Timing & trends

This analysis as well as Martin Armstrong’s Quarterly Closing Post clearly state that it is just not Gold’s time to explode upwards. Jordan indicates below the factors that will have to fall into place before Gold can begin a long term bull swing upwards – R. Zurrer for Money Talks

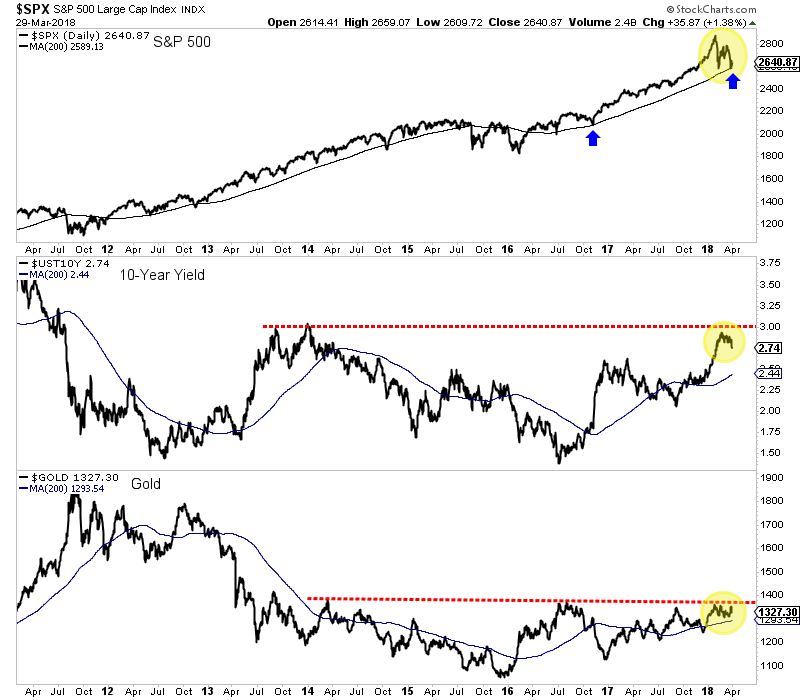

Last week we noted that Gold’s quarterly close would be a key marker for Gold’s immediate breakout potential. Gold was seemingly on course for its highest quarterly close since 2012 until it reversed back below quarterly resistance at $1330/oz. Hence, an imminent break to the upside is unlikely and gold watchers will have to remain patient. It’s not yet Gold’s time. It will be soon enough.

One catalyst for the most recent strength in Gold (the correction in equities) appears to have faded as the S&P 500 has held its 200-day moving average. A sustained rebound in equities while bond yields correct would not be particularly bullish for Gold. The obvious reason is capital is flowing into equities and not Gold. A rebound in equities amid a temporary reduction in inflation expectations would equate to stable or rising real yields.

{kind=link}

The other scenario is bond yields do not break to the upside, there is a slowdown, the stock market declines and the Fed has to reverse course all together. As we predicted in past editorials, long-term yields are trending lower and that could continue. In the meantime, Gold will not break to the upside unless the stock market experiences more turmoil.

In addition to the current macro-market backdrop, history suggests that it may be too early for Gold and gold stocks to begin another bull move. In November we discussed how the gold stocks were following the pattern that other markets followed after a “mega-bear market” (which we define as multi-year and +80% in price).

Take a look at those examples and note the time between the end of the bear market and the next significant low (from which the bull resumed). In most cases the time between those lows is two years and seven to nine months. For the gold stocks it has only been two years and two months since that epic January 2016 low.

Assuming stocks rebound and long-term bond yields continue to moderate, then Gold is unlikely to breakout this spring. However, that is perfectly okay as our historical study suggests the miners (while facing little downside) may not begin a real bull move for several months. Gold Investors should not be discouraged as they could panic at the absolute worst time (I’m already seeing it anecdotally). Regardless of whether the bull move begins in a few months, five months or whenever, we continue to remain patient while accumulating the juniors we think have 500% return potential over the next 18-24 months.

Jordan

1. It’s a Hideous Money Grab, Pure & Simple

1. It’s a Hideous Money Grab, Pure & Simple

by Michael Campbell

Mike is hot under the collar about a new tax about to be levied on anyone who who owns a cottage, ski condo or family vacation home. The tax will have to be paid every year! They’re calling it a speculation tax.

2. Bundesbank Warns German Banks Rates are Moving Higher

Martin Armstrong reports the latest movements on the interest rate front as well as the remarkable move by Germany which will convince the world the European project is authoritarian (Germany arrested a Catalonian politician enforcing Spain’s dictatorship)

3. Ozzie Jurock’s Latest Real Estate Recommendations

Ozzie’s track record has been remarkable, Surrey BC up 60% last year, Seattle, Phoenix, Coquitlam, Burnaby….the list goes on but what he wants you to know is where to go now

1. Yet Another Chart That Screams “Look Out!”

1. Yet Another Chart That Screams “Look Out!”

Another chart that bolsters Martin Armstrongs case that a Monetary Crisis is Beginning. A monetary crisis will change everything with both banks and debtors facing rapidly rising rates.

2. The Progressive Left Don’t Make Sense

by Michael Campbell

The left in Canada helps the US expand Oil production & build pipelines everywhere yet prevents Canada from exporting its Oil through pipelines. Just why are they on the US’s side?

3. The Way to Survive Hyperinflation

Martin Armstrong gives advice to a Venezuelan gentleman whose pension payout no longer can buy him a hamburger. A circumstance no longer an impossibility with the pension crisis unfolding as we speak in Canada & the US .

Mark expects the market to change directions after yesterdays nearly 3% Stock Market rout that was caused by a brace of factors from tariffs to a potential bond market crash. Using his 35 years of experience and his VOLUME REVERSAL ™ methodology Mark gives us a thorough analysis of this violent collapse and expected rally – R. Zurrer for Money Talks

Stocks showed a substantial move to the downside during trading on Thursday, with the major averages adding to the modest losses posted in the previous session. If you didn’t know, astrologically Mercury went retrograde and won’t go direct until April 15. Google it. Meanwhile, the ‘Ides of March’ and the Vernal Equinox often signals a change in market direction. The major averages ended the session near their worst levels of the day. The Dow plunged 724.42 points or 2.9 percent to 23,957.89, the Nasdaq tumbled 178.61 points or 2.4 percent to 7,166.68 points or 2.4 percent to 7,166.68 and the S&P 500 plummeted 68.24 points or 2.5 percent to 2,643.69. The sell-off on Wall Street supposedly reflected concerns about the impact of a potential trade war after President Donald Trump announced tariffs on at least $50 billion worth of Chinese imports, an absurdity about such a small amount as compared with the overall trade deficit with China. Instead, our sources say a potential bond crash may be the real reason.

Technically, I had mentioned that the 24,400 to 25,400 range was to be watched and lo and behold we broke it to the downside! Today’s actions completed a 5-wave decline off the highs, taking the Nasdaq 100 from 7200 to 6682, a loss of more than 500 points in a very short period of time. The S&P 500 went from over 2800 to 2642, 158 points. At this point, when you have key support near and short term oversold, with an extreme negative tick near the close of minus 1419 the chances of at least a bounce may be imminent, but we’ll see what happens tomorrow! We are definitely oversold at this point. Looking out a few days/weeks at the SPX, a return to SPX 2533 appears to be the markets objective. Short term support is at the 2632 and 2594 pivots, with resistance at 2656 and 2731 (See chart below).

Before the newly announced tariffs take effect, the Office of the US Trade Representative will release a list of more than 1,000 possible tariff lines, technical codes that apply to a particular good. There will then be a 30-day comment period during which companies and industry groups can raise objections to certain goods being included in the tariffs. During this time there will also be a public hearing on the tariffs. After the comment period, the USTR will determine which goods the tariffs will apply to and release those findings. So, it could be well into May or June before the tariffs are fully implemented. The restrictions on trade will most likely push up prices on imports of Chinese goods. For businesses that use the imports in their end products, the tariffs will most likely drive up costs and lead to increased prices or cuts in other areas of business.

The House of Representatives approved a $1.3 trillion spending bill to avert a government shutdown and fund federal agencies through Sept. 30. The Republican-led chamber backed the measure 256-167, sending it to the Senate ahead of a midnight Friday deadline. But 90 of the 238 House Republicans voted against it. Coupled with recently enacted tax cuts, the bill is projected to lead to budget deficits of more than $800 billion for this year. Conservatives balked at the deficit spending. Democrats complained that in the rush to pass the bill, few if any lawmakers had time to read through the 2,232-page tome to see what it actually contained. The bill was unveiled late on Wednesday.

Trump is frustrated over trade imbalances and the theft of intellectual property by China. His proposed tariffs aren’t likely to remedy the situation, and could make it worse. China’s Commerce Ministry issued a statement saying, “China will not sit idly to see its legitimate rights damaged and must take all necessary measures to resolutely defend its legitimate rights.” Reports suggest China will impose tariffs on US exports of the major agricultural products sorghum, soybeans, and hogs. More than half of the soybeans and sorghum exported by the US goes to China.

China is a major market for US agricultural products, cars, machinery, and other products. In 2016, China was the third largest market for US exports. Conversely, more than 41% of clothing and 72% of footwear sold in the US are made in China. Analysts believe that not only will US and Chinese businesses and consumers suffer from dampened demand and higher prices of goods, but other countries will experience collateral damage. US-China bilateral trade investment ties are integrated with global supply chains. So, a US-China trade war is necessarily going to have an effect on companies and consumers in other countries. And US-China relations are not good right now. The tariffs could encourage domestic Chinese sentiment to turn against the US. The announcement comes after the passage of a law allowing top US officials to visit Taiwan, a measure that China strongly opposes. Beijing views the self-ruled island as a “rogue province” that belongs to China. Truth is, we don’t know all the implications. We could have an all-out trade war, or the complexity of the global supply chain might limit the fallout. One thing seems highly probable – higher prices for consumer goods. Tariffs are essentially a tax. And while the Trump administration recently passed a tax break, the biggest beneficiaries were corporations. Tariffs will hit consumers squarely in the pocketbook. No surprise that Walmart and Target were each down 1.2% today. Boeing fell more than 5 percent. China has specifically threatened the US. aircraft maker if Trump raised levies. In 2016, the Communist Party newspaper said its Boeing orders, among them a $38 billion package announced when China’s president visited, could be replaced with Europe’s Airbus. Banks and insurers sold off as well. A slump in Treasury yields as investors sought havens weighed on the sector’s earnings prospects. JPMorgan Chase lost 4.2 percent. China’s Global Times — which has links to the ruling Communist Party – this week accused the U.S. of “dumping” soybeans, raising concern that the crop will be among the first items China targets. Currency depreciation could be one channel through which authorities in Beijing aim to increase the competitiveness of their products. The dollar rose 0.5 percent relative to the Chinese offshore yuan. China’s holdings of American bonds, notes and bills have already dipped to a six-month low as of January.

On the U.S. economic front:

A report released by the Labor Department showed a modest uptick in first-time claims for U.S. unemployment benefits in the week ended March 17th. The report said initial jobless claims edged up to 229,000, an increase of 3,000 from the previous week’s unrevised level of 226,000. Economists had expected jobless claims to dip to 225,000. A separate report released by the Conference Board showed a bigger than expected increase by its index of leading U.S. economic indicators. The Conference Board said its leading economic index climbed by 0.6 percent following a 0.8 percent increase in January. Economists had expected the index to rise by 0.3 percent.

Steel stocks turned in some of the market’s worst performances on the day, resulting in a 6.2 percent drop by the NYSE Arca Steel Index. Considerable weakness was also visible among financial stocks, with the KBW Bank Index and the NYSE Arca Broker/Dealer Index slumping by 4.1 percent and 3.6 percent, respectively. Oil service, pharmaceutical, transportation, and chemical stocks also moved notably lower amid broad based weakness on Wall Street.

In the bond market, treasuries showed a significant rebound following the drop seen in the previous session. Subsequently, the yield on the benchmark ten-year note, which moves opposite of its price, slid by 7.5 basis points to 2.832 percent.

Economic Reports

February Durable Goods Orders to be released at 8:30 AM EST on Friday are expected to increase 1.6% versus a drop of 3.7% in January. Excluding Transportation Orders, February Durable Goods Orders are expected to increase 0.5% versus a decline of 0.3% in January.

Canadian February Consumer Price Index to be released at 8:30 AM EST on Friday is expected to increase 0.5% versus a gain of 0.7% in January.

Canadian January Retail Sales to be released at 8:30 AM EST on Friday are expected increase 1.3% versus a drop of 0.8% in December.

February New Home Sales to be released at 10:00 AM EST on Friday are expected to increase to 620,000 units from 593,000 units in January.

Tomorrow we will find out what the ongoing US central bank policy will be going forward. What new Fed Chairman Powell decides on Wednesday will be a major driver of Stocks, Bonds and Gold for the forseeable future. This analysis covers both the playbook from the Fed and how each individual market is set to absorb change – R. Zurrer for Money Talks

Tomorrow we will find out what the ongoing US central bank policy will be going forward. What new Fed Chairman Powell decides on Wednesday will be a major driver of Stocks, Bonds and Gold for the forseeable future. This analysis covers both the playbook from the Fed and how each individual market is set to absorb change – R. Zurrer for Money Talks

March 20, 2018

1. It’s very important for gold, bond, and stock market investors to stay focused on the main fundamental price drivers and ignore what may feel exciting but is largely irrelevant to price discovery. Citizen demand from China/India and US central bank policy are the main price drivers for gold.

2. From 1960 to 1980, US recessions were generally inflationary, and the Fed raised rates during that period. Since then, recessions have carried a deflationary theme, and interest rates have fallen.

3. In 2013 I began suggesting that the Fed was going to end its deflationary QE and rate cutting programs. A new era of rate hikes and quantitative tightening would begin, resulting once again in inflationary US recessions.

4. I’ll dare to suggest that America is now poised to experience its first inflationary recession in almost three decades. Importantly, this is happening while Chinese and Indian citizen demand for gold is beginning to rise after a multi-year lull.

5. Ben Bernanke created enormous Main Street deflation with his QE and rate cutting policy. He incentivized corporations to engage in massive stock buyback programs while the Fed itself used printed money to buy government bonds. Small bank regulation made it unprofitable to make loans to small business. Main Street deflated, the labour force participation rate collapsed, and financial assets soared.

6. Please click here now. Double-click to enlarge this important labour force chart.

{kind=link}

{kind=link}

7. I’ve described Janet Yellen as the “Great Transitionist”. She tapered QE to zero as I predicted she would and began modest rate hikes. It’s clear that the US labour force participation rate bottomed during her tenure as Fed chair.

8. Jay “Mr. Hyde” Powell is poised to take her policy to the next level, and launch aggressive QT (quantitative tightening) and rate hikes, and the first of at least eight rate hikes should come tomorrow!

9. Wage inflation is poised to surge as the participation rate breaks out to the upside. Unfortunately, because Janet moved so slowly with her rate hikes, this wage inflation is going to occur as the US business cycle rolls over, creating an inflationary recession.

10. What does this mean for gold investors? Well, I think a celebratory drum roll is what it means! That’s because nothing is more positive for gold stocks than a long period of stagflation.

11. Against a background of a major resurgence in Chindian citizen demand for gold with stagnant mine supply (except for Russian and Canadian mines), a true “bull era” for gold, silver, and companies involved in all facets of the metals business is born!

12. Please click here now. Double-click to enlarge this Dow chart. I chart sixty major US stocks, including all thirty Dow Jones Industrials Average component stocks. What I’m seeing is a major breakdown in the health of the market. The market is being carried by fewer and fewer stocks.

{kind=link}

13. QT and rate hikes are sucking the life out of the market, and I’ve wondered aloud if Jay Powell’s words to stock market investors should be, “Sell in May, or get blown away by Jay!” The bottom line is that Mr. US Stock Market will have his first meeting with Mr. Hyde tomorrow, and I doubt it goes well for Mr. Market.

14. The meltdown in breadth doesn’t mean the US bull market in stocks is finished right now, but with the US bond bull market already slain by QT and rate hikes, it’s just a matter of time before Jay Powell pulls the US stock market’s life support plug. I’ve repeatedly told my subscribers that when investment decisions are made, forget about Trump, and focus on the Fed. Simply put, focus on the Fed, or wind up financially dead!

15. Investors need to think outside the stock and bond market box to prosper in an inflationary recession. On that note, please click here now. I wasn’t the earliest bitcoin investor, but I certainly was an aggressive bitcoin accumulator in the sub $500 zone.

{kind=link}

16. Bitcoin currently trades at about $8000. After establishing a core position with an average price of about $200, I’m obviously thrilled to be sitting in “forty bagger” mode today. Blockchain enthusiasts who enjoy this type of sustained wealth building fun can join me at my www.gublockchain.comwebsite.

17. It’s important for all investors to understand that at about $20,000 a coin, bitcoin threatened to steal thunder from mainstream media’s darling Dow Jones Industrial Average. An enormous regulatory drive was promptly launched in conjunction with the launch of five-coin bitcoin futures. An expected price correction was created by the regulators. These regulators don’t help investors. They just help themselves by getting salaries to perform useless tasks. Regardless, markets tend to be “here to stay” once these pencil pushers get involved. The bottom line is that regulation lets institutional investors embrace the asset class, and that’s happening now.

18. Of great interest to me is the major double bottom that is forming now on the daily bitcoin chart. Importantly, there’s a huge volume spike on the first decline to my $8000 – $5000 buy zone. Volume is low on the second decline to that same $8000 – $5000 area. The volume pattern and the time frame of one to two months between the bottoms is classic “Edwards & Magee” technical action!

19. Tom “Mr. Bitcoin” Lee (Ex head of US equities for JP Morgan) just issued a fresh bitcoin target of $90,000 by 2020. That’s possible, albeit aggressive. My intermediate term target of $34,000 is more moderate, more likely to happen, and still a superb gain from current price levels.

20. In a stagflationary environment like the one beginning now, bitcoin and precious metals are mostly likely to earn the title, “assets of champions”. Please click here now. It’s very important for gold investors to stay focused on the US central bank, India, and China. Hallmarking and the new spot exchange in India are just two very positive long term drivers of higher gold prices. A “Gold Board” will be launched soon. This board could ultimately have the power to determine the gold import duty rate and other key policy that affects the global gold price.

21. My Chinese jewellery stocks that I cover at www.gracelandjuniors.com are soaring higher as Chinese citizen gold buying is accelerating. Australian miners are also doing reasonably well. Investors in most individual GDX and GDXJ component stocks and the “raw juniors” need the patience to wait for US wage inflation and more progress in the Chindian gold markets. Then they can sink their teeth into the glory of new highs across the board for these stocks. It’s going to happen, but realism and patience are required. The seeds of inflation are being sown now. It’s not realistic to demand those seeds become jack in the beanstalk trees too quickly.

22. Please click here now. Double-click to enlarge this impressive daily gold chart. With “Jay Day” (FOMC decision day) tomorrow, gold is performing admirably in its post Chinese New Year trading. It’s making a beeline towards my $1300 Jay Day target zone. I expect statements from Jay Powell to set the stage for a move above the ultra-important $1370 area resistance zone. That should usher in substantial buying from Chinese citizens who have been quiet for the past few years.

{kind=link}

23. Please http://graceland-updates.com/images/stories/18mar/2018mar20gdx1.png. I’ve predicted that wage inflation an upturn in US money velocity should arrive by the summer if Jay Powell sticks to his projected actions.

{kind=link}

24. Most gold investors are not focused enough on buying their favourite gold stocks in the current $21 buy zone for GDX. Instead they are trying to guess when a big parabolic price rise will occur. That type of price action starts at the end of an inflationary period, not the beginning of it. I will say that I’m particularly excited to see substantial insider buying take place now at major gold mining companies. These company directors obviously see the current time as one for major gold stock accumulation. I’ll dare to suggest gold bugs around the world need to follow that lead!

Thanks

Stewart Thomson

Graceland Updates

Special Offer For Money Talks: Please send me an Email to freereports4@gracelandupdates.com and I’ll send you my free “The Ultimate Gold Stock Portfolio” report. I highlight eight of the most important gold stocks that investors should be holding right now, to profit as gold surges over $1370!

https://www.gracelandupdates.com

Email:

Stewart Thomson is a retired Merrill Lynch broker. Stewart writes the Graceland Updates daily between 4am-7am. They are sent out around 8am-9am. The newsletter is attractively priced and the format is a unique numbered point form. Giving clarity of each point and saving valuable reading time.

Risks, Disclaimers, Legal

Stewart Thomson is no longer an investment advisor. The information provided by Stewart and Graceland Updates is for general information purposes only. Before taking any action on any investment, it is imperative that you consult with multiple properly licensed, experienced and qualified investment advisors and get numerous opinions before taking any action. Your minimum risk on any investment in the world is: 100% loss of all your money. You may be taking or preparing to take leveraged positions in investments and not know it, exposing yourself to unlimited risks. This is highly concerning if you are an investor in any derivatives products. There is an approx $700 trillion OTC Derivatives Iceberg with a tiny portion written off officially. The bottom line:

Are You Prepared?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair