Timing & trends

“In the last 7 months alone the People’s Republic of China has added more gold to their reserves – over 500 tons – than the entire holdings of the European Central Bank. They aren’t alone.”

“Russia’s President Vladimir Putin has been aggresively investing into the precious metal over the last five years – spending some $500 million monthly as he diversifies his country’s assets out of Dollars and Euros. Currently, 9% of Russia’s reserves are held in gold.”

This, of course, begs the question: why?

According to the World Gold Council, Russia has more than doubled its gold reserves in the past five years. Putin has taken advantage of the financial crisis to build the world’s fifth-biggest gold pile in a handful of years, and is buying about half a billion dollars’ worth every month.

No one else in the world plays global power politics as ruthlessly as Russia’s chilling strongman…

Putin’s moves may matter to your finances, because there are two ways to look at gold.

On the one hand, it’s an investment that by most modern standards seems to make no sense. It generates no cash flow and serves no practical purpose. Warren Buffett has pointed out that we dig it out of one hole in the ground only to stick it in another, and anyone watching this from Mars would be very confused.

But there’s another way to look at gold: As the most liquid reserve in times of turmoil, or worse.

The big story of our era is not that the Spanish government is broke, nor is it that Paul Ryan apparently feels the need to embellish his running record.It’s that the United States, which has dominated the world’s economy for several lifetimes, is in relative decline.

We will soon be the first people in two hundred years to live in a world not dominated by either Pax Americana or Pax Britannica. This sort of changing of the guard has never been peaceful.

The declines of the Spanish, French and British empires were all accompanied by conflict. The decline of British hegemony was a leading cause of the First and Second World Wars.

What will happen as the U.S. loses its pre-eminence?

Maybe this will turn out better than similar episodes in the past. Maybe the Chinese will embrace an open society and the rule of law. If you believe that, there is probably no reason to hold any gold.

On the other hand, we may be about to enter a much more turbulent and dangerous era of power politics and international competition.

Source: Market Watch [via Ulsterman Report]

….read the entire article HERE

“Markets are going in the opposite direction of the world economy. If you’re positioned fundamentally, you’re positioned against these clowns.”

– John Burbank, Passport Capital, on the latest news from Europe’s central bank

Three headline events each tell us something important about global markets. More and more, government is a big player in markets — creating distortions, along with pitfalls and opportunities.

Item No. 1: The market says one thing. Earnings say something different.

The stock market rallied last week on news that the European Central Bank will “save the euro.” Basically, the ECB said it stands ready to buy bonds in unlimited quantities. To finance this, the ECB will essentially print money. This follows talk about how the US Federal Reserve stands ready to goose markets further — by printing more money.

In essence, the actions and chatter of central bankers are what are driving the rally since that little bottom we had in June after the market sold off about 9%.

Earnings are not driving the rally, that’s for sure.

The S&P 500 just registered a 0.8% growth rate in earnings for the second quarter, according to today’s Financial Times. The consensus for the third quarter is negative for the first time in three years. The ratio of companies saying they’d miss third-quarter forecasts versus those that that said they’d meet them was 3-to-1. That is the worst ratio since the fourth quarter of 2008, which came on the heels of the Lehman Bros. bust. “Historically, we have only seen numbers like this during times of recession,” says Christine Short of S&P Capital IQ (which tracks earnings) in today’s FT.

Yet the market hits a four-year high.

Take-away: Trust earnings. The market can go only so far on the gas of central banking. Don’t believe prices reflect what’s happening with the underlying companies. The market is too optimistic.

Item No. 2: Gloom spreads in China despite the best efforts of officials.

The FT reports that a third of publicly traded Chinese companies reported cash outflows for the second quarter. One headline seems to say it all, “Cash Squeeze Tightens Abroad Sections of China.” Another says, “Fragile China.”

Local governments have amassed piles of debt. The FT says these debts represent one-quarter of Chinese output. Yet China continues to announce ambitious plans to build railways and highways.

But one of the most-damning things I’ve come across on China hit my desk over the weekend. I seldom link to other articles in full, but this one is worth a read when you get a chance:

“In China, Silvercorp Critic Caught in Campaign by Police”

It is the story of a researcher in China who police arrested — and detained — because he works for a fund manager who writes negative reports on Chinese companies. (The researcher is a Canadian citizen, by the way, yet sits in a Chinese jail on flimsy evidence and no due process whatsoever. I can’t believe the Canadian government lets that stand.)

Chinese companies have had lots of fraud issues, as you may know. Investors have uncovered discrepancies and outright frauds in US-listed Chinese companies. This sent the stock of many such companies tumbling.

This in turn, hurt these companies’ ability to tap Western markets for more money, which hurts their ability to pay local taxes. And that hurts the local governments who labor under a pile of debt. It’s all an ugly, corrupt circle.

Take-away: If you are in China, you have to write positive reports or you get arrested. That’s the message here. There is no respect for independent research in China. There is no value on transparency. In fact, the organs of the state work against such things.

So in a reversal of my normal preference for “boots on the ground” research, I say you can’t trust anything coming out of China. Oh, and if you own Silvercorp, dump it. Avoid China as a general rule.

Of course, this has broader implications, as we’ve talked about before, especially for commodity markets (because China is such a large consumer of commodities). If the Chinese market is really propped up by government stimulus, then commodity markets are too.

This warning does not apply to precious metals, which I think are moving higher.

Item No. 3: The US government is selling its AIG stake.

Front page on The Wall Street Journal: The US government says it is going to sell $18 billion in AIG stock. This will cut its stake in the big insurer by half.

This is a reminder that the US government is still in the business of owning major stakes in big companies. It still owns stakes in Fannie Mae and Freddie Mac — which the government spent $188 billion on. It still owns big stakes in GM and in Ally Financial, which it spent $68 billion on.

These are companies that would have otherwise gone through the bankruptcy process — as would have a long list of institutions. What the bailouts did was preserve the same bad actors that got us into trouble in the first place. The corrective tonic of bankruptcy never got to do its full work.

I’m not going to get into the politics of it, or even the economics of it. I’m a practical man in these pages. We have to take the world as it is, not how we wish it would be. We have to do the best we can with the markets we find ourselves in.

So as unseemly as it sounds, my take-away from this story is one of opportunity.

Even after its rally, AIG still trades for about 56% of book value. Bruce Berkowitz at Fairholme owns a big chunk of it and calls it his best idea. Berkowitz is not immortal. He’s taken some licks and his reputation is not what it was. But I think he makes a good argument for AIG.

Here is what he wrote in his second-quarter letter:

“Our best idea remains AIG common (35% of the fund) with a reported book value of $57 per share. There are few occasions when systemically important franchises sell for half of book value and are profitable. This is one of those times.”

Book value is now $60 per share. On the Fairholme Funds website is a 21-slide case study on AIG from February. Though a bit dated, it still holds. AIG sells for less than 60% of book today. Yet peers trade for 80-100% of book. And the long-term average for the sector is 130% of book.

AIG is solidly profitable now. What’s holding it back, at least in part, is the fact that the government is looking to sell. As the market absorbs $18 billion-plus in sales, this will probably tamp down AIG’s share price.

Take-away: The US government still has large stakes in several financial companies. It is still a source of great distortions. However, as it sells these stakes, the overhang from its ownership will disappear. So too might the discounts these stocks trade for. AIG looks like a double as these things sort themselves out. (Ed Note: Do not consider this a Money Talks recommendation. Money Talks does not make stock recommendations on this unpaid portion of our website because we don’t know the financial make-up of those reading the information).

It’s a weird market we’re in. I can’t recall a time when government actions seemed to drive prices as much as now. I don’t like it. But there are ways to navigate your portfolio through the mess.

Regards,

Chris Mayer

for The Daily Reckoning

“Most of you reading this expect inflation in the years ahead, right? Well, I don’t. In fact, I am firmly in the deflation camp.”

A Decade of Volatility: Demographics, Debt, and Deflation

Just think about it. What has happened after every major debt bubble in history? What happened after the 1873-74 bubble? Or after the 1929-32 bubble? Did prices inflate or deflate?

We got deflation in prices… every time.

This time around, with the latest bubble peaking in 2007/08, the outcome will be exactly the same. There is deflation ahead. Expect it. Prepare for it.

But the bubble-bust cycle that history has allowed us to see is not the only reason I’m so certain we’re heading for deflation and a great crash ahead. I have other, irrefutable evidence…

For one, there is the most powerful economic force on Earth: demographics. More specifically, the power of the number 46. You see, that’s the age at which the average household peaks in spending.

When the average kid is born, the average parent is 28. They buy their first home when they’re 31… after they had those kids. When the kids age into nasty teenagers, the parents buy a bigger house so they can have space. They do this between the ages of 37 and 42. Their mortgage debt peaks at age 41. And like I said, their spending peaks at around 46.

From cradle to grave, people do predictable things… and we can see these trends clearly in different sectors of our economy, from housing to investing, borrowing and spending, decades in advance.

To watch a video version of this presentation by Harry Dent,

please click HERE:

This demographic cycle made the crash in the ’30s and the slowdown in the ’70s unavoidable. Now it is happening again… with the biggest generation in history – the Baby Boomers.

Consumer spending makes up more than two-thirds of our gross domestic product (GDP). So knowing when people are going to spend more or less is an incredibly powerful tool to have. It tells you, with uncanny accuracy, when economies will grow or slow.

Why Deflation Is the Endgame

Think of it this way: the government is hellbent on inflating. It’s doing so by creating debt through its quantitative easing programs (just for starters). But what’s the private sector doing? It’s deflating.

And the private sector is definitely the elephant in the room. How much private debt did we have at the top of the bubble? $42 trillion. How much public debt did we have back then? $14 trillion.

That looks like a no-brainer to me. Private outweighs public three to one. And the private sector is deleveraging as fast as it can, just like what happened in the 1870s and 1930s. History shows us that the private sector always ends up winning the inflation-deflation fight.

Now, I will concede that this is an unprecedented time. Today governments around the world have both the tools and the determination to fight deflation. And they are desperate to keep it at bay because they know how nasty it is (they, too, are students of history).

How bad is it? Think of deflation like what your body would do with bad sushi. It would flush it out as fast as possible. That’s what our system is trying to do with all the debt we accumulated during the boom years. It’s what the system did in the 1930s. Back then we went from almost 200% debt-to-GDP to just 50% in three years. It hurt like hell. The government doesn’t want this painful deleveraging.

The problem is, the longer the government tries to fight this bad sushi, the sicklier the system becomes. I know this because it’s what happened to Japan…

Japan’s bubble peaked in the ’80s. When the unavoidable deleveraging process began, the country did everything in its power to stop it. How is Japan doing today, 20 years after its crash? It is still at rock bottom. Its stock market is still down 75%.

Japan has gone through everything we’ll go through in the next few years. Does Japan have an inflation problem? That’s a rhetorical question. Did its central bank stimulate frantically? Also a rhetorical question.

Think of it another way: what is the biggest single cost of living today? Is it gold? Oil? Food? It’s none of these. It is housing. And what is housing doing? Dropping like a rock. It can’t muster a bounce, despite the lowest mortgage rates in history and the strongest stimulus programs anywhere… ever.

The Fed is fighting deflation purposely. It will fail.

Why the Fed Will Fail in All Its Efforts

There is simply no way the Fed can win the battle it’s currently waging against deflation, because there are 76 million Baby Boomers who increasingly want to save, not spend. Old people don’t buy houses!

At the top of the housing boom in recent years, we had the typical upper-middle-class family living in a 4,000-square-foot McMansion. About ten years from now, what will they do? They’ll downsize to a 2,000-square-foot townhouse. What do they need all those bedrooms for? The kids are gone. They don’t visit anymore. Ten years after that, where are they? They’re in 200-square-foot nursing home. Ten years later, where are they? They’re in a 20-square-foot grave plot.

That’s the future of real estate. That’s why real estate has not bounced in Japan after 21 years. That’s why it won’t bounce here in the US either. For every young couple that gets married, has babies, and buys a house, there’s an older couple moving into a nursing home or dying.

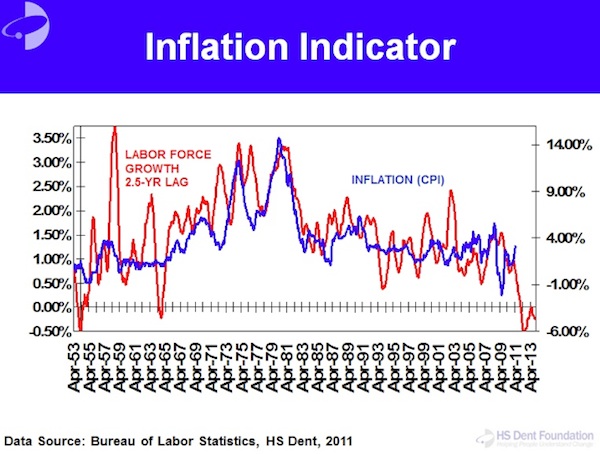

I watch this same demographic force move through and affect every other sector of the economy. The tool I use to do so is my Spending Wave. This is a 46-year leading indicator with a predictable peak in spending of the average household.

Here’s how it works: the red background in the chart above is the Dow, adjusted for inflation. The blue line is the spending wave, including immigration-adjusted births and lagged by 46 years to indicate peak spending. If you ask me, that correlation is striking.

The Baby Boom birth index above started to rise in 1937. It continued to rise until 1961 before it fell. Add 46 to 1937, and you get a boom that starts in 1983. Add 46 to 61, and you get a boom that ends in 2007.

Today demographics matters more than ever because of the 76 million Baby Boomers moving through the economy. That’s why I don’t watch governments until they start reacting in desperation. Then I adjust my forecasts accordingly.

Don’t Hold Your Breath for the Echo Boomer Generation

But all this talk about Baby Boomers inevitably births the question: “Surely the Echo Boom generation is coming up right behind their parents. They’ll fill the holes, right?”

Let me make this clear. If I hear one more nutcase on CNBC say, “The Echo Boom generation is bigger than the Baby Boom,” I might go ballistic. They are wrong. The Echo Boomer generation is NOT bigger than the Baby Boom generation. In fact, it’s the first generation in history that’s not larger than its predecessor is, even when accounting for immigrants.

It’s not all doom and gloom, though. We will see another boom around 2020-23. But for now, all the Western countries will slow, thanks to the downward demographic trend sweeping the world. Some are slowing faster than others are. For example, Japan is slowing the fastest (it actually committed demographic kamikaze, but that’s a discussion for another day). Southern Europe is next along in its decline. Eastern Europe, Russia, and Asia are following quickly behind.

Which brings me back to my point: there is no threat of serious inflation ahead. Rather, deflation is the order of the day. The Fed thinks it can prevent a crash by getting people to spend. To that I say, “Good luck.” Old people don’t spend money. They bribe the grandkids, and they go on cruises where they just stuff themselves with food and booze.

Do you know how to tell if you’re buying a car from an older person? It’s going to be ten years old and have only 40,000 miles on it. They drive 4,000 miles a year. They just go down the street to get a Starbucks coffee and a newspaper. Then they go back home. How do you know you’re buying a car from a soccer mom? It’s driven 20,000 miles a year, carting the kids around all day… to school, soccer practice, whatever. This is the power of demographics.

So let me tell you what causes inflation. It’s young people. Young people cause inflation. They cost everything and produce nothing. That’s inflation in people terms.

Why did we have high inflation in the ’70s? Because Baby Boomers were in school, drinking, spending their parents’ money. While this was going on, we experienced the lowest-productivity decade in the last century.

Do you remember the 1970s? We had worsening recessions as the old Bob Hope generation began to save more while the Baby Boomers entered the economy en masse… at great expense. It costs a lot of money to incorporate young people, raise them, and put them into the workforce.

Then suddenly, in the early ’80s, like some political genius did something brilliant, the economy started growing like crazy, and inflation fell. You know what that was? That was the largest generation in history transitioning en masse from being expensive, rebellious, young people to highly productive yuppies with young new families. It was the move from cocaine to Rogaine.

The correlation between labor force growth and inflation is crystal clear…

When lots of young people come into the labor force, it’s inflationary. When lots of old people move out of the labor force and into retirement, it’s deflationary. Right now, where is the highest inflation in the world? It’s in emerging countries. Do they have more old people or young people? They have more young people.

We saw it in the 1970s, we see it in emerging markets, and we’ll see it ahead as the Baby Boomers head off into the sunset. First, there was inflation. Ahead is deflation. No doubt about it.

Harry Dent, the editor of Boom & Bust, has put together a free report for John Mauldin’s readers, called: Survive and Prosper in This Winter Season: Take These Steps Now… Before Dow 3,300 Arrives. You can access this free report by clicking on this link:http://www.boomandbustinvestor.com/reports/current/BoomandBustInvestor_WinterSeason.pdf

Like Outside the Box? Then we think you’ll love John’s premium product, Over My Shoulder. Each week John Mauldin sends his Over My Shoulder subscribers the most interesting items that he personally cherry picks from the dozens of books, reports, and articles he reads each week as part of his research.

Share Your Thoughts on This Article

I fail to see the merit in Mario Draghi’s approach to the euro crisis. Buying “unlimited amounts” of bonds from indebted sovereign euro countries and then “sterilizing” the printed money is simply not going to work.

First, Germany’s Bundesbank, by far the most powerful national central bank in the euro zone, is not squarely behind the deal. That’s not a good sign.

Just hours after Draghi announced the plan, Germany’s Finance Minister Wolfgang Schaeuble also jumped into the fray, warning that he stood against the European Central Bank’s (ECB) bond-buying plan.

Second, Draghi plans on sterilizing the money printed by his bond-buying. That means the ECB will issue its own debt to mop up the money it’s printed. So there will be no net increase in the monetary base, which is dis-inflationary … at a time when precisely the opposite is needed, a dose of inflation.

Third, the sterilization will cause even more problems. The only countries that can afford to buy ECB bonds to mop up excess money printing are the rich euro-zone countries, mainly Germany and France.

Think that through. It means the bonds the ECB does buy, from failing sovereign nations, will put money in their coffers … while the bonds the ECB issues will take money out of the coffers of the richer nations.

Do you think Germany and France will like to see their liquidity tightened while their suffering neighbors get all the benefits? I don’t think so!

Fourth, by driving down short-term yields on sovereign bonds in heavily-indebted and busted euro-zone countries, the ECB will effectively shorten those countries’ debt maturities.

With those busted countries falling deeper and deeper into a depression, that will merely serve to make their debt loads worse in the longer run, because debt will have to be rolled over more frequently.

Fifth, the indebted nations of Europe that will get the aid will have to get their fiscal houses in order by complying with strict policies put out by the ECB. If they don’t, then the ECB backs away from buying and supporting their bonds.

Guess what? The ECB-imposed austerity measures will merely serve to make the debt crisis worse. And that’s assuming countries like Spain, Italy, Portugal, etc. will be able to comply with strict austerity measures in the first place.

That’s highly unlikely. Just look at how Greece has gone down the tubes with austerity measures that, in turn, forced it to go hat-in-hand time after time for more bailouts.

Put another way, if Spain, Italy, Greece etc. can’t comply, they lose the ECB backing. And if they do comply, their economies simply crater more.

In short, there is no way Draghi’s plan is going to work. The markets, most of which have rallied sharply on the news, are headed for one of the biggest disappointments I’ve ever seen. The gap between hope and reality has never been wider.

I see more trouble ahead, too. This Wednesday, Germany’s Federal Constitutional Court will decide the legitimacy of the European Stability Mechanism, the funding vehicle for bailout money. There’s a chance it will decide against it, which would put Draghi’s plan in jeopardy.

In addition, our Fed meets this Thursday and the majority of investors and traders are expecting Ben Bernanke to announce another round of money-printing.

They’re going to be sadly disappointed. Bernanke will do no such thing. While he will give the usual rhetoric that the Fed stands ready to print, and perhaps may give a few more clues about it, I strongly believe that the Fed will not initiate any money-printing until after the elections, at the earliest, and more likely, not until early 2013.

Bottom line: I don’t like what I’m seeing in the markets. It’s not just my gut, not just my interpretation of the news or fundamentals either.

- While the S&P has marched to a new recovery high, it remains largely unconfirmed by the advance/decline ratio, by volume, and by the Dow Transports.

- While gold has rallied to just above $1,700, it has thus far failed to take out my system resistance at the $1,727 level, let alone monthly resistance at $1,740 to $1,750.

- While silver has exploded higher too, it has also failed to take out monthly resistance at the $34 level.

Meanwhile, the euro remains below monthly resistance at the 1.28 level and the dollar is holding monthly support at the 80 level in the nearby Dollar Index futures. Crude oil has failed to get above important resistance at the $100 mark.

I see a giant trap about to slam shut. A lot of investors are going to get hurt. Don’t be one of them.

Until next time …

Best wishes,

Larry

P.S. From ECB meetings to the upcoming Fed meeting to the never-ending saga of European sovereign-debt problems, September is filled with uncertainty. But it’s also filled to the brim with opportunity. And in my Real Wealth Report, I help you seize the profit potential from the opportunities these events create. Activate your risk-free trial subscription by simply clicking here now!

“Thursday’s announcement of a bond buying program on the part of the ECB was expected but welcomed news nonetheless in the precious metals markets. Gold and Silver have been leading the charge over the last few weeks as the powers that be in Europe, and here in the U.S. have talked about taking action to stimulate their economies. With more money printing now virtually guaranteed, traders are looking for inflation hedges, and of course are turning to the metals. This action has pushed the price of gold back above $1700/ounce.

The recent buying push has also caused both gold and silver to break their long term downtrend lines. Gold’s downtrend line has been in place for a year and silver’s for 16 months. The action this week has also pushed each over its 50 week moving average (the blue line). This is bullish action, however in each case the stochastic (circled) is in overbought territory, which means that we can expect a pullback of some sort before the uptrend resumes. As money printing becomes the remedy of choice for worldwide economies, the appeal of gold and silver will only grow. This party is just getting started as we are now entering the positive season for gold and silver prices.” – Mark Leibovit via his VR GOLD LETTER Published This Morning September 7, 2012

Gold “A Bit Overcooked” Ahead of US Nonfarms Data, “Bazooka” from ECB “Is Just a Can Kick Down the Road”

by Ben Traynor BullionVault

SPOT MARKET prices for buying gold rose to $1698 an ounce Friday morning, in line with where they started the week, while stock markets also rose, following yesterday’s announcement of the European Central Bank’s bond market intervention plan.

US Treasuries fell, while commodities were broadly flat, with the exception copper, which posted gains. Copper traders are now more bullish than at any time since last October, according to a survey by newswire Bloomberg, which sites “mounting speculation” about central bank stimulus measures, such as a third round of quantitative easing (QE3) from the Federal Reserve.

A day earlier, gold hit its highest level in six months at $1713 per ounce Thursday, although it fell following the publication of a stronger-than-expected ADP Employment Report, a precursor to today’s official August nonfarm payrolls release.

“There is definitely long liquidation going on after the ADP number,” says one trader in Singapore.

“People spent the whole of yesterday buying gold and it is a bit overcooked up here. Now we have good data and the market is struggling to see how it can get a bad [nonfarm] payrolls data.”

“The consensus expectation for today’s nonfarm payrolls is 130,000 [jobs added in August],” says a note from Rabobank this morning, “although in reality it may [now] have been revised upwards…the final clues for today’s nonfarm payrolls were positive, at least for the economic recovery, not for the chances of QE3.”

Prices to buy silver meantime climbed to $32.40 per ounce this morning – on course for a 2% weekly gain – while on the currency markets, the Euro rose to its highest level in more than two months, a day after ECB president Mario Draghi announced the new Outright Monetary Transactions program, aimed at tackling the Eurozone crisis by buying distressed Eurozone sovereign bonds.

“OMTs will enable us to address severe distortions in government bond markets which originate from, in particular, unfounded fears on the part of investors of the reversibility of the Euro,” Draghi told Thursday’s press conference.

There will be “no ex-ante limits” on the size of OMTs, Draghi added.

“This is your bazooka,” Organisation for Economic Cooperation and Development chief Jose Angel Gurria told the Financial Times yesterday, having used that phrase earlier in the week when urging the ECB to act.

OMTs will target debt of up to three years in maturity, Draghi said, and will also be fully sterilized – meaning the ECB will sell other securities to absorb the liquidity created.

In addition, OMT purchases will be subject to conditionality, meaning governments would have to enter into some form of bailout program with at least the possibility of bond purchases by the European Financial Stability Facility, or its scheduled permanent successor the European Stability Mechanism. Governments that fail to fulfill their bailout commitments could face a withdrawal of ECB support.

Benchmark 10-Year Spanish bond yields fell to their lowest level since April this morning, dipping below 5.7% – two percentage points below their high in July. Italian 10-Year yields hit a six-month low at just over 5%.

Neither Italy nor Spain has formally requested a bailout, although Spain’s government agreed a €100 billion credit line in June to finance the restructuring of its banking sector.

Germany’s Constitutional Court is due to rule next Wednesday on whether or not the creation of the ESM is at odds with German law.

“Investors still view gold as a non-paper currency and I don’t think anything the ECB said or did yesterday has changed people’s psyche,” says Simon Weeks, head of precious metals at Scotia Mocatta.

“Really they just kicked the can down the road.”

In Switzerland meantime, the central bank may be considering a de facto devaluation of the Swiss Franc, moving its price floor for the Euro-Franc exchange rate from SFr1.20 to SFr1.30, FT Alphaville reports.

Over in China, the world’s second-biggest gold buying nation behind India last year, Beijing has approved 1 trillion Yuan worth of infrastructure spending, equivalent to around $158 billion.

“With clear signs of a worsening slowdown of economic growth, China’s central government has finally taken real actions,” says Bank of America Merrill Lynch economist Lu Ting.

“They are clearly stepping up the infrastructure investment push to help boost confidence and revive growth,” adds Zhang Zhiwei, chief China economist at Nomura in Hong Kong.

“We believe the decision for the Chinese government to intensively announce these projects over the past two days signals a significant change in its policy stance from the incremental and reactive approach to a more decisive and proactive approach.”

In November 2008, China announced a 4 trillion Yuan stimulus package as a response to the global financial crisis.

The deputy governor of India’s central bank meantime has again cautioned Indians against buying gold, following comments he made in July.

“Because interest rates are very low, people are investing in gold,” said KC Chakrabarty on Friday.

“But the poor should never invest in gold for whenever they have purchased gold, it either lands up in the temple or in the hands of the moneylender or, at the most, it may be given away during a daughter’s marriage.”

Earlier this week, key figures in India’s bullion industry expressed fears that gold import duties may be hiked for the third time this year.

Thinking of ? Make it safer, cheaper and easier with BullionVault…

(c) BullionVault 2012

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair