About the Author

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com.

The renowned financial expert John Mauldin who put together this conference has sent out this summary of the thinking of 14 different analysts as well as the forecasts of both Biotech and Crypto Currency panels. Interesting thoughts, well worth reading – Robert Zurrer for Money Talks

David Rosenberg

David Rosenberg

For the 10th year running, Gluskin Sheff Chief Economist and Strategist David Rosenberg was the leadoff hitter at the SIC—and he had a warning for investors.

Rosenberg believes that the US is in the very late stages of the business cycle and that investors should now be de-risking their portfolios. He suggested that investors should be focusing on companies with high earnings visibility and low debt ratios.

On the macroeconomic level, Rosenberg said that long-term deflationary trends such as adverse demographics and high debt levels are stronger than ever. Given these trends, he thinks that the current uptick in inflation is little more than a transitory spurt and will soon fade away.

Finally, Rosenberg said that Gluskin Sheff, which has $9 billion in assets under management, recently moved to 25% cash across all their portfolios.

Louis Gave

Up next was Louis Gave, CEO of Hong-Kong based Gavekal. Gave has consistently been one of the highest-rated speakers at the SIC, and he didn’t disappoint with some unique insights into what is happening in China.

Gave pointed out that China is currently going through a huge economic paradigm shift, one which has profound investment implications.

For the past few decades, the incentive in China has been to grow as quickly as possible. But going forward, China’s incentives will be based around what President Xi Jinping has called a “Beautiful China.”

This means a more sustainable growth model with less use of materials such as concrete and coal.

Gave believes that this shift plays into China’s imperial ambitions—and that’s a trend he is investing around. He went on to suggest that investors should be looking at Chinese financial and consumer stocks, plus countries that will benefit from the One Belt, One Road infrastructure build-out.

Global Investing Panel

The first panel of the SIC 2018 was a discussion around global financial trends with David Rosenberg, Grant Williams, and Louis Gave.

The first topic of discussion was the recent tariffs enacted by President Trump. Gave said he has opened a “Pandora’s box” for international relations and the tariffs could have a serious impact on the financial market.

The panel also discussed gold, with some split views on the yellow metal.

Gave said he doesn’t like gold as an investment but that he looks to it as a signal that emerging markets are growing. On the other side, Grant Williams suggested that with inflation picking up, now is an excellent time to own gold.

On the issue of international relations, when asked if they were worried about North Korea, all three panelists said no.

However, Gave and Rosenberg agreed that growing tensions between Saudi Arabia and Iran are reason for concern. Gave commented that if the tensions turn into a greater issue, oil prices could jump.

Patrick Cox, editor of Mauldin’s Transformational Technology Alert, and Karen Harris, managing director of Bain & Co’s Macro Trends Group, opened the show after lunch.

Cox said he sees a perfect storm brewing. The impact current anti-aging and life-extension research will have on society is almost something out of science fiction—but it’s actually happening. And it’s coming a lot sooner than most people think.

Although Millennials are about to outnumber Baby Boomers, the old-age dependency ratio—the number of retirees being supported by young workers—is rising. The young are paying the bills of the old. Will they rebel against this intergenerational problem?

Healthcare is driving growing budget deficits and medical costs. Regenerative medicine is the only answer, Cox said. He believes that this imperative will drive radical regulatory change and get these drugs and therapies to market far faster.

Biotech Panel

Eric Verdin, president and CEO of The Buck Institute for Research on Aging, showed how genes control lifespan. Research from the Buck Institute points to the impact of gene mutation on longevity. In his argument, he drew on lab results that produced a 35% life extension in mice.

Michael West, CEO of BioTime, talked about how the lion’s share of healthcare costs is spent fighting chronic diseases. In a lab setting, scientists have been able to reverse the aging process in cells. This cell process, said West, is now firmly under human control.

Aubrey de Grey, chief science officer of the SENS Research Foundation, parsed the critical differences between gerontology and geriatrics—things that happen throughout life versus those that happen at the end of life. Understanding the differences are crucial to how we approach the diseases of aging.

Niall Ferguson

Ferguson used the metaphor of an ancient city, and the difference between squares, where people meet, and towers, where the power resides.

For tech optimists, things did not go quite as they planned. An increasingly connected world should have led to an awesome world, but it didn’t work out that way. The power was not shifted to the “squares.”

The obvious question is, why should connecting the entire world make it a better place? Connectedness has instead disrupted political hierarchies. Without tools like Twitter, campaigns like Donald Trump’s would not have won. Social media made the difference.

Connectedness has created huge, monopolistic networks, Ferguson said, “and it will take a network to defeat a network.”

In the network battlefield, the winner takes all. The financial crisis was a global network crisis. In a hyper-connected world, is the status quo sustainable?

David McWilliams

Upheaval and change is not new; it happens all the time. McWilliams, economist and best-selling author, related this to the words of William Butler Yeats, who wrote that the center falls apart while the best people are silent, and the worst of society takes over.

None of the people paid to predict the future were right, said McWilliams. At the tipping points, when things are fragile, it is the unconventional thinker that sees the world clearly and holistically. We need unconventional thinkers today—but do we reward or punish them?

McWilliams drew a connection to the types of brains rewarded in academia. It is the linear thinkers that are encouraged, he stated. The result is that millions of people leave school feeling clever. They go into banking, the military, or become economists… and we employ them. Then we end up with group-think at the top of organizations.

The most conventional thinkers being economists is very dangerous at a time like today, he said.

Panel with Niall Ferguson, David McWilliams, and Our Own John Mauldin

When asked about volatility, Ferguson said he thinks the Fed is coming off of its role in volatility suppression.

McWilliams talked about the old link between monetary policy and inflation being broken. He sees the interplay of human behavior and economics as being out of sync.

Ferguson noted that people invested in financial models but had unexpected results. One example is QE, when the anticipated inflation did not happen.

The conversation moved to the populist backlash seen in the US and Europe, and Ferguson warned that it is not temporary—it will continue, but in unknown directions. Will it produce even more radical outcomes? Will it end like the final days of the Roman Empire?

It is extraordinarily hard to predict political outcomes. It introduces uncertainty into the process of solving problems—and looking to the historical models for help will not work.

The question of decentralization as it applies to blockchain tech was raised. This question leads us to another: Will we look back on this period and think how wrong we got the blockchain story?

Day 2

Events began this morning with an investor’s dream duo of Steve Blumenthal and JPMorgan’s Gabriela Santos.

Steve kicked-off proceedings with a discussion around valuations and why they paint a negative picture for returns going forward.

Throughout history, when valuations have been as high as they are today, returns have been in the low single digits or negative over the next decade. Thus, Blumenthal said investors should now be focusing on risk management and went through specific ways to do just that.

JPMorgan Asset Management’s Gabriela Santos picked up where Steve left off, talking about asset allocation. She said investors should be focused on emerging market equities, specifically Latin America.

Jared Dillian and I

Up next was my one-on-one discussion with Jared Dillian. Jared walked out to the Bee Gees “Staying Alive.” Why?

During the recent stock market correction, Jared quipped to me that investors need to be focused on “staying alive” because we are now entering a regime change in the markets.

To highlight just how important avoiding losses are, Jared read the audience a letter he received in response to a Bloomberg article he penned. In the letter, the individual investor said they had lost over $400,000 in just a few hours during the recent correction.

Always the contrarian, Jared left attendees with, “You want to do the trade that gets you laughed off CNBC.”

Neil Howe and John Mauldin

Then our own John Mauldin sat down with top demographer Neil Howe and discussed the generational strife in the US.

Baby Boomers have reaped the rewards from the secular bull market in financial assets and now own half of all the wealth in America. However, other cohorts haven’t done so well, and Neil said that means increasing inter-generational tensions going forward.

Neil left the crowd by saying the number one thing he is watching today is inflation.

George Friedman

Geopolitical futures chairman George Friedman took the stage for the final session on the morning of day 2—and he painted a negative picture for global relations.

George said the number one trend he’s focusing on today is the global export crisis, which has wide-ranging investment implications.

While large exporters such as Germany and China do well when the global economy is strong, George said demand and consumption are now stagnating—which is terrible for them. For example, exports account for over 50% of Germany’s GDP.

George went on to say that globalization has created a social crisis in developed countries, and that means we are likely to see continued political upheaval.

The analysis into the trends shaping financial markets, the economy, and international relations by the speakers have been outstanding so far.

Jeffrey Gundlach

DoubleLine Capital CEO, Jeffrey Gundlach who said that financial markets and the economy are facing a “moment of truth.”

Gundlach delved into several reasons why he believes the secular bond bull market is likely over. He points to the explosion in the US government budget deficit, the Fed’s balance sheet roll-off, and rising inflation as the reasons why.

Gundlach believes that rising bond yields, coupled with sky-high valuations, are a toxic mix for US equities.

But the “Bond King” wasn’t bearish on all equities, saying that certain sectors in emerging markets look attractive.

Grant Williams

Next up was crowd favorite Grant Williams, founder of Real Vision TV and author of Things That Make You Go Hmmm…, who dissected monetary policy and its long-term implications.

While quantitative easing (QE) has suppressed volatility and was very good for financial assets like stock and bonds, that trend is about to reverse.

With the Fed expected to hike interest rates four times this year, plus reduction of their $4.4 trillion balance sheet, rates are rising—fast! In less than 12 months, short-year Treasury yields have more than doubled.

Williams then discussed how investors should be allocating capital in this environment and offered some specific trade ideas for the audience.

Cryptocurrency Panel

The cryptocurrency panel followed with founder and CIO of Passport Capital, John Burbank, best-selling author and co-founder of the Discovery Institute, George Gilder, CEO and CIO of US Global Investors, Frank Holmes, and co-founder and CEO of Genesis Mining, Marco Streng, moderated by our own Jared Dillian.

The panel delved into several aspects of cryptocurrencies and blockchain technology—including the “business” side of mining Bitcoin, and how institutional investors are thinking about trading it.

Holmes, who recently made a multi-million-dollar investment in the world’s first publicly listed blockchain infrastructure company, went on to discuss how the transition to “immediate” and “digital” assets by Millennial and younger generations is changing the paradigm for markets.

George Gilder and John Mauldin

John Mauldin started with one of his favorite George Gilder observations, “The source of all wealth is information.” Gilder added that capitalism is not a scheme of rewards, it’s an information system. That takes us to the axiom: Wealth is knowledge.

Gilder gave us the sweeping example that the difference between our age and the stone age is entirely the gathering of information.

Mauldin asked about equilibrium. Gilder equates it to information theory. Expect surprises from outside the database—that is the genesis of the surprise. Information is disorder—the surprise—it is not equilibrium.

Mauldin added that economists assume equilibrium as part of their models. When in reality, the markets exist in a state of chaos.

George Gilder is an immensely deep thinker, and capsulating his thoughts on these pages is immensely difficult. You really have to be part of the discussion to get its full impact.

ETF Panel: Steven Bregman, Stephen Cucchiaro, Jan van Eck, Jared Dillian moderator.

Asked if explosive asset growth can continue, van Eck, president and CEO of Van Eck Associates, thinks it can, given the pressure to keep costs low. ETFs have invaded the financial system and are here to stay. Cucchiaro, president and CIO of 3EDGE Asset Management, added that ETFs and passive strategies grew together, but won’t necessarily remain so.

The ETF panel discussed risks embedded in leveraged ETFs and volatility ETFs/ETNs. All agreed they are complex and widely misunderstood. Van Eck pointed out that it’s dangerous to expect regulators to stop such products. Brokers have a suitability requirement and it is their role to prevent investors from taking excessive risk.

Of course, if you can’t tune in live but still want to access the video recording of the panel (and all the others from the conference), the Virtual Pass has you covered.

This analyst argues the HUI is going to drop down tor the 100 level at which point the opportunity in mining stocks willl be one in a lifetime. As he says “this may sound ridiculous, but the HUI at 200 sounded just as ridiculous when it was trading above 500 in late 2012. Yet, a year later, that’s exactly the value that we saw”. All 10 charts will enlarge with a click. – Robert Zurrer for Money Talks

The price of no asset can move up or down in a straight line, so why should mining stocks be any different? They have been declining relentlessly for almost 2 weeks, erasing more than 10% of their value. Sharp? Definitely. Unsustainable? Perhaps. When will the turnaround take place? It depends.

The price of no asset can move up or down in a straight line, so why should mining stocks be any different? They have been declining relentlessly for almost 2 weeks, erasing more than 10% of their value. Sharp? Definitely. Unsustainable? Perhaps. When will the turnaround take place? It depends.

It depends on the bullish signs and confirmations that we get. The correct question to be asking now is: “Why do we need any confirmations at all?” The reply is that because the situation is tense as there are good reasons for both a turnaround in a day or two and a continuation of the decline without a meaningful correction.

Before moving to the above details, we would like to give you an update on the gold-stock link. Let’s start with gold’s price compared to the S&P 500 Index (charts courtesy of http://stockcharts.com).

.png)

As we explained previously, there’s one thing that – right from the start – differentiates between the two kinds of reaction: stocks declining along with gold and stocks triggering a rally in gold. Autocorrelation. Autocorrelation is a fancy way of saying that what happens first makes the same reaction likely, which makes the follow-up to the follow-up likely to be the same as well – and so on. In other words, the way gold initially reacted to the decline in the S&P 500 was the way in which it kept on reacting in the following weeks and – sometimes – months.

What kind of price action did we see in the previous several days (not only yesterday)? On average, the S&P declined along with gold. So, what’s the likely impact that a declining stock market is going to have on the precious metals market? It’s likely going to be negative in the following weeks and – perhaps – months.

At this point, you may correctly ask: “If that’s the case, then why didn’t gold decline on Monday?” There are several reasons as to why this was not the case.

The simplest one is that the relationship described in the previous paragraph is supposed to work on average, but it doesn’t mean that gold and the S&P will move in the same direction on every single day. The metals didn’t react by soaring higher on Monday – they moved up rather insignificantly. Plus, miners were lower anyway.

The second thing is that Monday’s session was particularly volatile – something that investors were not prepared for emotionally. Some of them had probably bought gold and silver in hope of hedging themselves. After the session it turned out that it was not that helpful (the S&P was down 4%, while gold was almost flat, moving higher by less than 0.5%), so the following days of the general stock market’s decline may be characterized be much smaller willingness of the investors to purchase precious metals in hope of hedging their stock portfolios.

Yesterday’s session served as a confirmation of the “on average” type of link. On Monday stocks declined severely, while gold moved a bit higher. During yesterday’s session stocks moved a bit higher, but gold declined almost $20. On average, both assets declined. The link, as well as the bearish implications, remains intact.

.png)

Moreover, even though the gold to S&P 500 ratio moved higher, there was no invalidation of the previous breakdown – only a move back to the previously broken support / resistance line. The 2016 and 2017 lows seem to provide strong resistance, just as they provided strong support in the previous years. The implications are bearish for the ratio and for the precious metals sector.

.png)

As far as silver is concerned, we see a corrective upswing that follows a sharp slide and a breakdown below the previous lows. A corrective upswing is something very natural at this stage of the decline and should not be viewed as a reversal.

We marked similar situations with black rectangles. Virtually all big declines had this kind of pause before the slide continued, so seeing one now is definitely nothing odd or bullish. Interestingly, in two cases (April 2017 and June 2017) silver corrected from below the 50-day moving average to slightly above it only to plunge in the following days. So far, the price action is similar.

Please note that the pauses didn’t take more than a couple of days, so it seems that this pause is over or about to be over.

Having said the above, let’s move to the questions that we raised in the opening paragraph of today’s analysis. We wrote that the situation is tense as there are good reasons for miners to reverse sooner rather than later and that there are reasons for the decline to continue. Let’s see them in detail.

.png)

In the case of the gold stocks to gold ratio, we definitely have bearish implications. It was already after Monday’s closing price that we saw a small breakdown below the 2017 and 2016 lows, however, based on yesterday’s decline, the breakdowns are now clearly visible.

This opens the road to much lower valuations. Still, let’s not forget that verifications of breakdowns happen from time to time. For instance, in late October 2017, the ratio broke below the previous lows and consolidated before diving deeper. This corresponded to a relatively small – but still – corrective upswing in gold.

Then again, the above might have simply been a result of the cyclical turning point in gold (and in mining stocks). Consequently, it’s not clear if the preceding breakdown resulted in a verification, which in turn resulted in a small rally in gold. It seems more likely that it was the other way around. Gold and miners reversed their courses temporarily because of the turning point, but the corrective upswing was relatively small as – among other factors – the HUI to gold ratio was after a major breakdown and thus, there was a limit to how high the ratio and gold were eager to rally.

So, the question becomes, if we have a turning point nearby.

.png)

Not really, we already had one at the beginning of the month and it seems that the turnaround that preceded the turning point was the development that was likely to happen based on it.

Wait, there are turning points for mining stocks as well?

In short, yes, but it’s nothing entirely new – the turnings point for mining stocks are the turning points for gold, with additional sub-cycles in between.

We’ve been recently asked if it’s true that mining stocks have turning points between the 4th and the 10th day of the month. The reply is that this was the case in the previous year – but it’s moving toward the scenario in which the turning points are seen at or very close the end of the month. Consequently, the next turning point is not this week, but it’s already behind us and the next one is at the end of February and the beginning of March.

In other words, there’s not much more to the 4th to 10th day of the month rule – it’s a cycle that will likely be continued, but the above rule will likely not. If you’ve been following our analyses for some time, you knew about this cycle all along (precisely, about every other cycle as that’s what appeared most useful for the gold market).

The additional thing that we can see on the above chart is that the volume that accompanied yesterday’s decline was quite sizable, so the bearish implications of the price-volume link remain in place.

So, based on the gold stocks to gold ratio and the turning points for mining stocks (GDX, HUI and XAU), it doesn’t seem that the turnaround has to be seen shortly or that it’s likely.

Still, let’s keep in mind that if the current bearish momentum persists, mining stocks will reach their 2017 lows very soon. The RSI indicator is already close to the 30 level and since reaching it is a classic buy signal for the short term, we may see at least a corrective upswing soon.

Overall, based on the previous two charts, it seems that we may indeed see a corrective upswing once miners move to (or very close to) their 2017 lows, but it’s not likely that the upcoming rally will be anything significant.

The long-term HUI Index chart shows that one should indeed think at least twice before trying to time the upcoming correction.

.png)

Let’s start with the thing that’s easiest to interpret. We just saw a long-term sell signal from the Stochastic indicator. Last year we saw it only twice and, in both cases, a big decline followed. This was the case also multiple times in the preceding years. Consequently, the implications here are bearish.

The thing that’s more complex, but also more rewarding from the analytical point of view, is the continuation of the analogy to the 2011 – 2013 period.

The 2011 and 2016 tops were preceded by substantial rallies, but they were shortly followed by big and sharp declines, and then by corrective upswings. This, by itself, is not enough to view these situations as similar, but the additional details are. These additional details are the sizes of the corrective upswings (about 50% in both cases as marked using Fibonacci retracements) and the – approximate – time that it took for the corrections to materialize. We marked the latter using red dashed lines. As you can see, the horizons are almost identical.

The declining purple, dashed line is a line connecting the top with the top of the first local move up during the decline. In this case, the price that was reached is correct only approximately and the time seems to be off for more than a month. The latter seems to be a violation of the analogy, but please keep in mind that the last couple of weeks were characterized by a sharp slide in the value of the USD Index that was only reflected in the PM prices to a small extent. In fact, in terms of the euro, gold topped very early in January, and taking this date into account would imply only a small deviation in the analogy present on the above chart. Overall, it seems that we can still view the analogy as present.

The interesting fact about both initial local tops during the correction (the late-2012 one and the most recent 2018 one) is that they formed close to previous local tops.

What are the overall implications of the above? We should expect a big and volatile decline to follow. Last week’s performance and what we’re seeing this week seems to be just the very first sign of what’s to come. If the 2013 move is repeated, then we are likely to see the HUI Index well below the 100 level before the bottom is really in.

This may sound ridiculous, but the HUI at 200 sounded just as ridiculous when it was trading above 500 in late 2012. Yet, a year later, that’s exactly the value that we saw.

What does the above imply for the near term? Back in 2013, there was no visible corrective upswing until the HUI broke below the previous major low (the 2012 low). The analogous low is the late-2016 bottom, which is relatively far. So, if the analogy is to continue, then gold miners may move significantly lower without a bigger move higher.

Summing up, the outlook for the precious metals market is bearish for the following weeks and it seems that even if we see a corrective upswing shortly, it will not be anything spectacular. At least not until gold stocks move to their 2017 lows.

On a side note, please note that our bearish comments on the precious metals sector doesn’t make us an enemy of gold and silver investors – it makes us a true (!) friend. If you ask your friends how you look before going to an important meeting, everyone will tell you that you look great regardless of the truth as they will prefer not to be the ones that ruin your mood by saying something unpleasant. But a true friend will tell you how things really are, so that you can fix something before your leave. This may be unpleasant, but ultimately, it’s the second approach that benefits you.

Most gold promoters will want you to think that gold is going to go higher no matter what happens and all you should do is buy, buy, buy. And then buy some more. They don’t want to risk upsetting you. But not us. We’re that true friend that tells you what they think and why, regardless of the possibility of being unpleasant – so that you can benefit more. In this case, if we’re correct about the bearish outlook for the precious metals, it will be much more profitable to be buying at lower prices than at the current ones.

So, in our view, the outlook for the precious metals market is friendly bearish. The precious metals market is likely to move much higher in the coming years, but if we’re correct about the medium-term decline first, then the best buying opportunity is still ahead of us.

A great, clear analysis of previous bubbles, bear markets & crashes and the ultimate conclusion of the Fed’s desire to prevent any of the two negatives in that troika from ever occuring again. Lance Roberts is a Chief Portfolio Strategistand Chief Editor of the “Real Investment Advice” – Robert Zurrer for Money Talks.

My…my…how quickly we forget.

My…my…how quickly we forget.

Yesterday, as the markets rocketed higher, my email lit up with questions surrounding the discussion from this last weekend’s newsletter.

“I have questioned over the last couple of weeks exactly how much volatility the Fed would allow before stepping into the fray to keep the markets stable.

We now know it is roughly a 10% decline.

Specifically were the comments about QE being ‘useful to have in the toolkit for those times when the short-term interest rate tool may not be available,’ adding that the Fed is ‘quite likely’ to require large-scale asset purchases again because real rates will remain low due to slow productivity and labor-force growth. They also added that ‘if LSAPs are indeed not effective, then the Fed may need to take other measures.’ (Zerohedge has the complete article.)

In other words, despite the rhetoric to the contrary, the Fed isn’t going away…….ever!”

The deluge of emails revolved around much of the same premise.

“If the the Fed isn’t going away, then why would there ever be another bear market?”

It is certainly an interesting question, particularly as the Fed continues to trot out officials to make market supporting statements such as Fed Vice Chairman Quarles who stated on Monday:

“It might seem reasonable to assume that faster growth would lead to firmer inflation. However, I think a lot remains to be seen.”

Or even Mario Draghi, Chairman of the ECB, who said:

“In the presence of an economic situation that is improving constantly, we need the right blend of measures. Uncertainties continue to prevail.”

So, despite economies that are supposedly improving, Central Banks continue into their tenth year of “emergency measures.” As Michael Lebowitz recently stated:

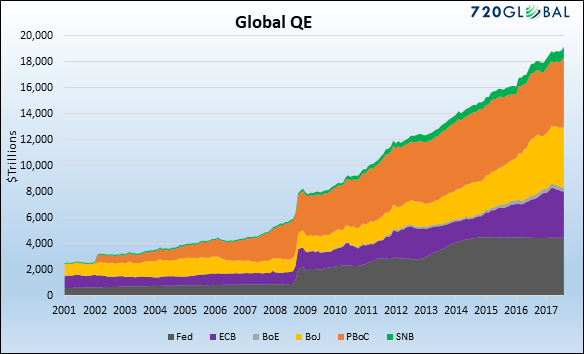

“Global central banks’ post-financial crisis monetary policies have collectively been more aggressive than anything witnessed in modern financial history. Over the last ten years, the six largest central banks have printed unprecedented amounts of money to purchase approximately $14 trillion of financial assets as shown below. Before the financial crisis of 2008, the only central bank printing money of any consequence was the Peoples Bank of China (PBoC).”

With that, I certainly understand the reasoning that if indeed “Central Banks” are now committed to monetary interventions going forward, the financial markets have been effectively “fire-proofed against bear markets.”

But such a belief is extremely dangerous.

It is also the same “belief” every major bubble was built upon throughout history and driven by the same underlying foundations.

Which created the bubble in “THE” asset class of choice at that time…

Which created the bubble…

Which always ended badly for investors.

Every. Single. Time.

Is “this time different?”

No, and it will end just the same as every previous liquidity driven bubble throughout history.

Of this, there is absolute certainty.

There are only TWO questions that must be answered:

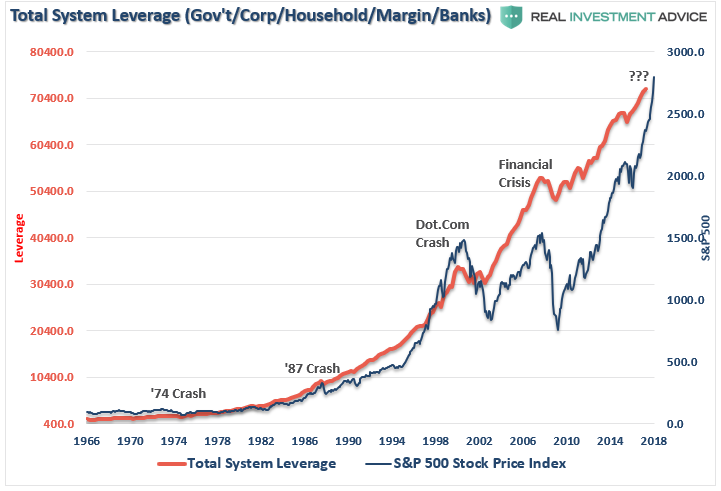

No one knows for certain what will cause the next financial crisis. However, in my opinion, the most likely culprit will be a credit-related event caused by the Fed’s misguided policy of hiking interest rates,and tightening monetary policy, when the financial system is more heavily levered than at any other point in human history.

The illusion of liquidity has a dangerous side effect. The process of the previous two debt-deleveraging cycles led to rather sharp market reversions as margin calls, and the subsequent unwinding of margin debt fueled a liquidation cycle in financial assets. The resultant loss of the “wealth effect” weighed on consumption pushing the economy into recession which then impacted corporate and household debt leading to defaults, write-offs, and bankruptcies.

With the push lower in interest rates, the assumed “riskiness” of piling on leverage was removed. However, while the cost of sustaining higher debt levels is lower, the consequences of excess leverage in the system remains the same.

You will notice in the chart above, that even relatively small deleveraging processes had significant negative impacts on the economy and the financial markets. With total system leverage spiking to levels never before witnessed in history, it is quite likely the next event that leads to a reversion in debt will be just as damaging to the financial and economic systems.

Since interest rates affect “payments,” increases in rates negatively impact consumption, housing, and investment which ultimately deters economic growth.

It will ultimately be the level of interest rates which triggers some “credit event” that starts the “next bear market”

It has happened every time in history.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will force investors to dump positions to meet margin calls at a time when the lack of buyers will create a vacuum causing rapid price declines.

Honestly, no one knows for sure. However, history can give us some guide.

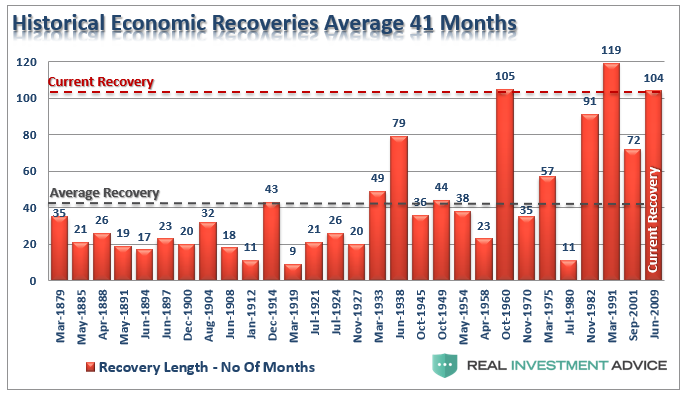

“In the past six decades, the average length of time from the first tightening to the end of the business cycle is 44 months; the median is 35 months; and the lag from the initial rate hike to the end of the bull equity market is 38 months for the average, 40 months for the media.” – David Rosenberg

Averages and medians are great for general analysis but obfuscate the variables of individual cycles. To be sure the last three business cycles (80’s, 90’s and 2000) were extremely long and supported by a massive shift in financial engineering and a credit leveraging cycle. The post-Depression recovery, and WWII, drove the long economic expansion in the 40’s, and the “space race” supported the 60’s.

Currently, employment, economic and wage growth remain weak with 1-in-4 Americans on Government subsidies and the majority living paycheck-to-paycheck. This is why Central Banks, globally, have continued aggressively monetizing debt in order to keep growth from stalling out. With the Fed now hiking rates, and reducing market liquidity, the risk of a policy mistake has risen markedly.

If David is correct, given the Fed began their current rate hiking campaign in December 2015, the next recession would occur 38-months later or February 2019. Such a span would make the current economic expansion the second longest in history based on the weakest economic growth rates.

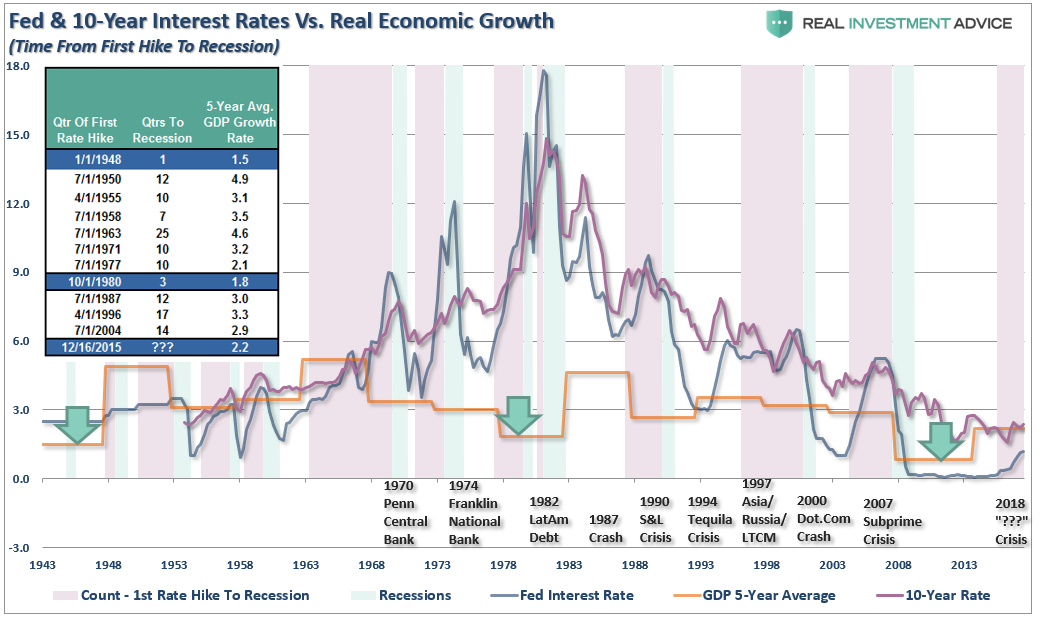

The chart and table below compares real, inflation-adjusted, GDP to Federal Reserve interest rate levels. The vertical purple bars denote the quarter of the first rate hike to the beginning of the next rate decrease, or onset of a recession.

If you look at the underlying data, which dates back to 1943, and calculate both the average and median for the entire span, you find:

The importance of this reflects the point made previously, the Federal Reserve lifts interest rates to slow economic growth and quell inflationary pressures. Yet, economic growth and inflation are running well below historical norms and system-wide leverage has surged to new records as individuals and corporations have feasted on debt in a low-rate environment.

That is now changing as the Fed hikes interest rates. Notice in the chart above, that recessions occur when the Fed starts hiking interest rates and the Fed rate approaches the 10-year Treasury rate. In every instance, a recession or “crisis” occurred.

If historical averages hold, and since major bear markets in equities coincide with recessions, then the current bull market in equities has about one year left to run. While the markets, due to momentum, may ignore the effect of “monetary tightening” in the short-term, the longer-term has been a different story.

As shown in the table below, the bulk of losses in markets are tied to economic recessions. However, there are also other events such as the Crash of 1987, the Asian Contagion, Long-Term Capital Management, and others that led to sharp corrections in the market as well.

The point is that in the short-term the economy, and the markets (due to momentum), can SEEM TO DEFY the laws of gravity as interest rates begin to rise. However, as rates continue to rise they ultimately act as a “brake” on economic activity.

While rising interest rates may not “initially” impact asset prices, it is a far different story to suggest that they won’t. In fact, there have been absolutely ZERO times in history that the Federal Reserve has begun an interest rate hiking campaign that has not eventually led to a negative outcome.

What the majority of analysts fail to address is the “full-cycle” effect from rate hikes. While equities may initially provide a haven from rising interest rates during the first half of the rate cycle, they have been a destructive place to be during the second-half.

It is clear from the analysis that “bad things” have tended to follow the Federal Reserve’s first interest rate increase. While the markets, and economy, may seem to perform okay during the initial phase of the rate hiking campaign, the eventual negative impact will push most individuals to “panic sell” near the next lows. Emotional mistakes are 50% of the cause as to why investors consistently underperform the markets over a 20-year cycle.

The exact “what” and “when” of the next “bear market” is unknown. It has always been some unanticipated event that triggers the “reversion to the mean.”

It will be obvious in “hindsight.”

While the media will loudly protest that “no one could have seen it coming,” there are plenty of clues if you only choose to look.

The Fed has not put an “end” to bear markets.

In fact, they have likely only succeeded in ensuring the next bear market will be larger than the last.

For now, the bullish trend is still in place and should be “consciously” honored. However, while it may seem that nothing can stop the markets rise, or seemingly the Fed will never let it fall, it is crucial to remember that it is “only like this, until it is like that.”

For those “asleep at the wheel,” there will be a heavy price to pay when the taillights turn red.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter and Linked-In

Victor Adair forecasts the near term direction of Stocks, Treasuries, Gold and Currencies including the vital US Dollar. Wrapping up the action of the markets last and telling Michael exactly what posititions he has on now – Robert Zurrer for Money Talks

The DJIA topped out one month ago after a 45%+ rally since Trump’s election. The DJIA moved broadly sideways between 16,000 and 18,000 for most of 2014, 2015 and 2016 and then took off on a 14 month Run for the Roses parabolic burst to 26,618. Following that top the DJIA had a swift 11% correction (top to bottom) and an equally swift bounce back from the lows with the market now slightly above where it was at the beginning of the year.

I think the bounce back from the lows is a dead cat bounce and that we’ll see new lows for two reasons, 1) The 9 year bull market is long in the tooth and the recent parabolic price action looks to have defined a top and 2) the global accommodative

Central Bank policies that underwrote the bull market are reversing.

Risk appetite seems more defensive than aggressive following the correction and I think the “buy any dip” crowd will be trading smaller size and will be using tighter sell stops if they get long. The US Dollar, which had been trending lower since Trump’s election, has caught a bid the past couple of weeks and I think that’s another “risk off” indicator.

My short term trading: I began the week short CAD, gold and WTI. I liquidated CAD and gold for good gains but covered the short WTI at a loss. At the end of the week I’m short Euro (could just as easily have been short gold,) I’ve re-shorted CAD (on the CPI bounce) and I wrote short dated puts on US Treasury bonds.

I’m looking for the US Dollar to rally if/when risk appetite becomes more defensive. Market positioning remains very USD bearish so if it does start to rally it could have a big quick move. Jerome Powell’s “coming out” Congressional testimony this coming Tuesday could spark a USD advance.

The Canadian Dollar has been the weakest of the G10 currencies Vs. USD since risk appetite topped out in late January, but it may be getting some support from higher WTI prices…and it seems to be ignoring the widening USD interest rate premium. However the main “driver” of CAD will be the strength or weakness of the big dollar.

The Euro has had a 20%+ rally against the USD in the last 13 months. Massive Euro bullish speculative positions have been built in the currency futures markets despite the huge widening of the USD interest rate premium. If the market comes to see 1.25 as a top in the Euro it will be tough to sustain long Euro positions with ~3% annual negative carry. A break below 1.22 could ignite selling pressure.

WTI topped out around the end of January and (just like the stock market) had a swift 12% correction…BUT…the bounce back in WTI has been stronger than the stock market bounce. I’ve had a bearish bias on the WTI supply/demand/inventory story but I think I’m currently “missing something” in that analysis so I covered my WTI puts mid-week for a loss and I’m flat. Speculators remain massively long WTI…so if the price does start to break there could be some serious selling pressure from those positions throwing in the towel.

US Treasury Bonds: US interest rates have been steadily rising since the September 8/2017 Key Turn Date with the 10 year nearly touching the 3% yield level this week. Speculators have built a huge bearish position in the futures market. I think the market is oversold so I’ve sold very short dated OTM puts.

by Martin Armstrong

Armstrong, who has been very accurate on rising interest rates, and he impact they are having on pensions and Europe says he sees another banking crisis coming just as the United States is looking at a new radical bank rescue policy. A policy that will effect depositors rather than taxpayers

by Michael Campbell

According to the Finance Minister the budget is going to be fair. Of course it will be, as long as eveyone shares Trudeau and Morneau’s opinion. Mike on one of the most divisive characteristics of our society

The 3 charts below tell the story: Jack Crooks makes a powerful argument that the US Dollar has entered into a long-term bear market cycle which will trigger a massive BIG move in sold out commodities for the next 8 years

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

A sane voice in a scrambled investment world.

~ Ed R.

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair