Timing & trends

….everything you buy today, you can buy cheaper within the next 2-3 years.

David McAlvany : We have talked about liquidity. We have talked about the implications of rising asset prices. Yet selectively, we are seeing stocks break down. You pointed out, very presciently last October, that Apple looked very much like RCA in the 1920s and could be poised for a correction. Of course, we have had the correction, close to 40%. Today, there are a growing number of stocks that are breaking down in the same manner, 30%, 50%, even 80% down in a short period, and that’s while the major indices are moving higher. What does that tell you, as someone familiar with the markets for 20, 30, 40 years now?

Marc Faber : When you have that many stocks breaking down every day, it’s not the symptom of a market that is bottoming out, it’s the symptom of a market that is already relatively high, where the bull market is already rather mature. That is what it tells me.

And by the way, I would like to add one more comment about what you said about liquidity. I’ve been in this business for a number of years, to be precise, 40 years. In the 1970s people went around the Middle East and said, “Oh, the Arabs, they have so much liquidity.” And at that time, I used to travel frequently to Kuwait, and they had a stock market, and at the peak of the Kuwaiti stock market in 1979-1980, the Kuwaiti stock market had a larger capitalization than the German stock market, and everybody always said that there was so much liquidity, it will never go down.

Fast forward: Japan in the late 1980s. Everybody told me there is so much liquidity, stocks in Japan will never go down. And then again, in the late 1990s, there is so much liquidity, NASDAQ will never go down. And for real estate the same, and so forth, and now I hear the same story. At the peak of the market, you always have lots of people who tell you how much liquidity there is around, but liquidity comes and goes, and you don’t know exactly what will happen. And I really don’t know whether the Dow Jones will peak out today, or in three months, or six months, or even a year. But we are moving into a speculative phase where my sentiment is that everything you buy today, you can buy cheaper within the next 2-3 years.

– in a recent interview with McAlvany

Click here to watch the full interview >>>>>>

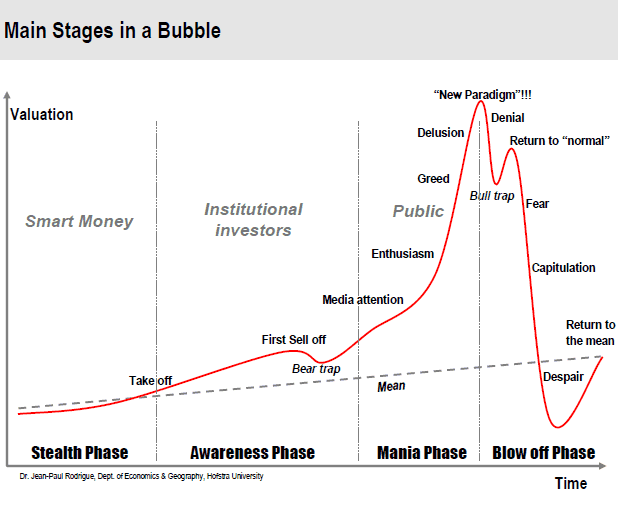

5 Steps Of A Bubble

…..Ed Note: Read about bubble Characteristics, The Dutch Tulip Mania, Minsky’s Theory of Financial Instability and so much more in this article HERE

It has been amusing listening to the hypocrisy from Brussels regarding the leverage in Cyprus.

Jeroen Dijsselbloem, president of the eurogroup led the charge that Cyprus had an unsustainable problem with deposits over 700% of GDP.

Here is a little perspective courtesy of the Financial Times.

Somehow we are supposed to believe that 7-1 ratio of deposits to GDP is a problem but the 22-1 ratio in Luxembourg is not. And what about the 4-1 ratios in France and the Netherlands?

What sunk Cyprus now rather than later was Cyprus was dumb enough to be in Greek bonds.

So why did Cyprus stay in Greek bonds so long? The answer is Cypiot banks were foolish enough to believe ECB president Jean Claude Trichet when he insisted there would be no haircuts on Greek bonds.

…..read more about the Timing the Axe on Spain and Italy HERE

Cyprus: As The Barn Door Closes

“As it turns out, these same oligrachs may have used the one week hiatus period of total chaos in the banking system to transfer the bulk of the cash they had deposited with one of the two main Cypriot banks, in the process making the whole punitive point of collapsing the Cyprus financial system entirely moot.”

“As it turns out, these same oligrachs may have used the one week hiatus period of total chaos in the banking system to transfer the bulk of the cash they had deposited with one of the two main Cypriot banks, in the process making the whole punitive point of collapsing the Cyprus financial system entirely moot.”

“While ordinary Cypriots queued at ATM machines to withdraw a few hundred euros as credit card transactions stopped.” Meanwhile, “The two banks at the centre of the crisis Laiki, and Bank of Cyprus – have units in London which remained open throughout the week and placed no limits on withdrawals.”

“Just brilliant.”

“In every sense of the word.”

……more on the Russian theft of their own money HERE

(Last 2 comments written by Kate the just announced WINNER of the BEST CANADIAN BLOG (scroll down at the link for Kate’s winning entry in the 13 th Annual Worldwide WEBLOG AWARDS)

The Next Price Spike Could Be In Food

Is The Junior Potash Sector Hitting Rock Bottom?

Population growth combined with potential inflationary effects could lead to increased demand for food. Increasing populations with declining arable land per capita will force farmers to boost yield using the key ingredient potash.

Potash or potassium salts are amazing fertilizers. They make the plant stronger and improves output. Potash helps the physical condition of the crop boosting vitality. It helps a plant’s immunity to withstand drought, infection and parasites. Do not forget that potash is also used in drilling, building materials, paper, pharmaceuticals and other products.

Continuing interest especially out of Asia, India and Brazil for a secure long term supply could boost global demand to 75 million tons by 2020 and boost the need for junior potash developers. These countries have major supply demand imbalances.

The global population increases 300-400 million people every five years. Rising emerging economies require more well rounded diets consisting of higher meat based and crop intensive diets.

Arable land is declining per capiita….

(an example of a food price spike below, go to the link above to reak more)

In a previous column, I showed you how the war cycles turn violently higher this year. I also addressed the issue of war, and its implications for the markets, at the Weiss Global Wealth Summit in January.

It’s a topic that no one likes to talk about. Yet I’ve studied the history and Cycles of War in detail. And I do not like what I see happening now in the least bit.

As I’ve also previously told you, I do not expect a war between China and the United States, nor between China and Taiwan, nor Russia and the United States.

But it’s also clear to me that there are many seeds of war now being sown, in many different areas.

First, we have the rising military might of China, and its territorial expansion into the South China Sea and the Spratly Islands.

Beijing wants control over the vast oil reserves in those regions, which could turn out to be the biggest in the world. Beijing also wants to exercise control over the vast, hugely important shipping lanes in the South China Sea, another reason we should all be concerned.

And make no mistake about it. China is becoming a military giant. It now has the largest number of active-duty troops in the world, at 2.28 million.

It has 7,400 tanks. 44 attack helicopters. 71 submarines. 2004 combat-ready aircraft. And a brand-spanking new, state of the art aircraft carrier.

And Beijing is upping its military budget over 10 percent this year, increasing its military spending by $106 billion.

Second, we also have rising cyber espionage all over the world, much of it instigated by China and North Korea. The media calls it “hacking.” I call it “spying.” Either way, there’s a good chance we may one day, in the not-too-distant future, see a full-scale cyber war break out.

Third, we have Iran and Israel, the Middle East. Always a problem, my models show this year could be the year that war breaks out in the Middle East. The Arab Spring is a prelude, one that has sown the seeds of war and uprisings and rebellions all over the Middle East.

But the area that worries me the most is none other than Europe, where the demons of previous wars are still very much alive.

Europe is a cesspool of rotten politics, inept leaders,

and a monetary system that was flawed from the outset.

And worse now, is that the latest Cyprus developments are directly planting the seeds for a civil war in Europe.

Europe is going to splinter apart at the seams. I am sure of it.

The mere gall that northern European leaders have to even suggest that Cypriots’ bank accounts be raided is something no one should take lightly. It shows how desperate the situation is in Europe … and how desperate the so-called “Troika,” has become.

The European Commission (EC), the International Monetary Fund (IMF), and the European Central Bank (ECB) are all clamping down hard on weaker European peripheral countries with austerity programs and now, threats of confiscation …

When in reality, they have no one to blame but themselves for the mess that Europe is in.

Yes, countries such as Greece, Cyprus, Portugal and others were profligate. But the stronger countries of Europe — Germany especially — are equally to blame. They are the countries that practically forced the weaker European countries to adopt the euro, putting them in a position where they could not compete against the stronger economies of Germany and France …

And they are the countries that rammed loans, that are now unpayable, down the throats of those countries.

It’s gotten so bad in Europe, the rise of neo-Nazi parties is astounding.

In Greece, the neo-Nazi “Golden Dawn” party has risen in popularity from 0.3 percent of the Greek people polled in 2009 to as much as 7 percent late last year. A 23-fold increase in just three years.

Germany’s Angela Merkel is now being portrayed in many European publications in Nazi garb.

Germany’s Angela Merkel is now being portrayed in many European publications in Nazi garb.

From the north of Europe to the Mediterranean in the south, fascist and neo-Nazi parties are growing at an alarming rate, gaining over 15 percent of the vote in recent local elections in many countries.

As EU Home Affairs Commissioner Cecilia Malmström recently stated, “Not since World War II have extreme and populist forces had so much influence on the national parliaments as they have today.”

Will Europe See a Civil War?

Unless the Troika backs off the weaker, heavily-indebted countries, which is not likely, yes, I believe Europe is headed toward massive civil unrest and war.

Another aspect that worries me, is Russia. According to Moody’s ratings agency, Russians have $19 billion in Cypriot banks, nearly as much as Cyprus’ entire GDP. Russian banks have an additional $12 billion invested and have loaned another $40 billion to Cypriot companies of Russian origin.

That’s just Cyprus. While there are no clear estimates on how much Russian money, legally or illegally, is spread out over Europe, it’s safe to assume there are boatloads. In 2012 alone, an estimated $56 billion left Russia, much of it going into Europe.

Vladimir Putin is up in arms over the crisis in Cyprus. He will not stand idly by while Russian money is at risk in Europe.

Keep in mind that Russia largely controls the European energy sector. The European Union depends on Russia for more than 32 percent of its crude oil, and nearly 39 percent of its natural gas needs.

Many countries in Europe depend upon Russia for 100 percent of their energy needs.

Germany depends upon Russia for as much as 36 percent of its energy needs.

If Putin feels Russian financial losses in Europe are unjust, I don’t doubt for one minute that he would threaten to retaliate by “turning the lights out” in Europe.

Sadly, based on my work on the war cycles and what’s happening now in the next phase of the great financial crisis and Europe’s sovereign debt crisis, war and massive civil unrest in many parts of the world is a very real threat. And it’s already starting to impact the financial markets.

It’s a major geo-political reason why the dollar is now breaking out to the upside, precisely as I have been forecasting.

And, it’s a major reason behind my forecast for a much higher U.S. equity market. Frightened capital from all over the world will pour into the U.S. and emerging markets of Asia.

To play the long side of the dollar for a strong rally this year, consider investing in thePowerShares DB US Dollar Index Bullish Fund ETF (UUP).

Per my previous suggestion in my February 11 Money and Markets column to purchase a small core position in the SPDR DJ Industrial Average ETF (DIA) at $134 or better: Raise that price to buy now on a pullback to the $141 level.

If and when filled, place a stop to reduce risk at $105, on a good-till-cancelled basis.

Lastly, despite the prospects for massive civil unrest around the world and even war this year, commodities are not yet out of the woods and are instead still largely in a disinflationary trend. That includes the precious metals.

The chief reason is the stronger dollar. Plus, the austerity measures and rising taxation that’s occurring around the globe. That’s sending most money to the sidelines or into liquid equity markets.

While gold will shine again someday soon, it’s still not time to back up the truck on the precious yellow metal.

Best wishes, as always, stay tuned …

Larry

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair