Timing & trends

September is often a bad month for the stock markets, historically speaking, and this year it could be especially turbulent. In addition to all the uncertainty about the weak US economy, there is uncertainty about what the Fed may do just ahead and what, if anything, will be done to address Europe’s recession and debt crisis. In addition, there is the looming presidential election which no doubt will go hyperbolic this month.

To begin this discussion, with all of its variables, let’s take a look at the precarious position the US stock market is in based on recent price action. The Dow Jones Industrial Average failed once again to break out decisively above overhead resistance at the 13,250 level in August.

This is the third time this year that the DJIA has failed at this level, and that could be a bearish development on its own – before we take into account a number of additional potentially negative possibilities that could show up this month. Let’s consider them.

The global stock markets are looking for answers on three big fronts in September:

- Can European leaders and policy makers put into action the promises made this summer for dealing with the debt crisis?

- Will the sputtering US economy get another dose of monetary stimulus on September 13 at the conclusion of the next monetary policy meeting?

- Will the next batch of data show China’s economy getting better or worse? Some worry that China’s economy will be the next to fall into a recession.

Any one of these issues could undermine investor confidence to the point that it triggers a new bear market in stocks. All of this comes against the backdrop of a very close US presidential election that could determine the country’s fiscal path for years to come. And all of this follows the month of August when trading volume in the markets was exceptionally weak, perhaps in anticipation of fireworks this month.

Central bankers in both Europe and the US will play a pivotal role in September, as we will see if their hints of more monetary easing – which kept stocks aloft during the summer months – come true.

There is a meeting of the European Central Bank this Thursday (Sept. 6), and the markets are looking to see whether the ECB will cut rates. More importantly, the markets will be watching to see if European leaders will approve purchasing sovereign debt of troubled countries.

This issue takes center stage following ECB President Mario Draghi’s recent comments that the ECB would do “whatever it takes” to defend the euro. Draghi pledged to buy short-dated Spanish and Italian bonds one month ago, and now the market hopes to see him add details about the size and scope of such purchases and any other “non-standard” forms of easing that might be on the table.

The European Commission is expected to have a proposal on a banking union by next Tuesday (Sept. 11), ahead of the EU leader’s summit in December. The ECB is expected to then have the supervisory role, and the proposed new “European Stability Mechanism” – if Germany’s court backs it – could then be used to recapitalize European banks.

That decision is expected to come on Wednesday of next week (Sept. 12), when a German Constitutional Court will decide whether the proposed new European bailout fund, the ESM, is legal. If approved, the much larger ESM would succeed the current limited EFSF bailout fund. Many also believe that this month could be the time when European leaders decide once and for all whether or not to issue “Eurobonds” which Germany vehemently opposes.

Finally, there is a critical decision that will likely come this month in regard to Greece. Earlier this year, Greece formally requested additional time for implementing further austerity measures. The European Commission, the ECB and the IMF – the so-called “Troika” – are expected to render a decision before the end of September.

Germany and France have refused to extend the time frame thus far, and Athens is scrambling to make cuts. The Troika will be assessing whether Greece will ever be able to get out from under its onerous debt burden, which is 160% of its GDP. It remains to be seen what the Troika will decide. If the answer is no, Greece could decide to default and exit the euro. We all know what that will mean for the global stock markets!

Then there’s the key Fed Open Market Committee (FOMC) policy meeting that also begins next Wednesday, which could determine whether the Fed will conduct a new round of easing this fall. Fed Chairman Ben Bernanke, in his Jackson Hole speech Friday, again said the Fed could do another round of easing, if necessary, giving the markets fresh commentary to consider as that important meeting approaches (more on this below).

Before the Fed meeting next Wednesday is this Friday’s key release of the August employment report, the day after President Obama’s big convention speech. The August employment report is the last big data point for the Fed to consider ahead of the upcoming FOMC meeting. It is also one of three final employment reports ahead of the US election, and political analysts expect employment to be a big factor for voters.

Ahead of Friday’s report, economists expect that just under 120,000 jobs were created in August, following 163,000 new jobs in the July report. That could be a big disappointment which could send the stock markets lower.

Finally, there are concerns on the part of some that China’s economy will fall into recession next year. I don’t happen to believe that China will fall into recession just ahead. China’s economy has slowed this year, but growth is still believed to be somewhere north of 3-4%, maybe even 5%.

These are just some of the key unknowns that will likely be resolved – or not resolved – this month. If you think about it, there are no clear-cut answers for any of these problems. And the equity markets could react negatively, no matter what decisions are reached or not reached.

Now let’s turn our eyes to the latest economic reports from the US.

The Economy Sends Mixed Signals in August

The Commerce Department revised its estimate of 2Q GDP growth from 1.5% to 1.7% (annual rate), following growth of 1.9% in the 1Q. The latest report was right in line with the pre-report consensus and confirms once again that economic growth is anemic.

The Consumer Confidence Index unexpectedly plunged from 65.4 in July to 60.6 in August, the lowest since last November. The pre-report consensus was for an increase to 66.0, so the dive was a surprise. Yet the University of Michigan Consumer Sentiment Index actually increased in August to 74.3 for reasons unknown. However in that same survey, 50% said their current situation is worse than it was five years ago. That tells the real story.

The Consumer Confidence Index, which was based on a survey conducted August 1 – 16 with about 500 randomly selected people nationwide, underscored that anxiety. The Index is widely watched because consumer spending accounts for 70% of GDP. It has remained well below the 90 reading that indicates a healthy economy – a level it hasn’t touched since the recession began in December 2007.

In the latest reading, the percentage of consumers expecting business conditions to improve over the next six months declined to 16.5% from 19% the month before. Those expecting more jobs in the months ahead declined to 15.4% from 17.6%, while those expecting fewer jobs rose to 23.4% from 20.6%.

On the manufacturing front, the ISM Index dipped below the key 50.0% mark in July, falling to 49.8%. This morning, the Institute for Supply Management reported that the Index fell further in August to 49.6%. Any reading below 50.0% in the Index is an indication that the economy is contracting.

On the unemployment front, initial claims for unemployment benefits rose to 372,000 in last Thursday’s report, up from 368,000 the prior week. The August unemployment report will be out this Friday, and the consensus is that it will remain unchanged at 8.3%.

Fortunately, not all the economic news of late has been bad. Durable goods orders in July were better than expected at 4.2%, up from 1.6% the month before. Retail sales were better than expected in July at 0.8%, up from -0.7% in June. Industrial production rose 0.6% in July, up from 0.1% in June. Factory orders were also better than expected in July. The Index of Leading Economic Indicators rose to 0.4% in July, up from -0.4% in June.

On the housing front, there was also some good news. Existing home sales rose to the highest level in over two years in July at 4.47 million units. New home sales also matched a two-year high in July, up 3.6% to 372,000 units. New permits for building homes rose 6.8% in July to 812,000 units, the highest rate since August 2008. Housing starts, on the other hand, unexpectedly fell 1.1% to 746,000 units in July.

While there was some good news in the economic reports released in August, the big drop in consumer confidence has to be concerning. Consumer spending, as we all know, is the big driver of the economy, and the significant drop in August is not a good sign.

Where Does the US Economy Go From Here?

The US economy is lousy, we can all agree on that. But what does it look like beyond this year? What follows is an updated snapshot of consensus economist estimates for GDP growth (quarter over quarter %) and the unemployment rate going out to the 1Q of 2014. The consensus estimates come from Bloomberg surveys of dozens of economists on a regular basis.

As shown in the first chart below, GDP growth is expected to still be below 2% in the 1Q of 2013. Economists are then expecting GDP to grow by 2.4% in 2Q 2013, 2.6% in 3Q ’13, 2.8% in 4Q ’13 and 2.95% in 1Q 2014. Unfortunately, 3%+ GDP growth is not expected at any point in the next year and a half.

Along with sub-3% GDP growth, economists aren’t expecting a significant drop in the unemployment rate over the next year and a half either. The consensus expectation for unemployment is 8% or higher through 2Q 2013, and then it dips by 20 basis points per quarter over the next three quarters. The unemployment rate does not drop below 8% until the 3Q of next year. By Q1 2014, the unemployment rate is only expected to be down to 7.5%, based on the average estimate of the economists surveyed.

As always, keep in mind that these estimates are those of “mainstream” economists, many of whom are employed by big banks and institutions. As a group, they are often wrong and their projections work on the theory that we won’t have a recession or another financial crisis – neither of which can be ruled out, in my opinion.

Bernanke’s Jackson Hole Speech – Mixed Signals

Analysts far and wide were hoping for clues in the Fed Chairman’s speech last Friday at the annual economic symposium in Jackson Hole, WY. Some came away optimistic that the Fed will announce QE3 at the upcoming FOMC meeting on September 12-13, while others felt just the opposite. So depending on who you read, you could have taken either position.

In his speech, Bernanke made the case that the first two rounds of QE were successful in helping the economy, a position that many would argue. He also suggested that QE3 – if it were to happen – would also be beneficial. In addition, he also stated:

“Unless the economy begins to grow more quickly than it has recently, the unemployment rate is likely to remain far above levels consistent with maximum employment for some time…. The Federal Reserve will provide additional policy accommodation as needed to promote a stronger economic recovery and sustained improvement in labor market conditions in a context of price stability.”

These remarks and others made The Wall Street Journal‘s MarketWatch.com conclude that Bernanke “made it clear that he’s ready to pull the trigger. The only question that remains is whether it will happen in mid-September or December.”

But while Bernanke made clear that the Fed is willing to intervene via QE3 – if necessary – he also left no doubt that he wants to avoid this if at all possible. Bernanke continued to caution that there are hard-to-quantify downside risks to QE, including higher inflation and the question of how the Fed will unload potentially several trillion dollars in debt securities at some point.

Then there is the question of timing, given that this is an election year. Would the Fed move to implement QE3 at its September 12-13 meeting next week, or would it wait until December? Some argue that the Obama administration would be reluctant to publicly endorse another large round of asset purchases by the Fed, as it would be seen as an admission by the White House that the economy is in dire straits. Privately, however, I would think the Obama administration would welcome it.

At the end of the day, most observers agree that the Fed is willing to do QE3, but probably only if it looks like the economy could be tipping into a recession. Time will tell. If Bernanke does not announce QE3 at next week’s press conference on Thursday (Sept. 13), then I think it’s safe to assume the Fed will do nothing until after the election.

My Thoughts on the Republican Convention

Finally, I suppose I should comment on the Republican convention. Overall, I thought it was very good. With the help of his wife, a couple of very good personal videos and a good closing speech, I think Mitt Romney accomplished what he needed to do. Even the talking heads on MSNBC and CNN agreed.

Many conservatives wished that Romney had been tougher on President Obama, but apparently he and his advisers felt it was better for him to stay above the fray and hope to convince undecided voters that he is human after all. While more post-convention polls will be out later this week, it looks like Romney got a “bounce” of 4-5 points. We’ll see. In any event, the race should remain fairly close.

The bigger question is, what do the Democrats do for three days starting tonight? Without much of a record to run on, the Obama campaign has spent almost all of its money trying to demonize Romney, which hasn’t worked. If they try to do that for four days on national TV, the relatively few viewers that are watching these conventions will tune out early-on.

So it will be most interesting to see what they come up with. The speaker line-up is not very impressive overall, although Bill Clinton’s speech tomorrow night will draw a lot of attention as it should. Other speakers include Harry Reid, Nancy Pelosi, John Kerry and Jimmy Carter.

Most notably, Hillary Clinton will not make an appearance, much less a speech. The most powerful woman in the Democrat Party will not even attend. Hmmm…. Makes you wonder who made that decision – Obama or Hillary?

“2016: Obama’s America” Movie – You Need to See It

Last week, I encouraged you to go see 2016, especially because it is a documentary on Barack Obama’s life and the major influences on him. I admitted that I learned several things about our president that I did not know. I’m not much of a movie goer, but I am going to see it a second time this weekend. I can’t remember the last time I saw a movie twice in theater. You really need to see it!

Over this summer, I have raised the possibility that some of President Obama’s policies have been a part of a grand plan to reduce America’s dominance in the world. Based on the huge response I have received with regard to that notion, it is clear that many of you agree on this point. That is why you need to see this movie. It is eye-opening.

I said this last week, but it bears repeating. I believe that this film will set off alarm bells, even among some liberals. I suspect that more than a few liberals will come away from the movie and conclude: Wait, that’s NOT what I signed up for! If you see the movie, you will know exactly why I say this.

Here is the link to the 2016 movie trailer: http://2016themovie.com.

Have a great week, and keep your seatbelts fastened for a potentially wild September.

Wishing summer wasn’t drawing to a close,

Gary D. Halbert

The Debt can never be paid off through “normal” means. Paying off by normal means would entail a huge, really killer boost in taxes and a brutal unmerciful, slashing of entitlements. The national debt of the US is now well over $16 trillion and growing at the rate of over one trillion dollars a year.

The only way the US’s debts can ever be seriously addressed is to devalue the dollar.

The US owns the world’s greatest hoard of gold. Here’s what I think the authorities have to do. They should unilaterally, overnight raise the price of gold to a high value, maybe around $10,000 an ounce. Thus, each dollar would be worth one ten-thousandth of an ounce of gold. This would allow our enormous debt to be paid off with vastly devalued dollars.

This would be inflationary, since everyone who owned gold would own a pile of devalued dollars. The huge increase in the number of dollars would drive prices up, and that would work against the current forces of deflation.

Nations owning gold would in turn (in order to compete) — devalue their own currencies, and thus be able to pay off their own “impossible” debts. In the end, a new world monetary system would have to be established, but the terrible problem of a planet choking on debt would be solved.

I think this is the only way the world-debt problem is going to be solved. It will, in the end, be solved by devaluation (as Roosevelt did in 1933, when he suddenly and unilaterally raised the price of gold from 20 to 35 dollars an ounce). Interestingly, we now hear an increasing amount of talk regarding gold entering the world monetary system. Furthermore, I think we are going to hear even more about gold in future months. Smart, wealthy, well-informed investors will start accumulating gold. (Soros and Paulson are doing it already. I don’t doubt that Soros has inside information.)

I also believe that the US will, in due time, start backing its currency with part-gold and the dollar will be convertible into gold at around $10,000 an ounce. This will render the dollar the most wanted currency in the world.

I believe the Chinese are onto the same idea. But as of now, China does not own as much gold as they desire, which is one reason China has rushed headlong into the gold business — China is currently the world’s biggest producer of gold. It is also why China is encouraging its own people to buy and accumulate gold. China knows that gold is the future of the world monetary system.

Ed Note: Central Banks are buying Gold, here’s 3 articles:

Central-Bank Gold Buying Seen Reaching 493 Tons In 2012

Is Central Bank buying just a driving force behind gold or much, much more!

Central Bank Action “Good for Gold”, ECB Bazooka Needed as Pressure on Spain Intensifies

Richard Russell publishes a detailed Daily comment, the latest Primary Trend Index (PTI) figure for the day will be posted on his web site — posting will take place a few hours after the close of the market. Also included will be Russell’s comments and observations on the day’s action along with critical market data. Each subscriber will be issued a private user name and password for entrance to the members area of the website.if you subscribe to his Letter that is published and mailed every three weeks. To subscribe go HERE

Russell also offers a TRIAL. (two consecutive up-to-date issues) for $1.00 (same price that was originally charged in 1958). Trials, please one time only. Mail your $1.00 check to: Dow Theory Letters, PO Box 1759, La Jolla, CA 92038 (annual cost of a subscription is $300, tax deductible if ordered through your business).

Investors Intelligence is the organization that monitors almost ALL market letters and then releases their widely-followed “percentage of bullish or bearish advisory services.” This is what Investors Intelligence says about Richard Russell’s Dow Theory Letters: “Richard Russell is by far the most interesting writer of all the services we get.” Feb. 19, 1999.

Below are two of the most widely read articles published by Dow Theory Letters over the past 40 years. Request for these pieces have been received from dozens of organizations. Click on the titles to read the articles.

With Summer unofficially behind us now, we enter three of the more interesting months of every trading year.

U.S. Stock Market – The “Don’t Worry, Be Happy” crowd on Wall Street shall eat up the perception that Bernanke and the FED have or will be in QE3 mode. Despite numerous fundamental and technical reasons for concern, it’s been my belief that the path of least resistance remains up, not down. I continue to think a marginal, new all-time high is possible.

U.S. Bonds – Thanks to QE3 unfolding, I continue to hope the 10yr. T-Bond yield can get down to 1.25% It would be a screaming short if and when it does. U.S. bonds look to be the worse investment vehicle for the next decade.

U.S. Dollar – Despite something like 95%-98% bulls, the U.S. Dollar managed only a dead-cat bounce and is rolling over as we speak. This is in the face of Europe still a basket case (what does that say about the dollar once Uncle Sam shows to be even a bigger basket case next year?). The only party that doesn’t know the U.S Dollar is terminally ill is the U.S. Dollar.

Gold – The “mother” of all gold bull markets has had a classic consolidation/correction in a secular bull market that still has much left on the upside.

Please remember we shall be collecting funds for the “Tokyo Rose” of gold bears when we go to new highs.

Oil and Natural Gas – Triple-digit oil is around the corner. Natural gas remains an avoid.

Special Note – The one fly in the ointment for many markets remains the belief it’s a question of when, not if, war breaks out between Israel and Iran. There are all sorts of signs suggesting it’s indeed when and the number of possible scenarios that can unfold if and when this take place are many. We shall see if and when the time comes and go from there.

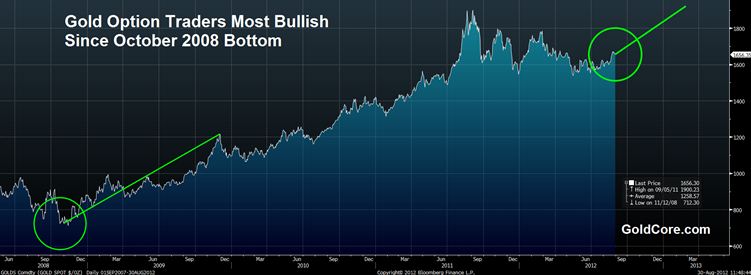

“A new and important bullish indicator for the gold market is that gold calls are at highs not seen since the October 2008 low as option traders go long gold in the belief that it will go higher.

It suggests that option traders believe that U.S. Federal Reserve Chairman Ben Bernanke will hint at or announce additional money printing and monetary easing at the Jackson Hole, Wyoming, symposium (Friday Aug 31st)

Alternatively, it suggests that they are bullish on gold due to the risks posed to the dollar and the risk of inflation taking off.

Option traders are regarded as savvier and tend to be more sophisticated then the more speculative futures traders.”

Mark goes on to say:

“Bernanke may again obfuscate and not give clear guidance regarding monetary policy and further QE.

However the smart money such as PIMCO’s Bill Gross, Jim Rogers, John Paulson and others believe that further QE and money printing remain inevitable. We would concur and advise investors to fade out the short term noise emanating from Jackson Hole and from assorted policy makers on both sides of the Atlantic and focus on the reality that further monetary easing and currency debasement will continue for the foreseeable future.”

PERSPECTIVE

Only a few weeks ago, stock market sentiment figures were at very bearish readings. This was prompted by the prospect of Spain’s insolvency, Euroland splitting up and the worst drought in the US in fifty years.

Not all could be enduring. Crops will soon be harvested and the drought will no longer be in the headlines. Grains will turn down.

In the meantime, often seasonal optimism could run into early September. Spanish yields have declined and industrial commodities (base metals and crude) have rallied as well.

Even most classes of bonds have rallied this week. This could be anticipating a pause in the stock market advance. Investment-grade corps, treasuries and emerging market debt are doing well, but the sub-prime seems to be topping (chart follows).

On money market stuff, the Ted-spread has narrowed significantly since the concerns of late last year. However, in the past two weeks it has had some unusual swings. Perhaps some volatility prior to a change.

An overall blessing has been the decline in the gold/silver ratio. From 59.4 in June it has declined to 54.5. Much of this has been accomplished in a rush since last week. Enough of a rush to drive the daily RSI down to 27. This has been the RSI level that has ended most of the declines over the past decade.

In looking at the ratio from the other direction, Ross’s Silver/Gold Chart is updated and attached. By this measure, the rally in precious metals is close to ending.

Usually our Pivots are sent out earlier on each Thursday, but things looked fascinating yesterday and much of today was spent trading. In order to get this one out a simpler form is being used.

Also noteworthy is that December corn has completed a “Sequential Sell” pattern that suggests an important top is at hand. The rollover would likely take down other hot agricultural commodities (GKX).

Momentum on the GKX reached 82 a couple of weeks ago and that has ended important rallies over the past decade. One of which was with the cyclical high in 2008. That high was 513 on the index, the next important high was 570 in March last year. So far, this year’s high was 533 a couple of weeks ago – with the momentum high. Today’s close was 513.

Crude oil has accomplished an outstanding swing from very oversold to rather overbought. Also yesterday’s ChartWorks noted that a “Sequential 9” had been accomplished. Also the Dollar Index is approaching support at the 81 level. Last week we noted that the Canadian was approaching resistance at 102 on good momentum. It reached 101.6 and it has declined to 100.5. Technically, a test is needed to reverse the trend, but weakness in the fall has been likely.

While we have been hoping the sunshine for orthodox investment would run into early September, the actual seasonals for the stock market suggest caution. Over the past thirty years the S&P has set its August high early in the last week of the month. Remember the rules for after Labor Day – Don’t be overweight equities and don’t wear white shoes.

With the initial discovery of financial troubles the flight to the liquidity of gold could help the price in dollars, but the “flight” could also be to the unique liquidity of US treasury bills, which would firm up the dollar.

WRAP

- The advice through the summer has been to sell into the rallies for most investment sectors. The hit to US bond markets has been a big heads up and the rebound could run for a week or so.

- It seems that another liquidity problem will not be avoided. The process of discovery could begin in the next few weeks.

- In which case, which sector could provide the “safe haven”?

- In the disaster that began in March 2000 banks became the defensive equity group. The long bond rallied from 91.8 in March 2000 to 110 as the crash completed in late 2002.

- In the 2008 Crash, long bonds also enjoyed the “flight to quality” in a bull move from 105 in mid-2007 to 143 at the end of 2008. There was no significant defensive equity sector.

- This time around, there may be no large equity sector that could be defensive. Moreover, the European bond revulsion could worsen and spread to the US bond markets. In which case, the long bond will not become the focus of the next flight to quality. A sound understanding of term risk could prevail.

Representative Sub-Prime Mortgage Bond

The RSI of the Silver/Gold ratio suggests that it is time to start scaling back positions in miners. Optimum gold targets are $1692 & $1720.

SIGNS OF THE TIMES

“Federal Reserve Chairman Bernanke calls it his ‘nightmare scenario’. Republicans are considering including a plank in their party platform calling for a full audit of the central bank.”

– Bloomberg, August 8

Why not?

Health agencies have been calling for full clinical testing of “alternative health remedies” such as homeopathic medicine. The latter could be germane as it prescribes small amounts of some compounds that are toxic. Now we all know that large expansions of credit are ultimately toxic. But in the early days of tax-payer seduction, central bankers touted that they knew just how much to issue to “manage” the economy. They would never be reckless in providing stability. Then every country had to have a central bank and a “national economy” resulting in the longest run of high volatility in history. Sort of a relentlessly forced instability.

Now the Fed is overloaded with “toxic waste”.

Hey, but not to worry! A year after the 2008 Crash, the Financial Stability Board was formed and based in Basel. It is made up of finance ministers and central bankers – all specialists in the arts of homeopathic finance.

Somehow this reminds of the BIS. The website of the Bank for International Settlements states its mission is “to promote international stability”. It was formed in 1930 – a year after the 1929 Crash – and is located in Basel.

“Foreign direct investment in China fell to the lowest level in two years in July.”

– Bloomberg, August 16

“China Mobile Ltd., the world’s biggest phone company by subscribers, fell the most [-5%] in more than year as profit growth cooled to the slowest annual pace in 13 years.”

by:

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bhoye.institutionaladvisors@telus.net

WEBSITE: www.institutionaladvisors.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair