Timing & trends

Unemployment Rate in Canada Stays Flat in May; Europe Continues to Add to Global Uncertainty

The S&P TSX Composite closed at 11,500.63, up 1.23% for the week, but down 3.8% since the start of the year and uncomfortably close to 2012 lows.

Canadian employment numbers came in on Friday slightly above expectation with 7,700 new jobs being created during the month of May. Consensus estimates for the month were for 5,000 new jobs. The numbers, while a little higher than expected, essentially put an end to the strong month-over-month momentum we have seen March. Collectively, March and April brought with them 140,000 new jobs; a 30 year record for Canada’s economy. Although the prudent minded knew to look at the numbers with caution, there were, not surprisingly, many optimists that hoped the performance was the start of a new trend. Clearly they were disappointed by the May numbers. Overall the Canadian unemployment rate remained flat at 7.3%.

While we continue to see mixed data in North America, the situation in Europe is nothing less than clear. The continent continues to struggle with an unyielding debt problem which many fear is spilling over into the global marketplace. After rallying at the start of the year, nearly all major global stock markets are now either down or flat. Although Greece remains firmly in the spotlight, Spain has moved a few steps up the ladder to release its financial woes upon the world. Spanish banks have come under serious pressure which has caused economists and analysts to predict that the country will formerly request an EU bailout on Saturday, making it the fourth nation in Europe to do so. The International Monetary Fund is currently in the process of conducting an audit on how much money Spain would require (due out Monday) with preliminary estimates at €50 to €60 billion and potentially higher. Not surprisingly, ratings agency Fitch announced on Thursday that it was reducing Spain’s credit rating by three notches on from A to BBB. This rating is now only one notch above junk status.

The situation with the PIGS (Portugal, Italy, Greece, and Spain) is analogous to what happens to an individual person that takes on too much debt. As an individual’s debt continues to grow, and their ability to pay that debt declines, naturally creditors will require a higher interest rate to compensate them for the additional risk. But at some point, creditors will just stop lending the money regardless of the rate that the debtor is willing to pay. This is true unless of course someone with a better credit rating and balance sheet agrees to co-sign the loans. In the case of Europe, this reluctantly generous co-signer is of course Germany. But Germany’s graciousness is not without a self-serving purpose as they stand to benefit more than anyone by the preservation of the Euro.

In the pre-Euro area, each of the debtor nations would simply allow their currency to de-value which would have the natural effect of lowering their respective debt burdens in real purchasing power terms. Although this is quite painful in the short term, it has historically been the only way to sort these issues out, as was the case with Argentina’s debt crisis in 1999 – 2002. The short-term pain was intense, but Argentina did recover and now enjoys one of the highest economic growth rates in Latin America.

SIX DAYS after they climbed back above $1600 an ounce, gold prices dropped back below that level on Thursday, as Federal Reserve chairman Ben Bernanke appeared before Congress at the Joint Economic Committee. (more below -Ed)

This is not the first time we’ve seen this. Back on February 29, gold fell $100 an ounce while Bernanke was testifying before the House Financial Services Committee. What on earth is the man saying to have such an adverse impact on gold prices?

Well, on the two occasions cited above, it wasn’t what he said, but what he failed to say that did the damage. In short, Bernanke failed to make any explicit promises of further Fed quantitative easing.

Last Friday, gold shot up 5% in Dollar terms, following disappointing US jobs and manufacturing data. Clearly, some traders were betting that the Fed would respond by announcing further stimulus, a bet that failed to pay off. Bernanke’s reticence in this regard is hardly surprising, though. It’s what central bankers do: they say as little as they can get away with to keep as many options open as they can.

They also talk to each other, and it seems the major central bankers have agreed a common script, one which has as its central theme a focus on the failings of fiscal policymakers (i.e. politicians). Here is European Central Bank president Mario Draghi speaking on Wednesday:

“Some of these problems in the Euro area have nothing to do with monetary policy. That is what we have to be aware of and I do not think it would be right for monetary policy to compensate for other institutions’ lack of action.”

