Wealth Building Strategies

Sell to Whom?

Sell to Whom?

(Almost) Everything Is Awesome

Bending the Yield Curve

The Dangers of Passive Investing

Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

“Forget the past. The future will give you plenty to worry about.”

– George Allen, Sr.

“I try not to worry about the future, so I take each day just one anxiety attack at a time.”

– Tom Wilson

The middle ground can be uncomfortable. As someone now widely known as the “muddle-through guy,” I have learned this the hard way. My bullish friends call me a worrywart, and the bearish ones think I am Pollyanna incarnate.

The irony here is that I’ve never claimed to be a great trader or a short-term forecaster. I think I have a pretty good record of calling major turning points. Next week or next month is another matter. Anything can happen, and it probably will.

That said, the fact that my forecast may be wrong doesn’t prevent me from making one. So, with all the usual disclaimers, today I will review some recent analysis from my reliable sources and let you take a peek into my worry closet.

One point we all agree on: We live in unusual times.

Last week Doug Kass sent around an e-mail comparing today’s markets to Queen’s classic “Bohemian Rhapsody.” I know that seems odd, but it was actually a good fit. I shared Doug’s full message with my Over My Shoulder subscribers. For everyone else, the point is that, like the song says, “Nothing really matters” to whoever is buying stocks these days. They just keep buying and pushing prices higher. As Jared Dillian says, “It’s a bull market, dude!” Stock prices do go higher in a bull market; and sometimes, as the end approaches, they make value investors very uncomfortable.

Neither Doug nor I quite understand the “Nothing really matters” attitude, though we have some theories. Doug is probably more bearish than I am. He has a long list of open questions. I zeroed in on the last one, which is critical: “When ETFs sell, who will buy?”

The stratospheric ascent of passive indexing is having side effects that I suspect will make markets sick at some point. Passive investing is perverting the financial markets’ core economic function, i.e., efficient capital allocation. In terms of stimulating buying interest, a company’s fundamental business prospects are now much less important than its presence in (or absence from) popular indexes.

We’ve created this environment in which badly managed companies can still see their stock prices rise along with those of well-managed companies. The actual facts about a company don’t mean all that much in a passive-investing world. Capitalization-weighted indexes aggravate this already problematic phenomenon. Money is pouring into stocks like Apple (AAPL) and Amazon (AMZN) simply because they are big. The resulting higher prices make them bigger still, and they pull in yet more capital. Here’s a look at the five largest stocks in the S&P 500.

What about the QQQ or the NDX? The five stocks above represent 42% of the NDX and 13% of the S&P 500. That means every time you buy an index based on the NASDAQ, 42% of your money goes into just five stocks, leaving 58% for the remaining 95. By the time you get past the largest 25, you are under 1% per stock. Apple alone is 12% of the NASDAQ 100 Index and 4% of the S&P 500. That explains, in part, why the NASDAQ has outperformed the S&P 500.

For the record, Goldman Sachs researchers recently released a paper with a strong fundamental forecast for those stocks. That is, they expect them to continue to go up, absent a recession or something else that triggers a bear market. I keep scanning the horizons in every direction, and I just can’t see anything that would trigger more than a minor correction today. Of course, a minor correction could deliver outsized impacts, given the heavy weighting of a few stocks and passive index investing. Be careful out there.

Doug asks, “When ETFs sell, who will buy?” The ETFs of the world may quickly begin trading below their actual net asset values (NAV). This is called price discovery, and the arbitrageurs will not be slow to take advantage of that difference. This means the indexes will drop much faster than they have gone up. I am neither a fortuneteller nor the son of a fortuneteller, but there are a few things I’ve picked up along the way. One of them is that, next time, stocks are going to go down breathtakingly fast once they begin to roll over.

This bull can’t end well, but it will end. At that point, Doug’s question becomes critical: Who will buy? I don’t know, but someone will. Prices for good and bad stocks will drop to whatever levels attract buyers. The indexes will eventually fall lower than any of us think likely right now. Whether that will happen next month, next year, or next decade is anyone’s guess.

Sidebar: You should think of cash as an option on your ability to buy the stocks that will lose 50% of their value and suddenly become the value stocks of the future. The option value on your cash today is not that much. You don’t make much on it, but you don’t lose much holding it. The time is going to come when you will be glad you have a little cash to put to work. Think March 2009.

(Almost) Everything Is Awesome

While Doug was musing about Queen, Louis Gave was thinking about rugby. Should one go where the ball is now, or try to figure out where the ball will be?

Louis asks that question while noting that it has been extremely difficult to lose money this year. Almost every tradable asset class has been climbing. You are probably making good returns this year unless you have been:

Overweight energy and materials, and/or

Overweight financials.

Those have been the primary weak spots. Investors in everything from technology to emerging markets, to Europe and even utilities have done well. All you had to do was avoid energy, materials, and financials.

The reasons for this are pretty simple. Inflation remains low to nonexistent in most places, which hurts commodity prices along with companies in the energy and materials sectors. The widespread belief that inflation will stay low is keeping long-term bond yields low, which reduces the net interest margin for lenders, particularly banks. Hence, we see underperformance in financial services stocks, too. Further complicating the energy story is the continued expansion of unconventional shale oil production in the United States. Eventually the technology will spread to the rest of the world. Countries that depend on high oil prices are hurting. (And not just Saudi Arabia and Russia but a whole host of Middle Eastern countries).

The conditions that will change this pattern aren’t complicated: higher inflation expectations and rising long-term bond yields. That combination would push energy and metals prices up and steepen the yield curve. But the problem there is that the Federal Reserve remains intent on raising short-term rates. If they tighten another notch next week, as everyone expects, the current trends seem likely to continue. Here’s Louis’s conclusion:

In sum, it is hard to foresee what will disturb the current Goldilocks scenario. So, investors who liken themselves to Rugby forwards (aka “piggies”) [an actual rugby term that is a double-play pun on investors getting greedy and hungry – JM] will want to continue dining at the trough of the current bull market. Meanwhile, investors who like to get their hair blow-dried before games (backs, or princesses), and prefer to run where the ball is going to be rather than where it is, may want to look at reducing their underweights in financials. After all, at current global fixed income valuations, it wouldn’t take much – central bank hawkishness, upside surprises to core CPI – to trigger a mild fixed income sell-off. And any steepening of the yield curve would lead to a very different investment environment.

The shape of the yield curve is clearly critical in assessing markets right now. I agree with Louis that any steepening would lead to big changes. I wonder if we might get a steepening the other way: An inverted yield curve – when short-term rates are higher than long-term rates – is a classic recession indicator. It’s something the US hasn’t seen lately but can’t avoid forever.

How can we get an inverted yield curve with short-term rates so low? The Federal Reserve just slowly and surely raises rates; the weight of debt begins to slow economic growth even more; and long-term rates drop. Voilà, inverted yield curve. That is at least classically what is supposed to happen. So let’s think about that for a few paragraphs.

The other much-anticipated news from next week’s FOMC meeting is how/when the Fed intends to start reducing the massive bond portfolio it accumulated during the QE years. The initial move may be simply to stop reinvesting the proceeds when bonds mature. That is still billions of dollars each month – enough for even the very deep Treasury bond market to notice. (Then again, maybe they just let their mortgage bonds roll off and keep buying the Treasuries. They have so many options, and they haven’t bothered to tell us which ones they are seriously considering.)

A little-discussed aspect of this situation is, who will buy the Treasury bonds once the Fed backs out? That part is beyond the Fed’s control. The federal government won’t stop borrowing just because the Fed stops “lending.” The Treasury will have to find other buyers for its paper and will likely pay higher rates to attract them. Maybe. That is what is supposed to happen. In a world where the unthinkable keeps happening, we’ll just have to wait and see.

Brevan Howard’s chief US economist, my friend Jason Cummins (a past SIC speaker, I should note) wrote a fascinating guest column in the Financial Times on this topic. He points out something quite obvious that hasn’t occurred to many. The Treasury Department must borrow enough cash to pay the government’s bills, but it has huge discretion as to how it structures federal debt.

That means Treasury Secretary Steve Mnuchin can choose to replace the Fed’s purchases by issuing new debt at any point on the yield curve. It doesn’t have to be of the same term as the maturing paper it replaces. He can issue thirty-year bonds, three-month bills, or anything in between, in whatever combinations he thinks best.

The implication, as Jason gently explains, is that Steve Mnuchin can essentially rebuild the yield curve into whatever shape he wishes – presuming he can find buyers. He always will, of course, at some price.

The Treasury is such a massive borrower that its entry at any given maturity level can crowd out other borrowers and force rates higher. I am sure the Treasury people who manage this process try to reduce interest expense as much as possible, but they can only do so much. The government has bills to pay.

If Mnuchin decides to concentrate new borrowing at the long end, it will drive up those yields and steepen the yield curve. That’s exactly what banks would like to see. That would enhance their profit margins – but with the possible outcome of raising mortgage and other long-term rates. Not good for the housing sector.

Or, Mnuchin could do more borrowing at the short-term end. That would be a bit of a gamble because there’s no way to know what rates will be when the debt matures in the relatively near future. The strategy would also flatten and possibly even invert the yield curve.

Just to make all this more suspenseful, the government is also bumping up against its statutory debt ceiling. Congress might have to approve an increase as soon as August, and some in the House want to use the opportunity to exact spending cuts. The odds are low, but we can’t rule out the possibility of another government shutdown scenario, as we saw in 2011 and 2013.

As Cummins noted, “As the clock ticks down and investors get increasingly skittish, the last thing the Treasury needs is to have to find more private sector buyers of its debt.” Agreed. That is why I expect the Fed to delay implementing its balance sheet reductions until after the debt ceiling is raised – or maybe longer, if employment growth and/or inflation weaken over the summer and fall.

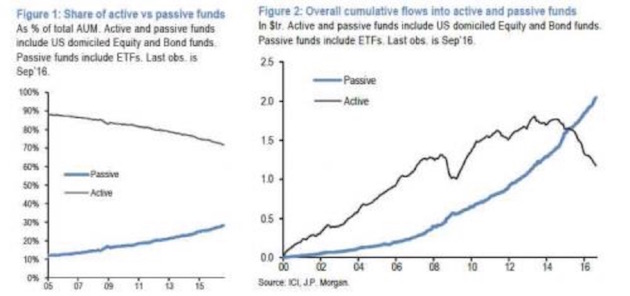

The Dangers of Passive Investing

Before we end, I want to come back to a few charts that illustrate some of the problems that are building up in the passive index world. It is not just ETFs, but also index mutual funds and the enormous amount of pension and insurance funds, along with many trust funds, that are passively invested directly in stocks. They simply duplicate indexes.

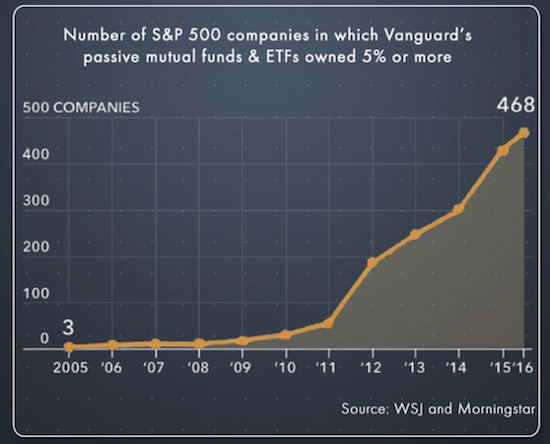

First, let’s note that Vanguard now owns more than 5% of 468 stocks in the S&P 500. That’s one fund company.

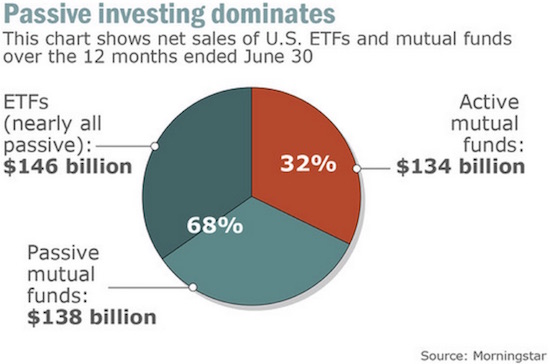

Here’s the picture for fund flows last year:

The number of hedge funds is at its lowest level since 2000. Passive funds are eating away at the assets under management by active funds:

This trend goes back to a point I made a few weeks ago but that needs to be repeated again and again. When the market obscures distinctions between good stocks and bad stocks because it buys all of them at the same time, there is no way for an active manager to take advantage of his skill in determining value. That ability to look at a company’s balance sheet and determine something close to true value is what gives active managers their edge. If you don’t have the chance to do this, you cannot add any alpha, and you are going to underperform the simple passive indexes – even though you charge higher fees. Money will leave you for the seemingly more plentiful pastures of passive indexing. One day you will be vindicated, and the money will come back (think Jeremy Grantham); but because investors will lose a great deal of their money in a bear market, you won’t get as much back in the short term as left you over the past few years. If you are an active manager, this just sucks.

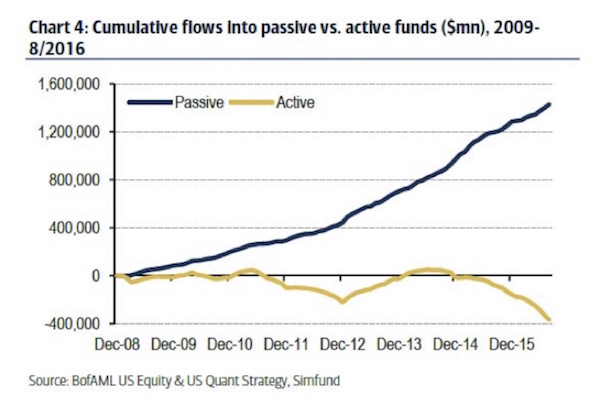

The next two charts show the difference between active and passive investing in the retail fund space. It’s a huge contrast:

The chart below traces the widening imbalance since 2008.

As I stated above, this imbalance will eventually be corrected. But the correction will not be pretty, though it may be swift.

If I’m going to keep my pledge to be shorter, more thoughtful, and faster, then I’d better close on that note.

Getting Married on St. Thomas, Omaha, San Francisco, and Freedom Fest in Las Vegas

Shane and I will be leaving for St. Thomas on 24 June, and we will be married on some beautiful beach on June 26, her birthday. Then I actually intend to relax for a week, enjoying time with my new bride and reading books with no redeeming social value (also known as science fiction/fantasy). I will begin final writing on my new book when I come back. I am finally really ready to attack the topic of what the world will look like in 20 years.

I have a quick trip to Omaha in the middle of June, then I’ll head directly on to San Francisco and Palo Alto for speaking engagements, come home to Dallas, recover for a few days, and then leave with Shane to go to Las Vegas for the Freedom Fest. It has become one of the largest libertarian gatherings, and I have so many good friends who go that it’s really a lot of fun for me. And while I am not much of a gambler (as in I suck at it and hate losing money to people who are much richer that I am), I really do like the shows. And dinners with friends.

That covers July, and August is, of course, the annual Maine fishing trip, but right now the rest of August looks to be pretty wide open. If I can figure it out, I may go somewhere that has a much cooler climate than Texas does in August and relax and write.

I will be cooking a chili dinner along with some prime this week for a dozen or so investment advisors who will be coming to Dallas to learn about my new Mauldin Solutions Smart Core investment program. For those of you have not yet gone to www.mauldinsolutions.com and given me a little bit of information about you, we have a white paper we would like to send to you, and there is other information on the website that will give you an idea as to how I think core portfolios should be structured in today’s world. Whether you are an individual or a professional or an institution, the principles are the same.

And with that I will hit the send button. You have a great week.

Your not going passively into the next bear market analyst,

John Mauldin

subscribers@MauldinEconomics.com

Copyright 2017 John Mauldin. All Rights Reserved.

|

Get a Bird’s-Eye View of the Economy with |

|

Share this letter using the buttons below |

|

Share Your Thoughts on This Article![]()

http://www.mauldineconomics.com/members

Thoughts From the Frontline is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com.

Any full reproduction of Thoughts from the Frontline is prohibited without express written permission. If you would like to quote brief portions only, please reference www.MauldinEconomics.com, keep all links within the portion being used fully active and intact, and include a link to www.mauldineconomics.com/important-disclosures. You can contact affiliates@mauldineconomics.com for more information about our content use policy.

http://www.mauldineconomics.com/subscribe

Thoughts From the Frontline and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin’s other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President and registered representative of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available, President and registered representative of Mauldin Securities, LLC, (MS) member FINRAand SIPC, through which securities may be o ffered. MWS is also a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB) and NFA Member. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee.

Note: Joining The Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Mauldin Securities. It is intended solely for investors who have registered with Mauldin Securities and its partners at www.MauldinCircle.com(formerly AccreditedInvestor.ws) or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Mauldin Solutions, LLC, a registered investment adviser with the US Securities & Exchange Commission and states unless an exemption is available. John Mauldin is a registered representative of Mauldin Securities, LLC, (MS), an FINRA registered broker-deale r. Mauldin Securities cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with w hich they have been able to negotiate fee arrangements.

PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account manager s have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273.

There are several key factors that have contributed to the financial fragility of the masses and our economy today. First, is that over the past 30 years, globalization and technology have helped to reduce the number of middle-class jobs available domestically. Fewer jobs and superfluous workers have led to stagnating incomes for most. At the same time, living expenses for critical services that are domestically-produced like education, medical services, child-care, housing and fresh food have all strongly outpaced income gains.

Today a middle-class lifestyle in America (ie., comfortable housing, transportation, food, health care and one family vacation a year), is estimated to require about 130k of annual household income for a family of 4. The median US household income, however–at 50k a year–is less than half the funds needed. In Canada, estimates of ‘middle class’ expenses vary in the range of 50-100k a year (see: Just who are middle-class).According to the latest 2014 StatsCan census, the median Canadian household income was $78,870.

Today a middle-class lifestyle in America (ie., comfortable housing, transportation, food, health care and one family vacation a year), is estimated to require about 130k of annual household income for a family of 4. The median US household income, however–at 50k a year–is less than half the funds needed. In Canada, estimates of ‘middle class’ expenses vary in the range of 50-100k a year (see: Just who are middle-class).According to the latest 2014 StatsCan census, the median Canadian household income was $78,870.

To plug spending deficits over the past 3 decades, families have increasingly added debt. American households now owe a record $12.7 trillion and Canadians $2 trillion, as of Q1 2017. Not only does servicing this debt further diminish disposable cash flow, but it also keeps people from building up net savings from their income.

Not surprisingly then, most households have insufficient retirement savings and about half say that they have no emergency savings to draw on and would have trouble coming up with $2k if needed within the next 30 days.

This leads to the last key contributor in this problem. Being over-indebted, under-saved and cash flow-deficient renders the masses vulnerable to a financial industry that has queered rules and policies in its favor while extracting hundreds of billions for itself –selling debt, transactions and products (under the guise of ‘advice’)–to an increasingly desperate and largely financially illiterate public.

Hear Beware the Overzealous Advisor

In the end, individuals play a leading role in their own poor financial outcomes. Often going with impossible ‘have your cake and eat it too’ promises and products, rather than math-based, rational plans and personal discipline.

One of the first steps to better outcomes is to openly admit financial facts in a world of facades. As hard as it may seem, doing otherwise is self-destructive, often repeatedly.

As Neal Gabler points out in this recent PBS segment: “Financial illiterates pay a heavy price for their illiteracy.”

Check out Are We in for Below-Average Returns Over the Next Decade?

Could you come up with $2,000 in 30 days if you had to? As many as 40 percent of American families can’t, despite the improving economy. Among them is Neal Gabler, who is frequently broke despite his successful career as a writer. As part of a collaboration between The Atlantic and the PBS NewsHour, Judy Woodruff looks at why Gabler and so many other Americans are struggling with savings. Here is a direct video link.

Mike Gleason: It is my privilege now to welcome in Dr. Chris of PeakProsperity.com, and author of the book Prosper! How to Prepare for the Future and Create a World Worth Inheriting. Chris is a commentator on a range of important topics such as global politicals, financial markets, governmental policy, precious metals and the importance of preparedness among other things. And it’s always great to have him with us.

Mike Gleason: It is my privilege now to welcome in Dr. Chris of PeakProsperity.com, and author of the book Prosper! How to Prepare for the Future and Create a World Worth Inheriting. Chris is a commentator on a range of important topics such as global politicals, financial markets, governmental policy, precious metals and the importance of preparedness among other things. And it’s always great to have him with us.

Chris, welcome back and thanks so much for joining us again.

Chris Martenson: Thank you. It’s a real pleasure to be with you today, Mike, and all of your listeners.

Mike Gleason: Well, since this is actually the first time we’ve had you on in 2017, Chris, to get started here I’d like to have you set the stage for us because many of us continued to be confused and bewildered by the resilience of these markets. So, first off, give us your thoughts on the first 130 days or so of Trump’s presidency, and then how is it that the U.S. equities market continues to soar to new heights despite what appears to be massive overvaluation? Basically, assess for us what’s going on in the political and financial markets here during the first half of the year as we start off.

Chris Martenson: All right. Well, I love how you set that up, because they’re actually coincident in my mind. The first four months of 2017, we saw something that has never been seen in world history, and that was central banks across the globe creating a trillion dollars of new hot money. So, if you want to know anything I think about the markets, we have to start with 250 billion thin air hot money base currency units being created and tossed into the financial systems. That really is a large explanation factor. And of course, there was this idea that Trump was coming in and that this could put some sort of a fresh air, a theme here, but let’s be clear.

Trump was a surprise victory there, and at about 2:30 in the morning (on election night) with the Dow down 800 points, it rallied and got back to green by open, and no question in my mind, but that was official action, the Plunge Protection Team or somebody like that, and so I think that’s the world we’re in now, really. That’s my setup. The macro setup is the authorities are dumping huge amounts of money into markets to get them to go higher. They’re also making sure that markets can’t go down at any point. They do what they can. My view is they’ll do that until they can’t, and then it will break and it’d be very surprising for a lot of people.

Mike Gleason: Expanding the point here, Chris, lately we have been addressing the exhaustion that some bullion investors are feeling. They have spent the past decade watching as the growth in government data’s accelerated, something you’ve been following and documenting for years, all the way back to your amazing Crash Course presentation, which really opened my eyes when I first consumed that amazing material. The Fed and other central banks have abandoned all restraint, zero interest rates, monetizing treasury bonds, and mortgage securities, and other exotic programs. The federal government has been running massive deficits for even longer, for half a century at least, but none of this, to this point anyway, has seemed to matter.

The U.S. dollar appears to be holding up, the bond vigilantes have never shown up, stock prices are making all-time highs and no one on Wall Street seems to be interested in buying safe haven assets. Now, the upcoming webinar that you’re going to be doing here very soon, and we’ll get into those details later in the podcast, is titled, “The End of Money” and you will be making the case that these fundamentals do in fact matter. Talk for a minute about what you see developing and why you think safe haven investors just need to stay the course despite what appears to be a punishing environment.

Chris Martenson: Well, I’d love to. You have to have a macro view at a time like this. There’s no other way to explain, when you’re in the middle of the largest money printing experiment, and I use that word carefully, in all of human history. To try and think that what guided us in the past is going to be useful during the most extraordinary money printing of all time is, I think, misguided. What do we do with that? Well, I think we have to understand how much is being printed, what that actually means, what it really tells us about what the Fed is thinking, how scared they are. Listen, you’ve got your chips on one side of the table than the other.

Either they know exactly what they’re doing and they’ve got this all under control, or they really don’t. If you have all your chips on the “they’ve got this covered” side, I think it’s a bad debt at this stage. So that’s why we’re having this webinar, is to talk with people who have pretty good insights into who the Fed is, how they were founded, how they were organized, what they’re thinking currently, and really that means we’re in that speculative mode still. Because were trying to figure out, Mike, what’s the Fed going to do? It’s not very fundamental, but we do know that fundamentally, when we back up even further, there always has to be a balance between the money you create and the stuff you buy with it. In this story, the money we create is both currency and it’s debt.

They both operate like money, like if I take out a student loan for $50,000 and spend that money, that $50,000 that went out because of credit expansion. When we look at this story, the world has had the fastest period of credit expansion in the last eight years or so that it’s ever had. It has this extraordinary base money creation, largest in all of history by far. It’s driven up financial assets like stocks and bonds to ridiculous heights. Quite mysteriously, left commodities pretty much completely off of that particular run since 2011 and QE3. So, when we put all of that in one spot, all I see is that the claims no real wealth are increasing, and that’s both the debt and the currency.

With both of these increasing as fast as they are, I know there has to be a correction at some point, and things have gotten really extreme lately, all across the globe but particularly in equity markets, places like that. What can you do? This is a crazy bubble time, you have to sit back and watch, you have to understand where it comes from. In The Crash Course, I make the case, Mike, that we’re not dealing with the after effects of a housing bubble that burst in 2007. We’ve been growing our credit at twice the rate of our income in this story, so total credit market debt compared to GDP. The debt’s been growing twice as fast as our income in this story for 45 years. That’s what broke in 2008, and it hasn’t been able to be fixed because it’s just a dumb model.

“Hey, we’re going to grow our expenses and our expenditures at twice the rate of our income.” You know, you can’t do that as a person, so you can’t do it as a nation. That’s what we’ve been doing and that’s what I think has just gotten to extraordinary levels right here, with what the central banks are now trying to just keep this going a little longer. And we don’t have a lot of history to guide us here. We have seen currencies collapse in the past, we’ve seen economies really struggle. You see that in Venezuela, but there’s really nowhere to escape this one, truthfully, because the whole world is involved in this at this point. It’s not like you’re in Austria in 1918 and you could duck over the border and be in a safe country.

Where would you go, given that it’s really the dollar, the Yen, the Euro have all been principally on this train? China caught up really fast in this story. Where would you go? With that, I don’t have any great answers besides people need to understand the context and then begin to build resilience in their portfolio, financial resilience, but other forms of resilience around social capital, emotional capital, all of the other things that we talk about in Prosper!, because I personally don’t see a way to get out of this without experiencing a lot of pain, economically.

Mike Gleason: We certainly are in uncharted waters. Now, the Fed has had a bit lower profile since the November elections. Trump has decided to stick with Janet Yellen, at least for the time being, and the constant political drama in Washington seems to be dominating even when it comes to investing news. Frankly, the constant obsession over what the FOMC might do at their next meeting had become tedious beyond words, so we’ve been glad for the respite. However, there will be plenty of attention on this month’s meeting, where officials are expected to hike rates again.

Do you agree with the consensus that two to three more rate hikes are coming in 2017? If they keep hiking, it seems The Fed will eventually wind up at odds with Trump who would almost certainly like to avoid holding the bag during the next big economic slowdown. So, what are your thoughts about the Fed during Trump’s administration here, Chris, both in the short run and in the longer term?

Chris Martenson: Well, the Fed is really just running its own script at this point in time. It’s pretty independent of who’s in the White House, and Trump can try and lean on them a little bit, but he won’t lean on them in the way that you or I might think he should, which is to tighten things up would probably be a wise course of action. But something that I’ve written about and I’ve even produced a short video on recently, is that this dynamic you’re talking about of tightening is not actually happening in this cycle. Because in 2008, Congress gave the Federal Reserve the right to pay interest on excess reserves that are held by depository institutions at the Fed.

So, the Fed prints money and of course that creates lots of excess reserves in the banking system, then the banks put that back at the Fed, and the Fed pays interest on that. The last three hikes that we’ve seen, going from basically a range of between zero and a quarter percent, on up to the current 1% in quarter increments, what we saw is that each one of those moments on the same day that the Fed allegedly hiked interest rates, they also increased the amount they were going to pay on excess reserves. So, now the banks have a choice. Am I going to keep money risk-free at the Fed or am I going to lend it to bank B overnight? Of course, they increasingly just chose to take the safe, sure money from the Fed, and so this is what’s different about this particular story, is that now when the Fed raises rates, not only does it not remove money from the system, but it’s actually adding more money to the bank system because it pays interest.

Two trillion dollars held at the Federal Reserve right now will generate at current rates, 20 billion dollars of interest income to the big banks on a yearly basis. That’s adding money, that’s not subtracting. So, it’s totally different.

Mike Gleason: Now, you recently wrote a fascinating piece on your Peak Prosperity site about how the Fed, in your view, is destroying America. You’ve alluded to some of those reasons but talk about this, Chris. Why do you believe this to be the case?

Chris Martenson: Because what they’re doing, it’s not just printing money, but they’re social engineering. They have to pick winners and losers. I know it sounds like the Fed prints money and does these crazy sophisticated things, or buys treasury at an auction, or does a reverse repo, and all these fancy names, but really all they’re doing is they’re printing money and they’re handing it out to the market and taking pieces of debt in return for that. So, when you really look at that dynamic, the Fed has been the engineer of the largest wealth gap that we’ve ever seen in all of our history at this point in time. It’s engineered one of the most, if not soon to be the most punishing income gaps.

It’s also purposely driven up the prices of houses which if you think about it, isn’t actually good for anybody except the very few people who sell and downsize, and capture that gain. It’s not good for first time home buyers, it’s not good for existing home owners who have to pay higher property taxes and insurance bills and things like that. But the Fed drove this up and created huge income disparities and really drove up the actual true cost of inflation in all the areas, metropolitan areas particularly, where these new private equity firms like Blackstone came in and just scooped up lots of properties. So, when you look at all of this, what is The Fed really doing?

Well, they’ve locked out the millennial generation pretty handedly. They’ve enabled the federal government to go forward with even more aggressive indebtedness, in taking on more debt. They’ve really encouraged, if not almost forced corporations to engage in financial engineering, because hey, if you’re a CFO, you can borrow 1% and retire dividend yield in stock at 2%, do that all day long. Makes total sense, but companies have been doing financial engineering, not productivity engineering. So, all of these things you can lay at the feet of the Fed, and listen, if they wanted to run six months, maybe 12 months of emergency interest rate cuts, back in 2008, early in 2009, I would have said okay.

But how long are we into this now, right? Depending on how you count it, we’re at least eight years into this thing, maybe nine, and that’s a pretty long emergency don’t you think? And all that’s happening during this emergency is we’re watching those things I just described, just get wider and wider, and wider. More financialization, less investment. Harder starts for students and millennials and other young people coming in, not easier. Really low business formations, because a trillion dollars of interest income didn’t go to people who are the traditional savers, the moms, the pops, the dads, grandmas, who then take their interest income, that trillion missing dollars and use that to help their sons and daughters and granddaughters and grandsons start businesses.

So, we’re seeing all of these effects, and of course, just the big mystery is that really it’s not talked about all that much yet, but it should be.

Mike Gleason: In terms of the metals, Chris, it’s been a decent but unspectacular year, despite what appears to be the ongoing price manipulation schemes of these bullion banks. What are your thoughts on the gold and silver markets?

Chris Martenson: Well, I’m just going to deviate slightly into the Bitcoin market, and noticed today, I think it’s around $2,300 or so. It’s been gyrating a bit, and I know it was higher recently, but just watching how those prices are actually behaving, that to me looks something like a free and fair market, right? You can actually watch and make sense of the movements in those markets. As you and your listeners really well know, that once the leverage paper market gets wrapped around any market, it’s now open to the players who want to control those markets to do what they will.

So, in my mind, really important article for everybody to read, two weeks ago roughly in the Wall Street Journal, we had that article about how the quants, all these people who have the math skills who can come in and write the algorithms that now run Wall Street. Those algorithms have access to huge amounts of capital, most of them are really trading at millisecond, maybe microsecond speeds, and they’re running around doing things in various markets, including the precious metals markets. I think those have been under basically the direct control of the bullion banks for quite a while, and it’s been their own personal piggy bank, if you will. And hey, that all makes sense, right? But as you know and as I know, those gains can’t go on forever, and at this point, I think gold and silver have found what feels to me like a base here, hopefully.

I have a strong sense that when this next financial crisis or paralysis comes along, that people are going to want safe haven assets at that point, and the safer the better. That’s because I think there’s institutional risk, possibly even sovereign risk. Things could really get hammered. Once you understand how extraordinary the leverage is in the system, and where the debts are distributed, and who is, who what, it really doesn’t add up well. So, if that gets called into question, guess what? Having precious metals is going to be a really important thing to do, and as we’ve discussed before, you’re going to either have them before that moment comes, or you probably won’t have them after. That would be my guess, seeing how quickly those markets can dry up.

Mike Gleason: Your website Peak Prosperity focuses on preparedness and self-reliant living. You can find communities there with interests ranging from investing to living off the grid. Are there any particular topics that members there are focused on at the moment? What are people interested in these days? We assume it isn’t all Washington D.C. politics all the time, so what are people in your sphere concentrating on these days, Chris?

Chris Martenson: Oh, good question, but we’ve been talking about a variety of things, all across the spectrum, really. At this particular juncture, we’re not spending nearly as much time on politics as you might think. What we’re pretty interested in is where the market’s going, what’s really happening across certain geopolitical areas, not U.S. politics, and interestingly, a third and growing area on our website is talking about how would you simply be in this world today?

Like, how we conduct ourselves, how are we living into the stories that unfolds, because these are brand new times. Increasingly, Mike, I’m running into people who get it. They’re like, “Ah, something is off in this story. We know it.” Some people understand it, some just feel it, it doesn’t matter. That’s really what a lot of us are talking about at Peak Prosperity now, is how do we stay focused? How do we stay in the game? How do live in a way so that we’re really enjoying ourselves today? But we’re also prepared for tomorrow, and so increasingly, I think it makes sense. This has been a fairly long, slow, topping process that we’re in right now, and I think there’s a sense here that we don’t know how much this can continue, right? It’s just tiring to be on alert all the time. What we’re talking about is how not to be on alert all the time, yet be prepared at the same time, if that makes any sense.

Mike Gleason: Well, as we begin to wrap up here, and before we get into some more of those details on your upcoming webinar, give us your thoughts on this period of calm before the storm that we appear to be in right now. Many were calling for a tumultuous year in 2017, coming off of the chaotic year we had in 2016, with Brexit and the crazy U.S. election and so forth, but to this point it hasn’t really materialized. What is it going to be that throws us off course, derails this historic rise in equities, and changes the economic landscape and then ultimately gets precious metals back into the consciousness of the investing public, Chris?

Chris Martenson: Well Mike, a lot of things could do it, of course, but what will do it is hard to say. This is a complex system. After the fact, people will point back and say, “Oh, it was when the German Finance Minister said that” or something, right? We’ll try and identify, but we have giant bubbles at this point in time. Nobody knows when bubbles are going to burst, and they always do it in a surprising way. It’s part of their definition. I’ve been thinking that this can’t go on much longer for a while, and it has, so I’m adjusting accordingly, and understanding, “Yeah, they’ve really got a pretty good sense of control on the system, but look how much it cost us?” Again, rewind. I think the most important information people can have is a trillion dollars had to be put into the system to basically hold everything elevated.

Slight gains, but really honestly, mostly just bumping along. That’s a really astonishing situation. I like to follow what the central bankers are doing, not what they’re saying. They’re saying everything’s great, but they’re doing emergency measures in the highest amounts ever. So, given all of that, I think it just makes a lot of sense for individuals to take action based on that, to make themselves prepared, make themselves more resilient, and there’s lots of things people can do. By the way, almost all of these things that we would recommend, if not all of them, are going to make your life better today. People will not look back on getting ready in the way we suggest, and say, “Gosh, I shouldn’t have got in shape. I probably shouldn’t have saved so much money. It’s too bad I have this functioning house.”

Nobody’s going to say that. So, I think this calm before the storm is the time that we use as the gift that it is. It’s still very easy, relatively speaking, to take whatever steps you want to take, and becoming prepared while things are really unraveling is a bad strategy. It’s hard to be efficient, it’s hard to be calm, it’s hard to be rational if you’re in the middle of all that when it happens. That’s been our advice, it’s been our advice for a while. Hasn’t really changed and I honestly, I don’t know how much longer this can go on. It’s surprised me every month of the way so far.

Mike Gleason: Yeah, you’ve got to fight that complacent, and then also like you mentioned, when things are unraveling, that’s not when you want to be just now starting to think about what you’re going to do in those situations.

Well Chris, thanks so much for your time and your wonderful insights. Now, we’ve touched on it a bit already, but talk about this upcoming webinar. When it is, who’s involved, and then share a little bit more about what you’ll be discussing, and then of course how people can registered for that, because it will undoubtedly be very worthwhile and informative. Give us the info there, if you would.

Chris Martenson: Sure. So, the structure is it’s a webinar, it’s about two and a half hours long. We have three special guests on there. Each one of those guests is going to speak for a period of time, and also there will be an opportunity for live Q&A for the participants who’ve registered for this webinar. The cost is $50 and the three guests we have are G. Edward Griffin, he wrote the book on the Federal Reserve, so he’s the author of The Creature from Jekyll Island, which I’m sure many of your listeners have read. We’ve got David Stockman, former head of the Office of Management and Budget under Reagan. Was a U.S. representative and a pretty frequent commentator on the macro conditions in the markets. He’s going to be helping us understand those conditions. Also, what’s happening in Washington D.C. because the politics here are probably going to shape Fed policy as they have for a while. Will the Trump tax cuts go through? What’s the infrastructure plan looking like? We’re counting on David for that.

And then, Axel Merk he’s the person who knows more Federal Reserve officials than anyone else I know. Both current and former, he just came back from a whole two or three day event where I think there were 20 Fed officials at, so he got to talk with them, and read the tealeaves and read the body language, so hopefully he’ll be given us some insights into what comes next.

Again, so this is on June 7th, it’s at noon, and it’s going to be a live webinar. So people who signed up for that also will be able to download and watch that later.

Mike Gleason: We’ve got a link to the webinar registration page from this podcast page on our site, and we urge people to sign up for that. It’s a truly great lineup of participants and it should be fantastic.

Well, excellent stuff as always, Chris. It’s been great to talk with you again and thanks for being so generous with your time today. Much success with the upcoming webinar, continued success with the book, and I hope you enjoy your summer, and I look forward to catching up with you later this year. Thanks very much, Chris.

Chris Martenson: Thank you so much.

Mike Gleason: Well, that will do it for this week. Thanks again to Dr. Chris Martenson of PeakProsperity.com and co-author of the book Prosper! How To Prepare for the Future and Create a World Worth Inheriting. Check out the site for information on that, as well as next week’s webinar on the “End of Money,” which is June 7th at 12 noon, Eastern Time. Just go to PeakProsperity.com/webinar for more information.

Mike Gleason is a Director with Money Metals Exchange, a national precious metals dealer with over 50,000 customers. Gleason is a hard money advocate and a strong proponent of personal liberty, limited government and the Austrian School of Economics. A graduate of the University of Florida, Gleason has extensive experience in management, sales and logistics as well as precious metals investing. He also puts his longtime broadcasting background to good use, hosting a weekly precious metals podcast since 2011, a program listened to by tens of thousands each week.

When the Central Banks finally lose control of propping up the markets, will the BIG MONEY be made in owning gold, silver or crypto-currencies? This is the question many investors who are focused on “alternative assets”, outside the typical mainstream stock, bond and real estate markets, are asking.

Most investors who have been concerned about the massively inflated Bubble Markets and the Greatest Financial Ponzi Scheme in history, have been investing in gold and silver. However, a new kid on the block, called Bitcoin and the other crypto-currencies, have gained a lot of attention due to the huge increase in their prices over the past few months.

So, now many investors are wondering what to make of these extremely volatile crypto-currencies and if they are nothing more than purely speculative and gambling vehicles. This is a logical assumption based on the massive spike in many of their crypto-currency values.

That being said, Charles Hugh Smith wrote the following in his article, Projecting The Price Of Bitcoin:

The wild card in cryptocurrencies is the role of Big Institutional Money.

I’ve taken the liberty of preparing a projection of bitcoin’s price action going forward:

You see the primary dynamic is continued skepticism from the mainstream, which owns essentially no cryptocurrency and conventionally views bitcoin and its peers as fads, scams and bubbles that will soon pop as price crashes back to near-zero.

Skepticism is always a wise default position to start one’s inquiry, but if no knowledge is being acquired, skepticism quickly morphs into stubborn ignorance.

Bitcoin et al. are not the equivalent of Beanie Babies.Cryptocurrencies have utility value. They facilitate international payments for goods and services.

This was very interesting analysis done by Charles Hugh Smith who is one of the more bright minds in the alternative media community. I have watched Bitcoin out of the corner of my eye over the past few years, but have not placed much attention on the leading crypto-currency. However, as the price of Bitcoin and crypto-currencies have surged over the past several months, I decided to take a closer look… to see what all the hubbub was about.

What I found out was quite interesting. Bitcoin’s price rise is not just based on mere speculative flows (as many assume), but rather it’s also rising due to the skyrocketing energy and capital costs to produce each coin. Yes, there is a lot more to this, but there is some METHOD TO THE MADNESS.

Charles Hugh Smith understands this and realizes that cyrpto-currencies will likely to continue to gain in price, interest and market cap going forward due to the way they were designed. Now, I am not saying I totally agree with Charles, but there is more behind crypto-currencies than just mere speculative flows into digital assets.

So, the question is…. where will the BIG MONEY be made when the Fed and Central Banks lose control of propping up the Markets? That’s a good question. Yes, the Central Banks will lose control because they are facing one force that they are unable to manipulate…. ENERGY.

While the Central banks can manipulate the oil price, than cannot manipulate the Falling EROI – Energy Returned On Investment that continues to decline. So, the more the EROI of oil falls, the more printing and propping up the markets the Central banks are forced to do. It is really that simple.

Thus, the END OF MARKET MANIPULATION has an expiration date…. and its not decades away. I wouldn’t be surprised that it takes place within the next 5-10 years… or even less.

To get an idea of the total current value of Gold, Silver and Bitcoin-Crypto-currencies, let’s take a look at the value of above ground gold and silver investment:

According to the data put out by the USGS – U.S. Geological Survey, GFMS, CPM Group and Kitco (market price), all the investment gold held in the world is worth $2.93 trillion versus $51.8 billion for silver. You will also notice that there isn’t much more above-ground investment silver in the world (2.59 billion oz) compared to gold (2.25 billion oz).

NOTE: The total global gold and silver value is based upon $1,300 for gold and $20 for silver

Now, if we bring in the total value of Bitcoin and all the other crypto-currencies, we have the following:

All the gold investment (including Central Bank and private investment) is approximately $2.93 trillion versus $89 billion for the total Bitcoin-Cryptos market cap and $52 billion for silver. So, the current market cap of Bitcoin-cryptos now surpasses the total global value of silver investment by $37 billion.

Of course, the Bitcoin-cyrpto market cap has increased significantly over the past few months. Common sense logic suggests the recent spike in Bitcoin and the other crypto-currencies will likely experience a large correction… thus a falling market cap. But, I agree with Charles Hugh Smith that these crypto-currencies will likely gain significantly over the next five years.

However, I also see the value of gold and silver rising considerably as well…. especially silver. The price of silver will likely increase in a much greater percentage because there isn’t much more physical silver in the world compared to gold, and its price is so low, that when large funds move into the silver market…. the huge pressure will be released by a much higher price.

There is a lot to understand about Gold, Silver and the Crypto-currencies going forward. Investors need to realize that while the crypto-currencies will likely see large gains in their values in the future, the BIG ENERGY PROBLEMS will are going to face may not be good for Cypto-currency network functionality. Again…. there is a lot of consider.

Which means… gold and silver will still be the some of the safest physical assets to own in the future.

Check back for new articles and updates at the SRSrocco Report.

Although frontier markets are a small subset of the emerging market universe, we think they represent an important constituency that offer some compelling potential opportunities. Here, I’ve invited my colleague Carlos Hardenberg, senior vice president and director of frontier markets strategies at Templeton Emerging Markets Group, to outline some of the opportunities he sees in these dynamic markets and debunk some of the urban myths.

Although frontier markets are a small subset of the emerging market universe, we think they represent an important constituency that offer some compelling potential opportunities. Here, I’ve invited my colleague Carlos Hardenberg, senior vice president and director of frontier markets strategies at Templeton Emerging Markets Group, to outline some of the opportunities he sees in these dynamic markets and debunk some of the urban myths.

There are a number of urban myths about frontier markets (the less-developed subset of the emerging-market universe). We think these myths may have caused investors to overlook them in favour of developed or traditional emerging-market alternatives.

We believe conditions are now ripe for a re-evaluation of this important niche. There are some very compelling reasons why many investors might want to take another look at frontier markets today. These can be summed up as the following, which I will delve into further.

- Expectations for robust economic growth

- Continued macro development

- Deep discounts in valuations

- Low correlations

Busting the Urban Myths

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair