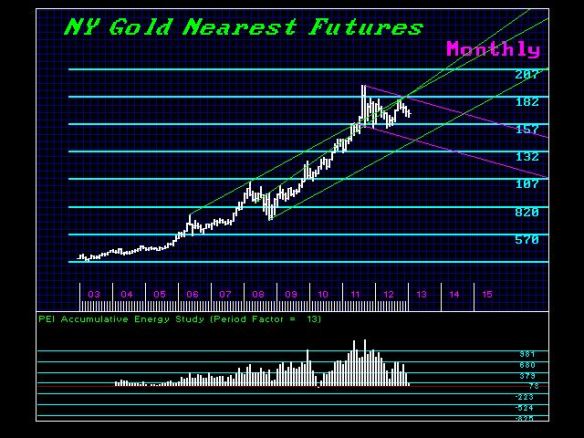

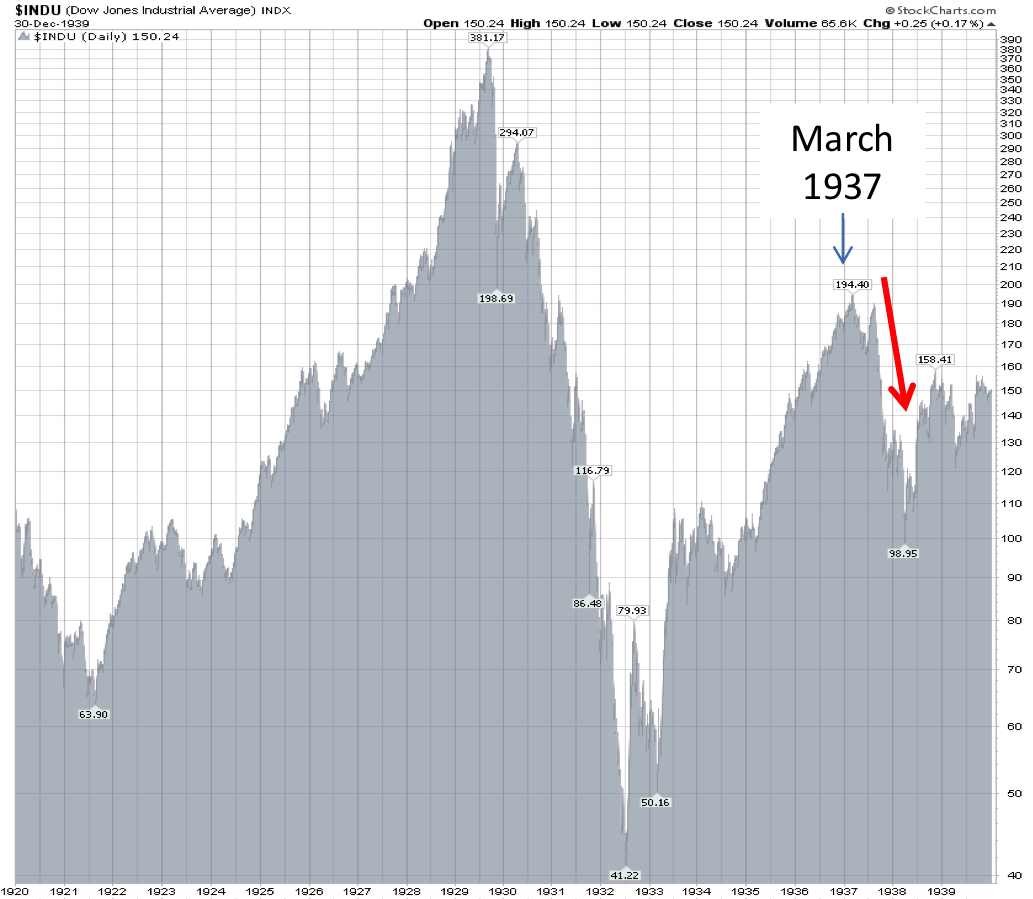

“a replay of 1937—a 50% market decline after a big rally from the low in 1932”

Quotable

“All through time, people have basically acted and reacted the same way in the market as a result of: greed, fear, ignorance, and hope. That is why the numerical (technical) formations and patterns recur on a constant basis.” – Jesse Livermore

Commentary & Analysis

Déjà vu; is it 1937 all over again?

We are not sure if we get a replay of 1937—a 50% market decline after a big rally from the low in 1932– but it feels a bit eerie to say the least. Now we have an extremely “overbought” stock market…false belief in a cyclical recovery…troubles in Europe…and rising tensions in Asia. I think a simple question is in order: Is risk skewed to the upside or downside? You know my answer.

Many attribute the big tax increase that took effect in 1937 as a major factor leading to another slowdown in the economy. Sound familiar? Big tax increases are biting into aggregate demand in 2013 thanks to the infinite wisdom of our Maximum Leaders who choose to punish initiative under the guise of “fairness.” It is to laugh! But it is what it is and we’ve seen it all before.

Quotable “Advertising is the rattling of a stick inside a swill bucket.”- George Orwell

Commentary & Analysis

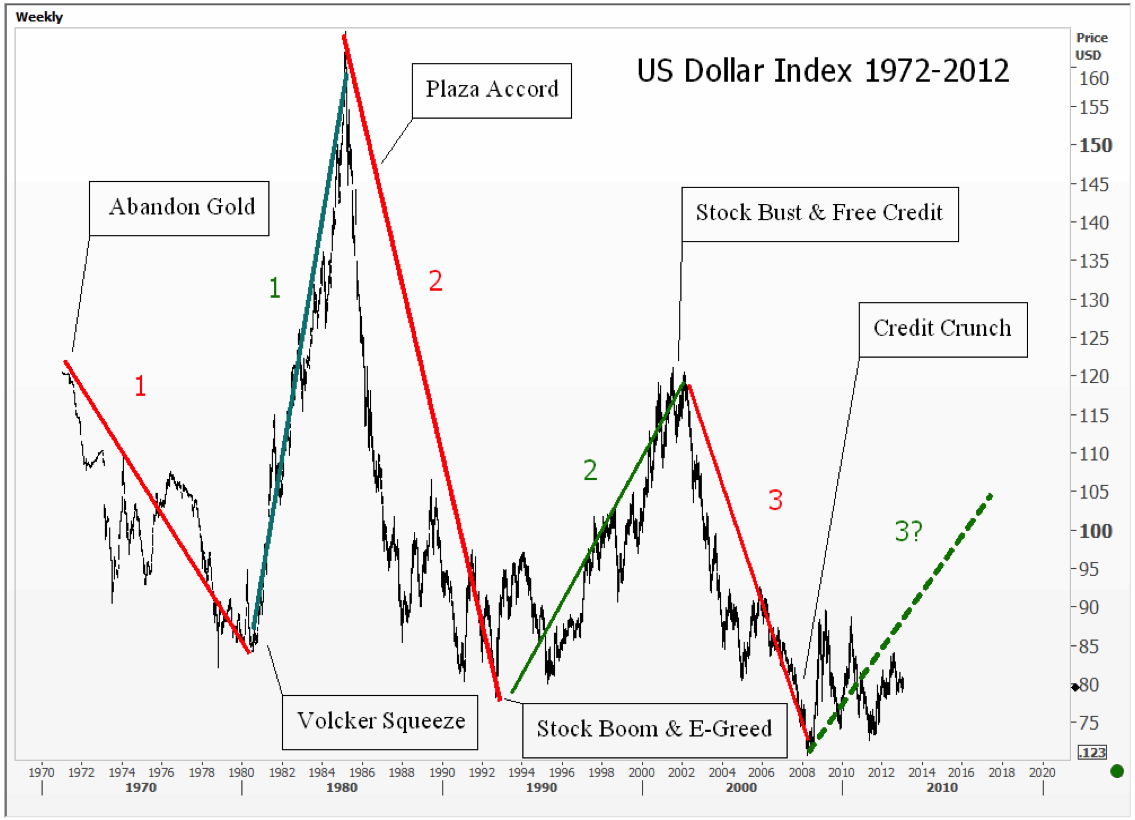

Thank you China for validating our dollar bull market call.

I saw a promotional campaign several months ago from a newsletter company promoting a currency conference to be attended by various currency “experts.” The lead, if you can believe it, was, “Get the Hell Out of the Dollar.” It’s your typical scare tactic nonsense in order to sell services and push people into the one-trick pony multi-currency deposit accounts in order to prepare for the “plunging dollar.”

Remember how these multi-currency banks were loading their clients into the Icelandic krona to grab that “high yield” because it was the US dollar that was going to crash and burn from the rising global risk. Well, if you remember (and the multi-currency bankers wish you wouldn’t) it was the Icelandic krona that crashed and burned. I think if investors decide to “Get the Hell out of the Dollar,” they may be sorry. Why? Because even China is expressing some love for Mr. Greenie and citing the same fundamental rationales we have shared in these pages.

Black Swan’s long held call is the US dollar is in a multi-year bull market and it was triggered by the sea change global macro event called the credit crisis. If you peruse the chart below you will notice, with the gift of hindsight and my labeling, that prior multi-year trend changes in the US dollar index were accompanied by major global macro events.

Based on the US $ Index, the dollar bottomed in March 2008 and we are in the third bull market since President Nixon closed the gold window back in 1971 forcing major currencies to float against one another. [I believe the US dollar index has completed its third bear market in March of 2008; which incidentally was about seven years in duration as where the prior two bear markets.]

From Mr. Ambrose Evans-Pritchard, “China loves the US dollar again as America roars back:”

“Jin Zhongxia, head of the central bank’s research institute, said America’s energy revolution and export revival had shaken up the global landscape and would lead to a stronger dollar over time. ‘The dollar’s global dominance will continue,’ he said.”

- Dr Jin said the world was moving to a “1+4” system, with the greenback serving as the anchor of global payments, supplemented by “four smaller reserve currencies” – the euro, sterling, yen and yuan.

- Compared with the euro area, the dollar zone has much greater resilience to shocks.

- Citigroup said lower energy imports and the revival of chemical industries would cut the US current account deficit by three quarters, eliminating a key cause of dollar weakness.

I may be a stretch to expect America to “roar back.” But relative to its competitors the US could be the destination for an inordinate amount of foreign direct investment, not to mention the “on shoring” that is taking place (manufacturers moving back to the US from China).

Of course China may not love the dollar at all. But at this stage in the cycle, jawboning the dollar higher would help China in two ways: 1) It would help China’s exporters at the margin, as they are fighting for a lot of the same export market with the US; and 2) relatively lower commodities prices in dollar terms would also support China’s domestic- demand transition.

[Last year China and the US were on the top of the list of exporters, with an 8.0% and 4.5% increase in exports, respectively. The rest of the developed world countries and BRICs had negative export growth in 2012. Notably, German exports were off 4.5% in 2012.]

It has been a very choppy trade in the US dollar index:

Rule #1: Anything can happen.

But net-net the dollar has worked higher even though gold blew off to a new high in August 2011(suggesting the fiat problem is much more than just the US dollar). And given my view: 1) the euro crisis isn’t over, 2) Japan will succeed in weakening the yen further, 3) the British pound seems be a favorite short on the “stagflation” trade, and, 4) the commodity dollar complex seems to be breaking down a bit, I think it is fair to say it may not be time to “Get the Hell Out of the Dollar.”

It is vital to understand that what we face is by no means the plain vanilla version of governments just printing into hyperinflation. These people are fighting back as is ALWAYS the case with core and major economies. The German hyperinflation took place AFTER a revolution with a unstable government that lacked credit. When there is “credit” then government FIRST tries to keep the game afoot and that means the bankers threaten they will collapse unless debt is serviced. This is why the FIRSTresponse is all out financial war against the people.

It is vital to understand that what we face is by no means the plain vanilla version of governments just printing into hyperinflation. These people are fighting back as is ALWAYS the case with core and major economies. The German hyperinflation took place AFTER a revolution with a unstable government that lacked credit. When there is “credit” then government FIRST tries to keep the game afoot and that means the bankers threaten they will collapse unless debt is serviced. This is why the FIRSTresponse is all out financial war against the people.