Uncategorized

The 12 Golden Rules for Successful Trading

1. Adopt a definite trading plan.

Because of the emotional stress that is inherent in any speculative situation, you must have a predetermined method of operation, which includes a set of rules by which you operate and adhere to, thus protecting you from yourself. Very often, your emotions will tell you to do something totally foreign or negative to what your market trading plan should be. It is only by adhering to a preconceived formula that you can resist the emotional temptations and stresses that are constantly present in a speculative situation.

2. If you’re not sure, don’t trade.

If you’re in a trade and feel unsure of yourself, take your loss or protect your profit with a stop. If you are unsure of a position, you will be influenced by a multitude of extraneous and unimportant details and will probably end up taking a loss.

3. You should be able to be right 40% of the time and still show handsome profits.

In speculating, it would be folly to expect to be right every time. An individual with the proper trading techniques should be able to cut his losses short and let his profits run so that even being right less than half the time will show excellent profits. This point is re-emphasized in Rule Four.

4. Cut your losses and let your profits ride.

The basic failing of most speculators is that they put a limit on their profits and no limit on their losses. A man hates to admit he’s wrong. Therefore, an individual will often let his loss ride, becoming larger and larger in hopes that eventually the market will turn around and prove him correct. Then after a while, he begins hoping for a small loss and gives up hoping for a profit. Human nature also dictates that an individual wants to take his profit right away and thus prove himself correct. There is an old saying, “You never go broke taking a small profit.” But you’ll certainly never get rich that way. Being satisfied with small profits is the wrong mental approach for making money in speculation. If you are correct when entering a speculative situation, you will know it almost immediately and will show a profit quickly. However, if you are wrong, you will show a loss and you should remove yourself from the situation quickly. Taking a small loss does not necessarily mean you were wrong in your thinking. It simply means that your timing was perhaps incorrect and that you should wait for the correct timing and situation to allow you to reenter the market. Remember, in any speculative situation, the market is the final judge. An individual must let the market tell him when he is wrong and when he is right. If you show a profit, ride it until the market turns around and tells you that you are no longer right, and, at that time, you should get out…but not before! On the other hand, the market will also tell you if you are wrong and it would be a serious mistake to argue with what it is saying.

5. If you cannot afford to lose, you cannot afford to win.

As we have stated in Rule Four, losing is a natural part of trading. If you are not in a position to accept losses, either psychologically or financially, you have no business trading. In addition, trading should be done only with surplus funds that are not vital to daily expenses.

6. Don’t trade too many markets.

It is difficult to successfully trade and understand a specific market. It is next to impossible for an individual, especially a beginner, to be successful in several markets at the same time. The fundamental, technical, and psychological information necessary to trade successfully in more than a few markets is more than the individual has either the time or ability to accumulate.

7. Don’t trade in a market that is too thin.

A lack of public participation in a market will make it difficult, if not impossible, to liquidate a position at anywhere near the price you want.

8. Be aware of the trend. (“The Trend is your friend”)

It is vitally important that a trader be aware of a strong force in the market, either bullish or bearish. When this force is at its height, it would be folly to attempt to buck it. However, one must learn to recognize when a trend is about to run its course or is near a period of exhaustion. By an ability to recognize the early signs of exhaustion, the trader will protect himself from staying in the market too long and will be able to change direction when the trend changes.

9. Don’t attempt to buy the bottom or sell the top.

It simply can’t be done unless you have the aid of a crystal ball or some other tool which could be peculiar to the mystic. Be content to wait for the trend to develop and then take advantage of it once it has been established.

10. Never answer a margin call.

This rule acts as a stop loss when your position has weakened considerably. By dogmatically and arbitrarily adhering to this rule, you will be forced to get out of the market before disaster sets it. It is often difficult to admit you’re wrong and get out of the market (which you probably should have done well before you received a margin call). However, the presence of a margin call should act as a final warning that you have let your position go as far as you conceivably can (unless the initial margin is out of line with the volatility of the contract).

11. You can usually sell the first rally or buy the first break.

Generally, a market which has just established a trend either up or down will have a reaction and good interim profits can be made by recognizing this reaction and taking advantage of it. For example, in a bull market, the first reaction will generally be met by investors waiting to buy the break. This support generally causes the market to rally. The reverse is true of a bear market.

12. Never straddle a loss.

A loss by itself is difficult enough to accept. However, to lock in this loss, thus making it necessary for you to be right twice rather than the once (which you previously found impossible) is sheer absurdity.

While the following are not specific trading rules, they are general observations which will aid the speculator in formulating an understanding of markets:

You must retain control of the situation and yourself. Do not allow your position to control you. It is a mistake to find yourself in a position larger than you can reasonable handle. When this occurs, you will find that the sheer size of the position, rather than the facts of the situation itself, affects your judgment.

The commodity does not know that you own it. You must remain impersonal in your trading. When you take a position and you are wrong, remember it is better to get out immediately! The market will not feel badly about it if you do, but you will if you don’t.

The market always looks its worst at its bottom, and the best at the top. It is important to remember that before the market turns around, it is at its very worst. Therefore, be prepared to treat each day objectively by not allowing the emotional fever to carry over and cloud your judgment.

Equity…Equity…Equity…Not Cash. If a man is long from 100 points below the market and you are long from the opening that day, you both had the same amount invested in the market from the time both of you were long. Therefore, if the market goes up ten points, you each have made the same amount that day. If the market goes down 10 points, you have each lost the same amount. You should not be confused by the fact that someone has taken a position before you. You must be concerned with your own situation primarily. Each day, start fresh. Your paper profits or losses from previous days should not enter into your decisions regarding the course of action you will take.

Treat paper profits as if they are your own money. They are! Naturally, the opposite also holds true.

The 12 Golden Rules for Successful Trading

1. Adopt a definite trading plan.

Because of the emotional stress that is inherent in any speculative situation, you must have a predetermined method of operation, which includes a set of rules by which you operate and adhere to, thus protecting you from yourself. Very often, your emotions will tell you to do something totally foreign or negative to what your market trading plan should be. It is only by adhering to a preconceived formula that you can resist the emotional temptations and stresses that are constantly present in a speculative situation.

2. If you’re not sure, don’t trade.

If you’re in a trade and feel unsure of yourself, take your loss or protect your profit with a stop. If you are unsure of a position, you will be influenced by a multitude of extraneous and unimportant details and will probably end up taking a loss.

3. You should be able to be right 40% of the time and still show handsome profits.

In speculating, it would be folly to expect to be right every time. An individual with the proper trading techniques should be able to cut his losses short and let his profits run so that even being right less than half the time will show excellent profits. This point is re-emphasized in Rule Four.

4. Cut your losses and let your profits ride.

The basic failing of most speculators is that they put a limit on their profits and no limit on their losses. A man hates to admit he’s wrong. Therefore, an individual will often let his loss ride, becoming larger and larger in hopes that eventually the market will turn around and prove him correct. Then after a while, he begins hoping for a small loss and gives up hoping for a profit. Human nature also dictates that an individual wants to take his profit right away and thus prove himself correct. There is an old saying, “You never go broke taking a small profit.” But you’ll certainly never get rich that way. Being satisfied with small profits is the wrong mental approach for making money in speculation. If you are correct when entering a speculative situation, you will know it almost immediately and will show a profit quickly. However, if you are wrong, you will show a loss and you should remove yourself from the situation quickly. Taking a small loss does not necessarily mean you were wrong in your thinking. It simply means that your timing was perhaps incorrect and that you should wait for the correct timing and situation to allow you to reenter the market. Remember, in any speculative situation, the market is the final judge. An individual must let the market tell him when he is wrong and when he is right. If you show a profit, ride it until the market turns around and tells you that you are no longer right, and, at that time, you should get out…but not before! On the other hand, the market will also tell you if you are wrong and it would be a serious mistake to argue with what it is saying.

5. If you cannot afford to lose, you cannot afford to win.

As we have stated in Rule Four, losing is a natural part of trading. If you are not in a position to accept losses, either psychologically or financially, you have no business trading. In addition, trading should be done only with surplus funds that are not vital to daily expenses.

6. Don’t trade too many markets.

It is difficult to successfully trade and understand a specific market. It is next to impossible for an individual, especially a beginner, to be successful in several markets at the same time. The fundamental, technical, and psychological information necessary to trade successfully in more than a few markets is more than the individual has either the time or ability to accumulate.

7. Don’t trade in a market that is too thin.

A lack of public participation in a market will make it difficult, if not impossible, to liquidate a position at anywhere near the price you want.

8. Be aware of the trend. (“The Trend is your friend”)

It is vitally important that a trader be aware of a strong force in the market, either bullish or bearish. When this force is at its height, it would be folly to attempt to buck it. However, one must learn to recognize when a trend is about to run its course or is near a period of exhaustion. By an ability to recognize the early signs of exhaustion, the trader will protect himself from staying in the market too long and will be able to change direction when the trend changes.

9. Don’t attempt to buy the bottom or sell the top.

It simply can’t be done unless you have the aid of a crystal ball or some other tool which could be peculiar to the mystic. Be content to wait for the trend to develop and then take advantage of it once it has been established.

10. Never answer a margin call.

This rule acts as a stop loss when your position has weakened considerably. By dogmatically and arbitrarily adhering to this rule, you will be forced to get out of the market before disaster sets it. It is often difficult to admit you’re wrong and get out of the market (which you probably should have done well before you received a margin call). However, the presence of a margin call should act as a final warning that you have let your position go as far as you conceivably can (unless the initial margin is out of line with the volatility of the contract).

11. You can usually sell the first rally or buy the first break.

Generally, a market which has just established a trend either up or down will have a reaction and good interim profits can be made by recognizing this reaction and taking advantage of it. For example, in a bull market, the first reaction will generally be met by investors waiting to buy the break. This support generally causes the market to rally. The reverse is true of a bear market.

12. Never straddle a loss.

A loss by itself is difficult enough to accept. However, to lock in this loss, thus making it necessary for you to be right twice rather than the once (which you previously found impossible) is sheer absurdity.

While the following are not specific trading rules, they are general observations which will aid the speculator in formulating an understanding of markets:

You must retain control of the situation and yourself. Do not allow your position to control you. It is a mistake to find yourself in a position larger than you can reasonable handle. When this occurs, you will find that the sheer size of the position, rather than the facts of the situation itself, affects your judgment.

The commodity does not know that you own it. You must remain impersonal in your trading. When you take a position and you are wrong, remember it is better to get out immediately! The market will not feel badly about it if you do, but you will if you don’t.

The market always looks its worst at its bottom, and the best at the top. It is important to remember that before the market turns around, it is at its very worst. Therefore, be prepared to treat each day objectively by not allowing the emotional fever to carry over and cloud your judgment.

Equity…Equity…Equity…Not Cash. If a man is long from 100 points below the market and you are long from the opening that day, you both had the same amount invested in the market from the time both of you were long. Therefore, if the market goes up ten points, you each have made the same amount that day. If the market goes down 10 points, you have each lost the same amount. You should not be confused by the fact that someone has taken a position before you. You must be concerned with your own situation primarily. Each day, start fresh. Your paper profits or losses from previous days should not enter into your decisions regarding the course of action you will take.

Treat paper profits as if they are your own money. They are! Naturally, the opposite also holds true.

The frantic shouting and signaling of bids and offers on the trading floor of a futures exchange undeniably convey an impression of chaos. The reality however, is that chaos is what futures markets replaced. Prior to the establishment of central grain markets in the mid-nineteenth century, the nation farmers carted their newly harvested crops over plank roads to major population and transportation centers each fall in search of buyers. The seasonal glut drove prices to giveaway levels and, indeed, to throwaway levels as grain often rotted in the streets or was dumped in rivers and lakes for lack of storage. Come spring, shortages frequently developed and foods made from corn and wheat became barely affordable luxuries. Throughout the year, it was each buyer and seller for himself with neither a place nor a mechanism for organized, competitive bidding. The first central markets were formed to meet that need. Eventually, contracts were entered into for forward as well as for spot (immediate) delivery. So-called forwards were the forerunners of present day futures contracts.

Spurred by the need to manage price and interest rate risks that exist in virtually every type of modern business, today’s futures markets have also become major financial markets. Participants include mortgage bankers as well as farmers, bond dealers as well as grain merchants, and multinational corporations as well as food processors, savings and loan associations, and individual speculators.

Futures prices arrived at through competitive bidding are immediately and continuously relayed around the world by wire and satellite. A farmer in Nebraska, a merchant in Amsterdam, an importer in Tokyo and a speculator in Ohio thereby have simultaneous access to the latest market-derived price quotations. And, should they choose, they can establish a price level for future delivery–or for speculative purposes–simply by having their broker buy or sell the appropriate contracts. Images created by the fast-paced activity of the trading floor notwithstanding, regulated futures markets are a keystone of one of the world’s most orderly envied and intensely competitive marketing systems. Should you at some time decide to trade in futures contracts, either for speculation or in connection with a risk management strategy, your orders to buy or sell would be communicated by phone from the brokerage office you use and then to the trading pit or ring for execution by a floor broker. If you are a buyer, the broker will seek a seller at the lowest available price. If you are a seller, the broker will seek a buyer at the highest available price. That’s what the shouting and signaling is about.

In either case, the person who takes the opposite side of your trade may be or may represent someone who is a commercial hedger or perhaps someone who is a public speculator. Or, quite possibly, the other party may be an independent floor trader. In becoming acquainted with futures markets, it is useful to have at least a general understanding of who these various market participants are, what they are doing and why.

Hedgers

The details of hedging can be somewhat complex but the principle is simple. Hedgers are individuals and firms that make purchases and sales in the futures market solely for the purpose of establishing a known price level–weeks or months in advance–for something they later intend to buy or sell in the cash market (such as at a grain elevator or in the bond market). In this way they attempt to protect themselves against the risk of an unfavorable price change in the interim. Or hedgers may use futures to lock in an acceptable margin between their purchase cost and their selling price. Consider this example:

A jewelry manufacturer will need to buy additional gold from his supplier in six months. Between now and then, however, he fears the price of gold may increase. That could be a problem because he has already published his catalog for a year ahead.

To lock in the price level at which gold is presently being quoted for delivery in six months, he buys a futures contract at a price of, say, $350 an ounce.

If, six months later, the cash market price of gold has risen to $370, he will have to pay his supplier that amount to acquire gold. However, the extra $20 an ounce cost will be offset by a $20 an ounce profit when the futures contract bought at $350 is sold for $370. In effect, the hedge provided insurance against an increase in the price of gold. It locked in a net cost of $350, regardless of what happened to the cash market price of gold. Had the price of gold declined instead of risen, he would have incurred a loss on his futures position but this would have been offset by the lower cost of acquiring gold in the cash market.

The number and variety of hedging possibilities is practically limitless. A cattle feeder can hedge against a decline in livestock prices and a meat packer or supermarket chain can hedge against an increase in livestock prices. Borrowers can hedge against higher interest rates, and lenders against lower interest rates. Investors can hedge against an overall decline in stock prices, and those who anticipate having money to invest can hedge against an increase in the over-all level of stock prices. And the list goes on.

Whatever the hedging strategy, the common denominator is that hedgers willingly give up the opportunity to benefit from favorable price changes in order to achieve protection against unfavorable price changes.

Speculators

Were you to speculate in futures contracts, the person taking the opposite side of your trade on any given occasion could be a hedger or it might well be another speculator–someone whose opinion about the probable direction of prices differs from your own.

The arithmetic of speculation in futures contracts–including the opportunities it offers and the risks it involves–will be discussed in detail later on. For now, suffice it to say that speculators are individuals and firms who seek to profit from anticipated increases or decreases in futures prices. In so doing, they help provide the risk capital needed to facilitate hedging.

Someone who expects a futures price to increase would purchase futures contracts in the hope of later being able to sell them at a higher price. This is known as “going long.” Conversely, someone who expects a futures price to decline would sell futures contracts in the hope of later being able to buy back identical and offsetting contracts at a lower price. The practice of selling futures contracts in anticipation of lower prices is known as “going short.” One of the attractive features of futures trading is that it is equally easy to profit from declining prices (by selling) as it is to profit from rising prices (by buying).

Floor Traders

Persons known as floor traders or locals, who buy and sell for their own accounts on the trading floors of the exchanges, are the least known and understood of all futures market participants. Yet their role is an important one. Like specialists and market makers at securities exchanges, they help to provide market liquidity. If there isn’t a hedger or another speculator who is immediately willing to take the other side of your order at or near the going price, the chances are there will be an independent floor trader who will do so, in the hope of minutes or even seconds later being able to make an offsetting trade at a small profit. In the grain markets, for example, there is frequently only one-fourth of a cent a bushel difference between the prices at which a floor trader buys and sells.

Floor traders, of course, have no guarantee they will realize a profit. They may end up losing money on any given trade. Their presence, however, makes for more liquid and competitive markets. It should be pointed out, however, that unlike market makers or specialists, floor traders are not obligated to maintain a liquid market or to take the opposite side of customer orders.

What is a Futures Contract?

There are two types of futures contracts, those that provide for physical delivery of a particular commodity or item and those which call for a cash settlement. The month during which delivery or settlement is to occur is specified. Thus, a July futures contract is one providing for delivery or settlement in July.

It should be noted that even in the case of delivery-type futures contracts, very few actually result in delivery.* Not many speculators have the desire to take or make delivery of, say, 5,000 bushels of wheat, or 112,000 pounds of sugar, or a million dollars worth of U.S. Treasury bills for that matter. Rather, the vast majority of speculators in futures markets choose to realize their gains or losses by buying or selling offsetting futures contracts prior to the delivery date. Selling a contract that was previously purchased liquidates a futures position in exactly the same way, for example, that selling 100 shares of IBM stock liquidates an earlier purchase of 100 shares of IBM stock. Similarly, a futures contract that was initially sold can be liquidated by an offsetting purchase. In either case, gain or loss is the difference between the buying price and the selling price.

Even hedgers generally don’t make or take delivery. Most, like the jewelry manufacturer illustrated earlier, find it more convenient to liquidate their futures positions and (if they realize a gain) use the money to offset whatever adverse price change has occurred in the cash market.

* When delivery does occur it is in the form of a negotiable instrument (such as a warehouse receipt) that evidences the holder’s ownership of the commodity, at some designated location.

Delivery

Since delivery on futures contracts is the exception rather than the rule, why do most contracts even have a delivery provision? There are two reasons. One is that it offers buyers and sellers the opportunity to take or make delivery of the physical commodity if they so choose. More importantly, however, the fact that buyers and sellers can take or make delivery helps to assure that futures prices will accurately reflect the cash market value of the commodity at the time the contract expires–i.e., that futures and cash prices will eventually converge. It is convergence that makes hedging an effective way to obtain protection against an adverse change in the cash market price.*

* Convergence occurs at the expiration of the futures contract because any difference between the cash and futures prices would quickly be negated by profit-minded investors who would buy the commodity in the lowest-price market and sell it in the highest-price market until the price difference disappeared. This is known as arbitrage and is a form of trading generally best left to professionals in the cash and futures markets.

Cash settlement futures contracts are precisely that, contracts which are settled in cash rather than by delivery at the time the contract expires. Stock index futures contracts, for example, are settled in cash on the basis of the index number at the close of the final day of trading. There is no provision for delivery of the shares of stock that make up the various indexes. That would be impractical. With a cash settlement contract, convergence is automatic.

Margins

As is apparent from the preceding discussion, the arithmetic of leverage is the arithmetic of margins. An understanding of margins–and of the several different kinds of margin–is essential to an understanding of futures trading.

If your previous investment experience has mainly involved common stocks, you know that the term margin–as used in connection with securities–has to do with the cash down payment and money borrowed from a broker to purchase stocks. But used in connection with futures trading, margin has an altogether different meaning and serves an altogether different purpose.

Rather than providing a down payment, the margin required to buy or sell a futures contract is solely a deposit of good faith money that can be drawn on by your brokerage firm to cover losses that you may incur in the course of futures trading. It is much like money held in an escrow account. Minimum margin requirements for a particular futures contract at a particular time are set by the exchange on which the contract is traded. They are typically about five percent of the current value of the futures contract. Exchanges continuously monitor market conditions and risks and, as necessary, raise or reduce their margin requirements. Individual brokerage firms may require higher margin amounts from their customers than the exchange-set minimums.

There are two margin-related terms you should know: Initial margin and maintenance margin.

Initial margin (sometimes called original margin) is the sum of money that the customer must deposit with the brokerage firm for each futures contract to be bought or sold. On any day that profits accrue on your open positions, the profits will be added to the balance in your margin account. On any day losses accrue, the losses will be deducted from the balance in your margin account.

If and when the funds remaining available in your margin account are reduced by losses to below a certain level–known as the maintenance marginrequirement–your broker will require that you deposit additional funds to bring the account back to the level of the initial margin. Or, you may also be asked for additional margin if the exchange or your brokerage firm raises its margin requirements. Requests for additional margin are known as margin calls.

Assume, for example, that the initial margin needed to buy or sell a particular futures contract is $2,000 and that the maintenance margin requirement is $1,500. Should losses on open positions reduce the funds remaining in your trading account to, say, $1,400 (an amount less than the maintenance requirement), you will receive a margin call for the $600 needed to restore your account to $2,000.

Before trading in futures contracts, be sure you understand the brokerage firm’s Margin Agreement and know how and when the firm expects margin calls to be met. Some firms may require only that you mail a personal check. Others may insist you wire transfer funds from your bank or provide same-day or next-day delivery of a certified or cashier’s check. If margin calls are not met in the prescribed time and form, the firm can protect itself by liquidating your open positions at the available market price (possibly resulting in an unsecured loss for which you would be liable).

Spreads

While most speculative futures transactions involve a simple purchase of futures contracts to profit from an expected price increase–or an equally simple sale to profit from an expected price decrease–numerous other possible strategies exist. Spreads are one example. A spread, at least in its simplest form, involves buying one futures contract and selling another futures contract. The purpose is to profit from an expected change in the relationship between the purchase price of one and the selling price of the other. As an illustration, assume it’s now November, that the March wheat futures price is presently $3.10 a bushel and the May wheat futures price is presently $3.15 a bushel, a difference of 5 cents. Your analysis of market conditions indicates that, over the next few months, the price difference between the two contracts will widen to become greater than 5 cents. To profit if you are right, you could sell the March futures contract (the lower priced contract) and buy the May futures contract (the higher priced contract). Assume time and events prove you right and that, by February, the March futures price has risen to $3.20 and May futures price is $3.35, a difference of 15 cents. By liquidating both contracts at this time, you can realize a net gain of 10 cents a bushel. Since each contract is 5,000 bushels, the total gain is $500.

The Contract Unit

Delivery-type futures contracts stipulate the specifications of the commodity to be delivered (such as 5,000 bushels of grain, 40,000 pounds of livestock, or 100 troy ounces of gold). Foreign currency futures provide for delivery of a specified number of marks, francs, yen, pounds or pesos. U.S. Treasury obligation futures are in terms of instruments having a stated face value (such as $100,000 or $1 million) at maturity. Futures contracts that call for cash settlement rather than delivery are based on a given index number times a specified dollar multiple. This is the case, for example, with stock index futures. Whatever the yardstick, it’s important to know precisely what it is you would be buying or selling, and the quantity you would be buying or selling.

The frantic shouting and signaling of bids and offers on the trading floor of a futures exchange undeniably convey an impression of chaos. The reality however, is that chaos is what futures markets replaced. Prior to the establishment of central grain markets in the mid-nineteenth century, the nation farmers carted their newly harvested crops over plank roads to major population and transportation centers each fall in search of buyers. The seasonal glut drove prices to giveaway levels and, indeed, to throwaway levels as grain often rotted in the streets or was dumped in rivers and lakes for lack of storage. Come spring, shortages frequently developed and foods made from corn and wheat became barely affordable luxuries. Throughout the year, it was each buyer and seller for himself with neither a place nor a mechanism for organized, competitive bidding. The first central markets were formed to meet that need. Eventually, contracts were entered into for forward as well as for spot (immediate) delivery. So-called forwards were the forerunners of present day futures contracts.

Spurred by the need to manage price and interest rate risks that exist in virtually every type of modern business, today’s futures markets have also become major financial markets. Participants include mortgage bankers as well as farmers, bond dealers as well as grain merchants, and multinational corporations as well as food processors, savings and loan associations, and individual speculators.

Futures prices arrived at through competitive bidding are immediately and continuously relayed around the world by wire and satellite. A farmer in Nebraska, a merchant in Amsterdam, an importer in Tokyo and a speculator in Ohio thereby have simultaneous access to the latest market-derived price quotations. And, should they choose, they can establish a price level for future delivery–or for speculative purposes–simply by having their broker buy or sell the appropriate contracts. Images created by the fast-paced activity of the trading floor notwithstanding, regulated futures markets are a keystone of one of the world’s most orderly envied and intensely competitive marketing systems. Should you at some time decide to trade in futures contracts, either for speculation or in connection with a risk management strategy, your orders to buy or sell would be communicated by phone from the brokerage office you use and then to the trading pit or ring for execution by a floor broker. If you are a buyer, the broker will seek a seller at the lowest available price. If you are a seller, the broker will seek a buyer at the highest available price. That’s what the shouting and signaling is about.

In either case, the person who takes the opposite side of your trade may be or may represent someone who is a commercial hedger or perhaps someone who is a public speculator. Or, quite possibly, the other party may be an independent floor trader. In becoming acquainted with futures markets, it is useful to have at least a general understanding of who these various market participants are, what they are doing and why.

Hedgers

The details of hedging can be somewhat complex but the principle is simple. Hedgers are individuals and firms that make purchases and sales in the futures market solely for the purpose of establishing a known price level–weeks or months in advance–for something they later intend to buy or sell in the cash market (such as at a grain elevator or in the bond market). In this way they attempt to protect themselves against the risk of an unfavorable price change in the interim. Or hedgers may use futures to lock in an acceptable margin between their purchase cost and their selling price. Consider this example:

A jewelry manufacturer will need to buy additional gold from his supplier in six months. Between now and then, however, he fears the price of gold may increase. That could be a problem because he has already published his catalog for a year ahead.

To lock in the price level at which gold is presently being quoted for delivery in six months, he buys a futures contract at a price of, say, $350 an ounce.

If, six months later, the cash market price of gold has risen to $370, he will have to pay his supplier that amount to acquire gold. However, the extra $20 an ounce cost will be offset by a $20 an ounce profit when the futures contract bought at $350 is sold for $370. In effect, the hedge provided insurance against an increase in the price of gold. It locked in a net cost of $350, regardless of what happened to the cash market price of gold. Had the price of gold declined instead of risen, he would have incurred a loss on his futures position but this would have been offset by the lower cost of acquiring gold in the cash market.

The number and variety of hedging possibilities is practically limitless. A cattle feeder can hedge against a decline in livestock prices and a meat packer or supermarket chain can hedge against an increase in livestock prices. Borrowers can hedge against higher interest rates, and lenders against lower interest rates. Investors can hedge against an overall decline in stock prices, and those who anticipate having money to invest can hedge against an increase in the over-all level of stock prices. And the list goes on.

Whatever the hedging strategy, the common denominator is that hedgers willingly give up the opportunity to benefit from favorable price changes in order to achieve protection against unfavorable price changes.

Speculators

Were you to speculate in futures contracts, the person taking the opposite side of your trade on any given occasion could be a hedger or it might well be another speculator–someone whose opinion about the probable direction of prices differs from your own.

The arithmetic of speculation in futures contracts–including the opportunities it offers and the risks it involves–will be discussed in detail later on. For now, suffice it to say that speculators are individuals and firms who seek to profit from anticipated increases or decreases in futures prices. In so doing, they help provide the risk capital needed to facilitate hedging.

Someone who expects a futures price to increase would purchase futures contracts in the hope of later being able to sell them at a higher price. This is known as “going long.” Conversely, someone who expects a futures price to decline would sell futures contracts in the hope of later being able to buy back identical and offsetting contracts at a lower price. The practice of selling futures contracts in anticipation of lower prices is known as “going short.” One of the attractive features of futures trading is that it is equally easy to profit from declining prices (by selling) as it is to profit from rising prices (by buying).

Floor Traders

Persons known as floor traders or locals, who buy and sell for their own accounts on the trading floors of the exchanges, are the least known and understood of all futures market participants. Yet their role is an important one. Like specialists and market makers at securities exchanges, they help to provide market liquidity. If there isn’t a hedger or another speculator who is immediately willing to take the other side of your order at or near the going price, the chances are there will be an independent floor trader who will do so, in the hope of minutes or even seconds later being able to make an offsetting trade at a small profit. In the grain markets, for example, there is frequently only one-fourth of a cent a bushel difference between the prices at which a floor trader buys and sells.

Floor traders, of course, have no guarantee they will realize a profit. They may end up losing money on any given trade. Their presence, however, makes for more liquid and competitive markets. It should be pointed out, however, that unlike market makers or specialists, floor traders are not obligated to maintain a liquid market or to take the opposite side of customer orders.

What is a Futures Contract?

There are two types of futures contracts, those that provide for physical delivery of a particular commodity or item and those which call for a cash settlement. The month during which delivery or settlement is to occur is specified. Thus, a July futures contract is one providing for delivery or settlement in July.

It should be noted that even in the case of delivery-type futures contracts, very few actually result in delivery.* Not many speculators have the desire to take or make delivery of, say, 5,000 bushels of wheat, or 112,000 pounds of sugar, or a million dollars worth of U.S. Treasury bills for that matter. Rather, the vast majority of speculators in futures markets choose to realize their gains or losses by buying or selling offsetting futures contracts prior to the delivery date. Selling a contract that was previously purchased liquidates a futures position in exactly the same way, for example, that selling 100 shares of IBM stock liquidates an earlier purchase of 100 shares of IBM stock. Similarly, a futures contract that was initially sold can be liquidated by an offsetting purchase. In either case, gain or loss is the difference between the buying price and the selling price.

Even hedgers generally don’t make or take delivery. Most, like the jewelry manufacturer illustrated earlier, find it more convenient to liquidate their futures positions and (if they realize a gain) use the money to offset whatever adverse price change has occurred in the cash market.

* When delivery does occur it is in the form of a negotiable instrument (such as a warehouse receipt) that evidences the holder’s ownership of the commodity, at some designated location.

Delivery

Since delivery on futures contracts is the exception rather than the rule, why do most contracts even have a delivery provision? There are two reasons. One is that it offers buyers and sellers the opportunity to take or make delivery of the physical commodity if they so choose. More importantly, however, the fact that buyers and sellers can take or make delivery helps to assure that futures prices will accurately reflect the cash market value of the commodity at the time the contract expires–i.e., that futures and cash prices will eventually converge. It is convergence that makes hedging an effective way to obtain protection against an adverse change in the cash market price.*

* Convergence occurs at the expiration of the futures contract because any difference between the cash and futures prices would quickly be negated by profit-minded investors who would buy the commodity in the lowest-price market and sell it in the highest-price market until the price difference disappeared. This is known as arbitrage and is a form of trading generally best left to professionals in the cash and futures markets.

Cash settlement futures contracts are precisely that, contracts which are settled in cash rather than by delivery at the time the contract expires. Stock index futures contracts, for example, are settled in cash on the basis of the index number at the close of the final day of trading. There is no provision for delivery of the shares of stock that make up the various indexes. That would be impractical. With a cash settlement contract, convergence is automatic.

Margins

As is apparent from the preceding discussion, the arithmetic of leverage is the arithmetic of margins. An understanding of margins–and of the several different kinds of margin–is essential to an understanding of futures trading.

If your previous investment experience has mainly involved common stocks, you know that the term margin–as used in connection with securities–has to do with the cash down payment and money borrowed from a broker to purchase stocks. But used in connection with futures trading, margin has an altogether different meaning and serves an altogether different purpose.

Rather than providing a down payment, the margin required to buy or sell a futures contract is solely a deposit of good faith money that can be drawn on by your brokerage firm to cover losses that you may incur in the course of futures trading. It is much like money held in an escrow account. Minimum margin requirements for a particular futures contract at a particular time are set by the exchange on which the contract is traded. They are typically about five percent of the current value of the futures contract. Exchanges continuously monitor market conditions and risks and, as necessary, raise or reduce their margin requirements. Individual brokerage firms may require higher margin amounts from their customers than the exchange-set minimums.

There are two margin-related terms you should know: Initial margin and maintenance margin.

Initial margin (sometimes called original margin) is the sum of money that the customer must deposit with the brokerage firm for each futures contract to be bought or sold. On any day that profits accrue on your open positions, the profits will be added to the balance in your margin account. On any day losses accrue, the losses will be deducted from the balance in your margin account.

If and when the funds remaining available in your margin account are reduced by losses to below a certain level–known as the maintenance marginrequirement–your broker will require that you deposit additional funds to bring the account back to the level of the initial margin. Or, you may also be asked for additional margin if the exchange or your brokerage firm raises its margin requirements. Requests for additional margin are known as margin calls.

Assume, for example, that the initial margin needed to buy or sell a particular futures contract is $2,000 and that the maintenance margin requirement is $1,500. Should losses on open positions reduce the funds remaining in your trading account to, say, $1,400 (an amount less than the maintenance requirement), you will receive a margin call for the $600 needed to restore your account to $2,000.

Before trading in futures contracts, be sure you understand the brokerage firm’s Margin Agreement and know how and when the firm expects margin calls to be met. Some firms may require only that you mail a personal check. Others may insist you wire transfer funds from your bank or provide same-day or next-day delivery of a certified or cashier’s check. If margin calls are not met in the prescribed time and form, the firm can protect itself by liquidating your open positions at the available market price (possibly resulting in an unsecured loss for which you would be liable).

Spreads

While most speculative futures transactions involve a simple purchase of futures contracts to profit from an expected price increase–or an equally simple sale to profit from an expected price decrease–numerous other possible strategies exist. Spreads are one example. A spread, at least in its simplest form, involves buying one futures contract and selling another futures contract. The purpose is to profit from an expected change in the relationship between the purchase price of one and the selling price of the other. As an illustration, assume it’s now November, that the March wheat futures price is presently $3.10 a bushel and the May wheat futures price is presently $3.15 a bushel, a difference of 5 cents. Your analysis of market conditions indicates that, over the next few months, the price difference between the two contracts will widen to become greater than 5 cents. To profit if you are right, you could sell the March futures contract (the lower priced contract) and buy the May futures contract (the higher priced contract). Assume time and events prove you right and that, by February, the March futures price has risen to $3.20 and May futures price is $3.35, a difference of 15 cents. By liquidating both contracts at this time, you can realize a net gain of 10 cents a bushel. Since each contract is 5,000 bushels, the total gain is $500.

The Contract Unit

Delivery-type futures contracts stipulate the specifications of the commodity to be delivered (such as 5,000 bushels of grain, 40,000 pounds of livestock, or 100 troy ounces of gold). Foreign currency futures provide for delivery of a specified number of marks, francs, yen, pounds or pesos. U.S. Treasury obligation futures are in terms of instruments having a stated face value (such as $100,000 or $1 million) at maturity. Futures contracts that call for cash settlement rather than delivery are based on a given index number times a specified dollar multiple. This is the case, for example, with stock index futures. Whatever the yardstick, it’s important to know precisely what it is you would be buying or selling, and the quantity you would be buying or selling.

History and Fundamentals

Often considered the “poor man’s gold” silver has been climbing the investment and demand charts since its discovery thousands of years ago in Anatolia, now modern day Turkey. Silver’s unique properties make it ideal for thousands of applications found in every day life.

Silver is:

- The best conductor of electricity of all Metals

- The best conductor of heat of all metals

- The most reflective of metals

- A powerful anti-bacterial & anti-viral agent

- Malleable and ductile

- Valued for its beauty

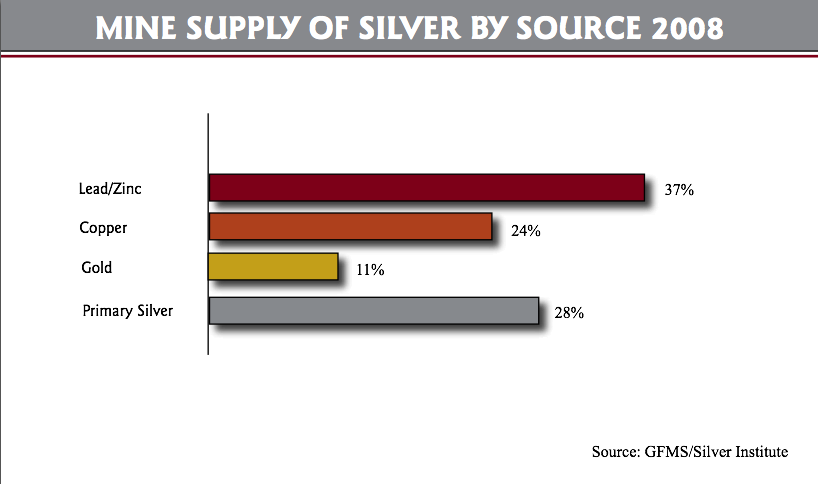

Silver is found today in mines around the world; the top producing mining countries are Peru, Mexico and China.

HISTORY OF SILVER MINING

3000 BC The first major silver mines were discovered in Anatolia, modern day Turkey.

1st C. AD Roman discoveries developed Spain into a major silver producer.

Early 1500s After Columbus’ New World expeditions, the discovery of huge, prolific silver deposits in Mexico, Peru and Bolivia changed the focus of silver mining and enriched the Spanish Empire for 300 years.

1500 – 1875 Approximately 1.5 billion ounces mined in Mexico with the majority produced during the 1700’s. 1700s The backbone of the Spanish Empire was the

one billion ounces of silver produced from Veta Madre (The Mother Vein) in Guanajuato Mexico (Endeavour Silver has mines hosted in the Veta Madre) .

1857 Silver mining became an important industry in the State of Nevada (The Silver State) when the fabled Comstock Lode was discovered.

1859 – 1877 Comstock yielded silver and gold with a value aproaching $400 million, the equivalent of more than $500 billion today.

1900 – 1920 50 per cent expansion in global production to about 190 million troy ounces annually spurred by discoveries in several countries including Canada, the United States and Mexico.

1921 – Present Improved techniques in ore separation allowed for concentration of silver with lead, zinc and copper. The explosion in production of these various base-metal sources has led to an increase in both silver output and silver usage. 3000BC – Present All the silver ever mined would fit in a 55 metre cube.

3000BC – Present All the silver ever mined would fit in a 55 metre cube.

HISTORY OF SILVER AS CURRENCY

CA 2500 BC Silver first introduced into Egypt and was considered more valuable than gold.

475 BC China was the first country to monetize silver.

775 AD “British Pounds Sterling”: in approximately 775 AD the Saxon kingdoms issued silver coins known as “sterlings”, 240 of them being minted out of one pound of silver. Large payments were reckoned in “pounds of sterling” later shortened to “pounds sterling.”

1072 After the Norman Conquest, the pound was divided for simplicity of accounting into 20 shillings and 240 pence or pennies.

1497 Spanish “Pieces of Eight” were coins first struck in 1497 containing a high silver purity and weight. They were the basis of the monetary system of the Spanish Empire and were widely circulated around the world. They were accepted as legal tender in the US until 1857.

1600’s – 1900’s The Mexican Peso evolved into one of the world’s strongest and most widely accepted currencies due to its silver content.

1800s By the mid 1800s, China through trade and mercantilism, was in possession of 50% of the world’s above ground silver. The British sold opium to China in exchange for tea, silk and silver – a factor in the Opium Wars between Great Britain and China during the mid -1800s.

1930s Silver was used as China’s official currency until the 1930s.

SILVER APPLICATIONS

Industrial:

As the best conductor of electricity, silver has a multiple of uses in switches, contacts and fuses in electrical appliances, automobiles and electronics such as computers, TV’s, DVD + CD players and cell phones.

Chemical reactions use silver as a catalyst; approximately 700 tons of silver are consumed annually in the production of plastics. Mitsui of Japan is developing a catalytic converter for diesel engines using silver as opposed to platinum or palladium.

Billions of silver oxide-zinc batteries are produced annually for use in watches, cameras and small electronic devices.

Invisible silver is a thin coating of silver on double thermal windows. This coating not only rejects the heat from the sun, but also reflects internal heat inward.

As the most reflective of metals, silver is used in specialized optical devices, automobile windshields and for both commercial and household mirrors.

Very little silver used in industrial applications is re-cycled, it is consumed.

Health:

Hippocrates, the father of modern medicine, wrote that silver had beneficial, anti-disease properties.

Wealthy, ancient Greeks, Romans and Phoenicians stored their wine, water and oil in silver jugs to maintain their freshness and prevent spoiling.

Silver compounds show a toxic effect on some bacteria, viruses, algae and fungi. Health and medical applications of silver are wide ranging and its uses include dressings and ointments for burns and wounds, anti-bacterial pharmaceuticals, coatings on hospital implements and surfaces, to name a few.

Silver is being used to treat wastewater and to treat streams containing radioactive and biological contaminants.

Silver is increasingly being used for water purification and as an anti-bacterial agent in swimming pools.

Clothing is being manufactured with silver impregnated fabric to kill bacteria and fungi in order to reduce disease and odour. Military uniforms, sporting wear and everyday clothing are now produced that contain this special fabric.

Recent research shows that silver also promotes the production of new cells, increasing the rate of healing wounds and bone.

Alexander the Great was advised by Aristotle to store boiled water in silver containers to prevent diseases caused by contaminated water

ANNUAL USES OF SILVER

2008 % of Total Use

Jewerly and Silverware 261.0 37.7 %

Photography 140.7 20.3 %

Electronics and Batteries 123.4 17.8 %

Brazing Alloys/Solders 51.6 7.4 %

Coinage 28.2 4.1 %

Super Conductors 18.0 2.6 %

Mirror 11.3 1.6 %

Caustic Silver 7.2 1.0 %

Tube, Sheet and Bar 6.3 0.9 %

Biocides 6.0 0.9 %

Miscellanous 39.5 5.7 %

“Gold is the sweat of the sun, silver is the tears of the moon”

Inca proverb

Silver Fundamentals

History of Silver contributed by Hugh Clarke, VP Corporate Communications Endeavour Silver Corp. www.edrsilver.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair