Since the blow off in April 2012, total market sales have tried and failed several times to break above the new lower stair tread of declining sales. Bulls now have to wait until the spring of 2014 before they can try to bring the rest of us along for another ride, because seasonally, the peak sales window is in late spring, early summer.

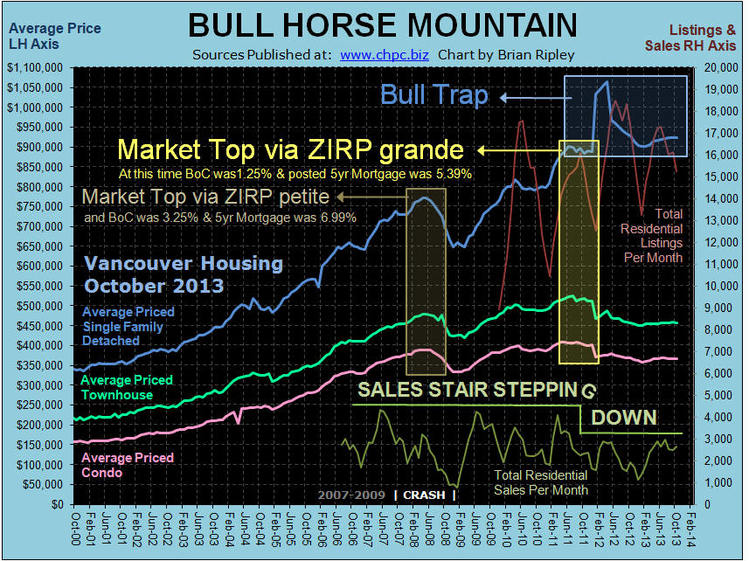

One other observation is that the ZIRP petite market top in the spring of 2008 was accomplished with a Bank of Canada Bank Rate set at 3.25% and retail banks posting a consumer 5 Year Fixed rate mortgage at 6.99%; but the sales crash was already in motion and headed towards the March 2009 pit of gloom. To get the housing market not to collapse because well over 10% of Canadian GDP is a result of the construction industry (twice the U.S. reliance) Chart Here; the BoC moved to ZIRP grande with a Bank of Canada Bank Rate set at 1.25% and the retail banks posted their consumer 5 Year Fixed rate mortgage at 5.39%. This policy of price controls on the cost of credit has not stopped sales from stair stepping lower. If you want to remove the mask from asset price discovery, do what a good appraiser does; an income approach. Imagine what a small increase in mortgage rates, say back to ZIRP petite will do to your disposable income.

Wikipedia defines a BULL TRAP as “an inaccurate signal that shows a decreasing trend in a stock or index has reversed and is now heading upwards, when in fact, the security will continue to decline. It is seen as a trap because the bullish investor purchases the stock, thinking it will increase in value, but is trapped with a poor performing stock whose value is still falling.”

“The Condo Game”