And here’s Bernanke a day later:

“…under current policies and reasonable economic assumptions, the [Congressional Budget Office] projects that the structural budget gap and the ratio of federal debt to GDP will trend upward thereafter, in large part reflecting rapidly escalating health expenditures and the aging of the population. This dynamic is clearly unsustainable…fiscal policy must be placed on a sustainable path that eventually results in a stable or declining ratio of federal debt to GDP.”

Translation: don’t look at us.

Central bankers are trying to put pressure on their political masters to deal with problems that are beyond the scope of monetary policy. It is these problems, they argue, that are at the root of the current crisis.

It was put to Bernanke by JEC vice chairman Kevin Brady that the Fed itself is encouraging political inaction by keeping QE3, a potential third round of quantitative easing, on the table.

In other words, the belief that the Fed is on standby to combat any crisis makes a crisis more likely, reducing as it does the incentive to take difficult preventative action.

The trouble is, the Fed and other central banks daren’t row too far back from talk of stimulus for fear that this will provoke a crisis. This is why Bernanke made it clear the option was on the table, while also saying “Look over there” and pointing at the so-called fiscal cliff – the combination of tax cut expiries and mandated spending cuts that await the US should lawmakers fail to reach agreements to prevent them (a genuine risk in an election year).

So we are at an impasse, meaning gold prices are susceptible to marginal sentiment and bets on what monetary policymakers will do next. This has been the case all year. For example, gold prices rallied in January after the Fed published projections showing its policymakers expected near-zero interest rates until late 2014. Gold also saw a jump in March as Bernanke reiterated the need for accommodative policies.

The truth is, though, that there has been little rhyme or reason to these moves. If you look at what Bernanke actually said on each occasion, it is pretty much a rehash of what he’s said before. Fed statements since the start of the year have all broadly said this: “We’re not out of the woods, we’ll keep an eye on things, and we’ll do as we see fit.”

Details have changed, depending on the newsflow, but that’s all. Here’s an extract from Thursday’s testimony:

“…the situation in Europe poses significant risks to the US financial system and economy and must be monitored closely. As always, the Federal Reserve remains prepared to take action as needed to protect the US financial system and economy in the event that financial stresses escalate.”

Later on, Bernanke said there is “no justification” for fears that QE could spark inflation. Taking these comments together, one could make a case that the Fed are about to push the button marked ‘More Stimulus’. But of course, traders had already jumped to that conclusion last Friday, and so were forced to ‘unjump’.

The truth is, we don’t know when or if we will see more QE, and we doubt anyone at the Fed does either. QE is not about economic stimulus. Not really. It may be packaged as a way of boosting growth, but in our view its real aim is to fight crises in the banking sector.

This is where it gets difficult for gold investors. It may be that the Fed, along with other central banks, are holding fire until the banking stresses in Europe become really acute. As we saw last November and December, a banking crisis can be accompanied by sharp falls in gold prices, as gold is sold or leased to raise Dollars, increasing its immediate supply and putting downward pressure on prices.

Indeed, along with the disappointment that Bernanke was note more dovish following last week’s economic news, another possible explanation for gold’s fall this week is that uncertainty over QE raises the risk of a sudden funding crunch.

Another factor to bear in mind is inflation expectations. Bernanke said on Thursday that these are “quite well anchored”. But some argue that they are still too high to make QE an immediate prospect, with 5-Year breakeven rates – the difference in yield between inflation-linked and nominal debt – still too high:

There remains a significant chance we will yet see more Fed QE. But things may need to get quite a bit worse first. In the meantime, the only clues we are likely to get are those we can glean from the Orwellian radio static of central banker doublespeak.

Or, if you’re a long run investor, you could just ignore the noise being made by gold prices and crack open a beer…

Ben Traynor

BullionVault

Gold value calculator | Buy gold online at live prices

Editor of Gold News, the analysis and investment research site from world-leading gold ownership service BullionVault, Ben Traynor was formerly editor of the Fleet Street Letter, the UK’s longest-running investment letter. A Cambridge economics graduate, he is a professional writer and editor with a specialist interest in monetary economics.

(c) BullionVault 2011

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

“As we never tire of observing, gold has delivered a much higher return during the last 15 years than Berkshire Hathaway, perhaps the most civilized of American stocks. By any quantitative measure, gold has kicked Berkshire’s rear-end from wherever you happen to be reading this column all the way back to Omaha, Nebraska.”

Gold is “forever unproductive,” says Warren Buffett, CEO of Berkshire Hathaway.

“Civilized people don’t buy gold,” says Buffett’s sidekick, Charlie Munger. Civilized people, says Munger, “invest in productive businesses.”

So let’s see… Where does that lead us?

If…

A) Berkshire Hathaway invests in productive businesses and;

B) Investing in productive businesses is civilized and;

C) Warren Buffett and Charlie Munger direct Berkshire’s investments;

Then…

D) Buffett and Munger are civilized.

Gee whiz! That’s lucky!

But to make sure the world appreciates just how civilized these two civilized gents are, they continuously (and very publicly) belittle both gold and the uncivilized masses who consider it a store of value.Gee whiz! That’s lucky!

“Gold gets dug out of the ground,” Warren Buffett famously observed, “then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

Yes, that’s right, anyone from Mars…or from Berkshire Hathaway headquarters. But most of the other seven billion folks residing on either Earth or Mars understand that gold has at least some utility. At a minimum, they understand that gold possesses more utility than the gold-bashing blather that spills from the lips of Buffett and Munger. Gold may be inert, but at least it’s not toxic.

“When it comes to bashing gold,” writes Eric McWhinnie for Wall St. Cheat Sheet, “few do it as publicly and extremely as the crew at Berkshire Hathaway… Buffett dedicated a decent part of his latest shareholder letter to criticizing gold. He painted an analogy of the world’s gold stock as a useless cube that would fit within a baseball infield. Buffett wrote:

Today the world’s gold stock is about 170,000 metric tons. If all of this gold were melded together, it would form a cube of about 68 feet per side. (Picture it fitting comfortably within a baseball infield.) At $1,750 per ounce — gold’s price as I write this — its value would be about $9.6 trillion. Call this cube pile A.

Let’s now create a pile B costing an equal amount. For that, we could buy all U.S. cropland (400 million acres with output of about $200 billion annually), plus 16 Exxon Mobils (the world’s most profitable company, one earning more than $40 billion annually). After these purchases, we would have about $1 trillion left over for walking-around money (no sense feeling strapped after this buying binge). Can you imagine an investor with $9.6 trillion selecting pile A over pile B?

Ummm…maybe…depending on the circumstances in which one finds oneself.

Even Charlie Munger acknowledges that “gold is a great thing to sew onto your garments if you’re a Jewish family in Vienna in 1939.” Although Munger’s tasteless remark was an attempt to disparage gold, he inadvertently paid the monetary metal a compliment. He acknowledged that gold is the “go to” investment during times of crisis. It is the thing to own in uncivilized times.

Clearly, gold was not the very best thing to own when the young Buffett and Munger were launching their careers — a period that happened to coincide with America’s post-WWII, once-in-an-empire, economic boom. At the end of the Second World War, the United States possessed a robust manufacturing infrastructure; its competitors possessed ruble. Not a bad time to invest in America’s “productive businesses.”

But not every investor will find himself in the midst of one of the most powerful, world-dominating economic expansions in human history. Instead, some investors may find themselves in some sort of “Vienna, 1939.” In such circumstances, the ideal investment may not be a share of Coca-Cola…or even a share of Apple (more about which below). It may be an ounce of gold.

“Some Jews in Vienna in 1939 operated extremely productive businesses,” we observed in the May 24 edition of The Daily Reckoning. “Unfortunately, they could not stitch any of those into their garments.”

But gold is not merely a great thing to own amidst extreme circumstances. It can also be a great thing to own amidst merely marginal circumstances, like, for example, if you happen to be living during the tail end of one of the most powerful, world- dominating economic expansions in human history…rather than at the beginning of it. In other words, gold may be a great thing to own in America in 2012 — no matter whether you be Jewish, Christian, atheist or spiritually confused.

“As civilizations lose their civility,” we observed a few days ago, “investing in productive businesses can be a very unproductive activity. As civilizations lose their civility, share prices tend to fall and gold prices tend to rise…which is exactly what has been happening in our beloved U.S.A during the last few years.”

Thus, as we never tire of observing, gold has delivered a much higher return during the last 15 years than Berkshire Hathaway, perhaps the most civilized of American stocks. By any quantitative measure, gold has kicked Berkshire’s rear-end from wherever you happen to be reading this column all the way back to Omaha, Nebraska.

Unlike Buffett and Munger, David Einhorn, founder of Greenlight Capital, believes we Americans are in an era in which gold is likely to reward those who hold it. He recently countered Buffett’s “analysis” of gold by saying, “If you wrapped up all the $100 bills in circulation, they would form a cube about 74 feet per side… The value of all that cash would be about a trillion dollars. In a hundred years, that money will have produced nothing… It will not pay you interest or dividends and it won’t grow earnings, though you could burn it for heat… Alternatively, you could take every US note in circulation, lay them end to end, and cover the entire 116 square miles of Omaha, Nebraska. Of course, if you managed to assemble all that money into your own private stash, the Federal Reserve could simply order more to be printed for the rest of us.”

Einhorn’s dig at the Berkshire boys is merely his latest counter- punch against the anti-gold elite. A few weeks back, he likened Fed Chairman Ben Bernanke’s monetary policy to gorging on jelly donuts.

“A jelly donut is a yummy mid-afternoon energy boost,” Einhorn explained. “Two jelly donuts are an indulgent breakfast. Three jelly donuts may induce a tummy ache. Six jelly donuts, that’s an eating disorder. Twelve jelly donuts is fraternity pledge hazing.

“My point,” Einhorn elaborated, “is that you can have too much of a good thing… Chairman Bernanke is presently force-feeding us what seems like the 36th jelly donut of easy money and wondering why it isn’t giving us energy or making us feel better. Instead of a robust recovery, the economy continues to be sluggish…”

“As a result,” Einhorn concluded, “I will keep a substantial long exposure to gold, which serves as a jelly-donut-antidote for my portfolio.”

Like Einhorn, many other high-profile hedge fund managers are amassing large quantities of gold and gold-related investments. According to filings with the Securities and Exchange Commission, several big hedge funds upped their allocation to gold during the first three months of 2012. Billionaire fund manager John Paulson, for example, maintained his large 17.3 million-share position in the SPDR Gold Trust (NYSE:GLD). He also upped his holding of NovaGold Resources (NYSE:NG) and IAMGOLD (NYSE:IAG).

Daniel Loeb’s Third Point hedge fund maintained its position in “GLD,” while boosting its stake in Barrick Gold (NYSE:ABX). George Soros’ management firm nearly quadrupled its exposure to “GLD” during the first quarter, while also buying call options on Newmont Mining (NYSE:NEM).

Those guys aren’t buying gold because they expect it to be “forever unproductive,” as Buffett asserts, or because it is only useful during a Nazi occupation, as Munger asserts. They are buying it because they believe the American economy of the near-future will not treat investment capital as hospitably as the American economy of the last several decades.

They are buying it because they perceive that important aspects of American civilization are becoming somewhat more barbaric…like, for example, the barbaric fiscal policies that never fail to produce trillion-dollar deficits, or the barbaric monetary policies that always fail to produce sustainable economic activity.

Barbarous times call for barbarous measures.

Regards,

Eric J. Fry

for The Daily Reckoning

[Joel’s Note: Obviously, Dear Reader, the Berkshire Boys are not the only folks pooh-poohing gold these days. In fact, bashing gold is something of a daily Wall Street pastime. And even those folks who feel no need to bash gold are quite content to ignore it. They’d rather buy a “hot stock” like Facebook…ugh…or maybe a proven winner like Apple.

We have no idea who’s right or wrong here or, more importantly, who will be right or wrong going forward. But we’d love to hear your thoughts on the subject…just for kicks. We’d like to hear from you whether gold or Apple will be the better bet over the next five years.

Matt Nesto posed this identical question a couple days ago to his guest on “Breakout,” Lee Munson, Chief Investment Officer at Portfolio, LLC. Munson responded unequivocally, “I’d rather you go out…and buy Apple.” As for gold, Munson scoffed, “When the world looks to be ending, like 2008, people aren’t going to buy gold, they’re going to buy dollars, and if things really get bad, they’ll buy dry food and automatic guns.”

What about you, Dear Readers? Do you side with Munson (and Buffett and Munger)? Or do you think gold might be the better bet? Or maybe you are conflicted, just like Daniel Loeb, the hedge fund manager Eric cites in his column. Although gold is the second largest holding in Mr. Loeb’s hedge fund, Apple is the fourth largest holding. Hmmm…maybe that’s the perfect hedge. Anyway, we’d love to hear your thoughts.]

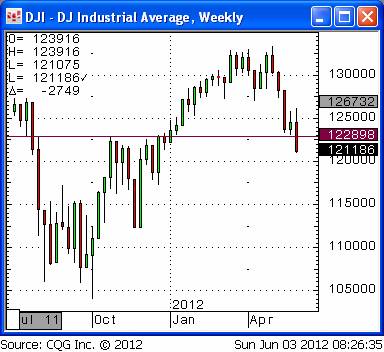

Below is our updated wave chart of the Dow Jones Industrial Average. We get the sense that if we don’t get

the “bounce” higher soon, this market can fall hard i.e. major capitulation from the newly anointed bulls. By our

count we are entering the most powerful leg of the down wave. We are assuming the bear market rally to 13,339 on

May 1st is done! [Labeled 2 of 3] We want to remain long-term short equities and most risk asset markets as the

global macro is playing out as we anticipated.

Subscribe to Black Swan’s Free Currency Currents HERE (subscription lower right side)

Since February I have been anticipating a significant change in market psychology that would produce lower stock and commodity prices and a rising US Dollar. I waited for confirmation and got that…in spades…the first week of May (see May 7 commentary) with a number of KEY WEEKLY REVERSALS. I continue to trade on the expectation of lower stocks, lower commodities, and a higher USD…with gold also doing better…all the while expecting that we could see a “brisk” counter-trend move across markets! – from www.VictorAdair.com

Market action the last three days and especially today was a perfect storm, or if you like, it never rains but it pours: European debt concerns intensified and evidence mounted that the global economy is slowing down. Markets behaved just as you would expect in a post credit bubble collapse…by seeking safe havens in a deflationary environment…as the consequences of “way more money has been borrowed than will ever be repaid” keep coming home to roost.

Last week I wrote about how I had “done a 180” from being a gold BEAR for the last three months (Feb to May) to being a gold BULL as I sensed a change in market psychology…I thought that gold, which had been the baby thrown out with the bathwater as “risk assets” declined, might morph from a “risk asset” into a “safe haven”… and that seemed to happen this week…especially today when gold rallied over $60 while global stocks tumbled.

Looking at markets this week it would be a gross understatement to say that money moves as Market Perceptions change. Money is physically moving from the periphery to the centre…Spanish banks have apparently lost deposits of 100 billion Euros as people pull funds out of Spanish banks and either put that money under the mattress or wire it to Germany…in another context money is leaving the “rest of the world” and going to the USA…(and Japan, oddly enough) moving from the periphery to the centre…

Charts: We had KEY WEEKLY REVERSALS this past week in the S+P and gold (and silver and platinum…)

The VIX, the FEAR index, which traded to a 5 year low of 14% in mid-March, jumped to 26.6% today but it is still a long way from the 45% it hit in early October of last year…which might imply that, “You ain’t seen nothing yet” as far as fear goes.

Credit markets: the yields of (relatively!) “safe credits” (US, UK, Germany, Switzerland, Canada, etc) have moved to record lows while “weak credits” have seen rising yields.

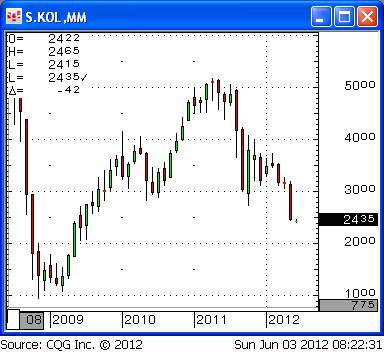

Energy: Crude oil prices have plummeted as Perceptions change about the health of the global economy…less demand for fuel…WTI was $106 May 1,2012…it traded a low of $82 today…a 23% decline. The Coal ETF traded to a three year low.

Currency: the CAD has lost 6 cents from the end of April to today. The Euro fell 9% to a 2 year low in the same time frame…the US$ Index has closed higher for 5 consecutive weeks.

Stocks: The major American stock indices have been among the strongest in the world but today the DJI went negative YTD. The Toronto stock index is down ~5% YTD.

Commodities: the CRB commodity index has been trending lower since the KEY turn date of May 2, 2011, and has fallen ~27% since then to a 2 year low, down 12 of the last 14 weeks. My concern, as previously expressed, is that there has been a huge build up of speculative long positions in commodities (greater than before the crash in 2008) and these positions are vulnerable to a liquidation accelerated decline….bad news for the CAD and other commodity currencies.

The 64 Zillion dollar questions: Will the “authorities” be spurred to action…or are they “keeping their powder dry” until things get worse before they act? Is the intensifying crisis in Europe severe enough to make the authorities try to get in front of the bank run with some kind of continent wide deposit insurance? A Eurobond? Will the Fed come in with more QE as the American employment picture worsens? It looks like the gold market, in addition to being a “safe haven” during a “risk asset” storm may be anticipating some form of “printing.”

Psychology: Very risk adverse…BUT…market Perceptions could turn on a dime if the “authorities” take action…possibly setting off a sharp rally in the Euro if some of the current massive short positions try to cover…and given the All-One-Market aspect of today’s financial markets, a sharp reversal in the Euro could set off sharp reversals in other markets…

My trading horizon view: Since February I have been anticipating a significant change in market psychology that would produce lower stock and commodity prices and a rising US Dollar. I waited for confirmation and got that…in spades…the first week of May (see May 7 commentary) with a number of KEY WEEKLY REVERSALS. I continue to trade on the expectation of lower stocks, lower commodities, and a higher USD…with gold also doing better…all the while expecting that we could see a “brisk” counter-trend move across markets!

My “Big Picture” view: remains that we are living in a deflationary world…a natural sequel to a thirty year credit boom…that the actions of the “authorities” to date have been “rear-guard” in strength, although certainly powerful enough to produce tradable rallies. I have thought that deflationary pressures would move from market to market like “rolling thunder”…hitting the USA first, then Europe with Asia next up. My net worth is nearly all in cash, 75%CAD, 25%USD, and I actively trade financial markets to make money and keep watch on developments.

Best wishes for good health and good trading,

Victor

Victor Adair – www.VictorAdair.com

Senior Vice President and Derivatives Portfolio Manager

Victor Adair is a Senior Vice President and Derivatives Portfolio Manager at Union Securities Ltd. Victor began trading financial markets over 40 years ago and has held a number of senior positions during his long career as a commodity and stockbroker. He provides daily market commentary on CKNW AM 980 radio Vancouver and is nationally syndicated on Mike Campbell’s weekly Moneytalks radio show.

Victor’s trading focus is primarily on the currency, precious metal, interest rate and stock index markets and his clients are high net worth individuals and corporations.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair