early January and fell to 331. This is a good test of the low and the advance has made it to 346.

Agricultural prices (GKX) became very oversold at 340 in January and jumped to 375 yesterday. Of interest is that the Daily RSI got to 79, which compares to 83 reached with the spectacular drought rally of 2012.

Sometimes various markets can explode in March-April and we have referred to the phenomenon as the “Silly Season”. This seems to be happening, perhaps somewhat early.

In some examples the “rotation” has been fabulous and the spike up will be followed by a spike down. Then stability.

The rally in base metals was good and the one for agriculturals has been very good. A setback to stability seems likely.

In 2011 our “Momentum Peak Forecaster” called for a surge in speculation to complete and be followed by a cyclical bear. The high was 370.

The key low for the CRB was 272 in November and this was tested in early January at 272. The rally to 301, yesterday, was outstanding. The Daily RSI has clocked a huge swing from 22 to 85, which is quite like the drought rally of 2012.

The CRB could decline to the 275 level and trade in a range for most of the year.

Link to February 21, 2014 Bob Hoye interview on TalkDigitalNetwork.com:

http://talkdigitalnetwork.com/2014/02/gold-and-commodities-advance-strongly/

– Deflated by the CPI, margin debt exceeds levels reached in 2007 and in 2000.

– It took some five years for margin debt to peak in the Tech Bubble of 2000.

– It took some five years for margin debt to peak in the Great Bubble of 2007.

– Although the latest posting is for December, it has been five years since margin debt was at a cyclical low.

– Margin debt is close to a cyclical high.

PIVOTAL EVENTS

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

Albert Einstein – “I know not with what weapons World War III will be fought, but World War IV will be fought with sticks and stones”

Albert Einstein – “I know not with what weapons World War III will be fought, but World War IV will be fought with sticks and stones” HardAssetsInvestor: What’s your view on the recent surge in natural gas above $5/mmbtu?

HardAssetsInvestor: What’s your view on the recent surge in natural gas above $5/mmbtu?